NEWS

3 Sep 2025 - The UK ETS - a policy mechanism to deliver net zero

|

The UK ETS - a policy mechanism to deliver net zero abrdn August 2025 The result of the UK Emission Trading Scheme (ETS) consultation could provide a pathway to net-zero emissions by 2050 and potentially offer a roadmap for global climate policy. What's the issue?Net zero refers to a state where the residual emissions that remain after all feasible decarbonisation has taken place are neutralised by carbon removals. The UK targets net-zero emissions by 2050 (Scotland by 2045). Yet, until now, there has been no clear policy mechanism to address these residual emissions. In July, the UK Government released the long-awaited outcome to its consultation on Integrating Greenhouse Gas Removal (GGRs) into the UK ETS. Historically, GGR credits were only usable in voluntary carbon markets as offsets. The new proposal would allow their inclusion in compliance markets, creating a policy mechanism we believe is necessary to achieve a true net-zero end-state. Each year, organisations subject to the UK ETS must purchase and submit emissions allowances through auctions, in line with their operational emissions. Under the proposed changes, GGRs would be made available through the auction mechanism, replacing normal emissions allowances on a one-for-one basis. Crucially, this will not affect the overall supply cap, which continues to decline annually and remains the primary lever through which the ETS drives decarbonisation. Intuitively, this is a sensible approach. To date, revenues from ETS auctions have flowed into the UK Treasury's general budget. Integrating GGRs would continue to boost Treasury revenue, albeit to a lesser extent, while also incentivising capital flows into carbon removal projects. While imperfect, the approach offers a dual benefit of incentivising decarbonisation and generating capital for carbon removal projects. A definitive list of the eligible removal methods hasn't been provided, but it will be guided by the forthcoming GGR British Standard Institution (BSI) standards, which currently includes:

Why are woodland and peatland not on that list?Peatland restorationNot currently on the list, as it avoids emissions rather than removes them. We think excluding peatlands is a misstep. In the UK, degraded peatlands are a significant source of emissions, accounting for 15-20% of Scotland's emissions alone. Their absence from the GGR means there's still no clear financial mechanism to help prevent these emissions. WoodlandThere's a strong indication that woodland creation will be included, but a few things must be resolved first: 1. Standard alignment: The UK Woodland Carbon Code (a voluntary scheme) already sets out standards that the GGR BSI will seek to develop. A decision is needed on whether these two frameworks will co-exist or be consolidated. 2. Policy debate: The UK Climate Change Committee recommended against inclusion, citing concerns around permanence, measurement and verification. Additionally, it highlighted the risk of market distortion and a strategic focus on engineered removals. However, several key organisations (including Department for Environment, Food and Rural Affairs) have pushed back on these concerns. What are the investment risks and opportunities?The proposed integration signals growing policy support and improves long-term market stability for GGR projects. It promotes investment in six ways. 1. Clear integration timeline - lays out the plan to legislate by 2028 and operationalise GGR integration into the ETS by the end of 2029. While subject to additional regulatory assessments and consultation, this blueprint helps reduce uncertainty for GGR developers and investors. 2. Ex-post credit issuance and long-term storage - UK ETS allowances will only be awarded after verified carbon sequestration, ensuring environmental integrity and accountability. Projects must also demonstrate a minimum carbon storage period of 200 years, with liability and fungibility measures in place. While this strengthens credibility, it diverges from some practices in the voluntary carbon market. 3. UK-based projects only - eligibility is limited to domestic removal projects, which is a positive for UK-based initiatives. Moreover, it enables offtake agreements to proceed, helping unlock investment. 4. GGR operators - improved liquidity and price discovery for GGR credits. 5. Double-whammy for carbon capture operators - companies investing in carbon capture infrastructure stand to gain on two fronts: they reduce exposure to the UK ETS carbon price (currently £48/tCO₂) and could potentially generate revenue through GGR credits. This dual incentive could significantly improve project economics. That said, we have concerns about large-scale UK assets, such as Drax's 2.6GW biomass power station, where upstream supply-chain emissions might not be adequately accounted for. Smaller operations, including Evero's Ince biomass power station at 21.5MW, raise fewer concerns. By 2029, the Ince BECCS project will seek to use the HyNet CCS infrastructure to transport and store around 250,000 tonnes of carbon beneath the Irish Sea. Several companies own biomass plants that could meet the criteria: RWE, Veolia, SSE, and E.ON. 6. Improved UK investor sentiment towards nature-based solutions - there's strong momentum behind including woodland creation in the ETS, which would create a demand floor for such projects. Woodland creation is also cheaper than engineered removals like BECCS, making the opportunity scalable and cost-effective. Government modelling suggests including woodland creation in the ETS could result in a cumulative carbon sequestration of 29-39 MtCO2e by 2050 [1] But the benefits go well beyond carbon: the same modelling estimates a Net Present Social Value (NPSV) of £27-34 billion by 2027 [2], factoring in carbon savings, job creation, and wider ecosystem services such as flood protection, improved air quality, and biodiversity gains. (NPSV is an estimate of the total societal benefits of a policy or project, such as health, environmental, and economic gains, expressed in today's money.) Our take?We've responded to the consultation and are encouraged by the findings. While we await final confirmation and further detail, we believe this marks a positive policy shift, one that broadens the range of technologies available to decarbonise the economy. It also strengthens the financial case for these projects and could spur the development of new asset classes, increasing opportunities to support decarbonisation at a lower cost. The UK's policy drive is not happening in isolation. We're seeing similar developments in the EU, California, Quebec, and Brazil [3]. We therefore expect this year's COP30 conference to emphasise the important role of nature-based carbon removals and sinks in the global journey to net zero. |

|

Funds operated by this manager: abrdn Sustainable Asian Opportunities Fund , abrdn Emerging Markets Equity Fund , abrdn Sustainable International Equities Fund , abrdn Global Corporate Bond Fund (Class A) Sources include Carbonfuture's 2025 Global Guide to CDR Policy, CCarbon's WCI Emissions Outlook 2025-2026, and Climate Transparency's Implementation Check on Brazil's Carbon Market.

|

2 Sep 2025 - Australian Secure Capital Fund - Market Update

|

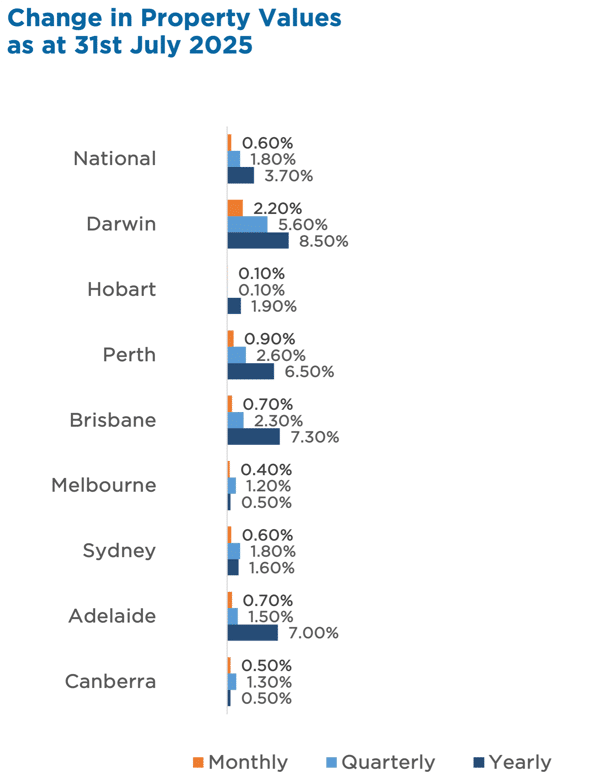

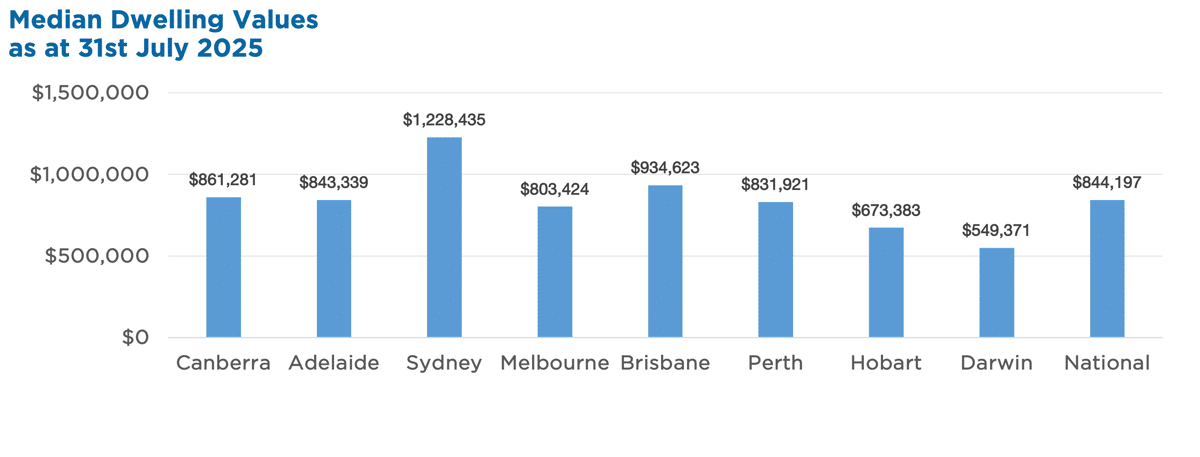

Australian Secure Capital Fund - Market Update Australian Secure Capital Fund August 2025 Australia's housing market kept its winning streak alive in July, with values rising 0.6% -- the sixth straight month of gains. Every capital city saw an uplift, led by Darwin's standout +2.2% and Perth's strong +0.9%. Tight supply (19% below average) and resilient buyer demand are keeping competition fierce, pushing auction clearance rates above the decade average. Houses are still in the lead, up 1.9% for the quarter (about $16,700), while units rose 1.4% (~$9,700) -- widening the record price gap to $223,000. Highlights:

Property Values

|

1 Sep 2025 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

|

||||||||||||||||||||||

| Wilson Asset Management Leaders Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

||||||||||||||||||||||

| La Trobe Australian Credit Fund - 12 Month Term | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

||||||||||||||||||||||

| RMC Enhanced Income Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Remara Investment Grade Credit Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Remara Credit Income Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

| Remara Credit Opportunities Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

| Remara Opportunistic Development Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

Want to see more funds? |

||||||||||||||||||||||

|

Subscribe for full access to these funds and over 900 others |

29 Aug 2025 - Hedge Clippings |29 August 2025

|

|

||

|

Hedge Clippings | 29 August 2025

News | Insights New Funds on FundMonitors.com The art of the comeback | Magellan Asset Management Recognising a stumble from a fall | Canopy Investors July 2025 Performance News Equitable Investors Dragonfly Fund DAFM Digital Income Fund (Digital Income Class) |

||

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |

29 Aug 2025 - Performance Report: TAMIM Fund: Global High Conviction Unit Class

[Current Manager Report if available]

28 Aug 2025 - Performance Report: ASCF High Yield Fund

[Current Manager Report if available]

28 Aug 2025 - Are you sure about that? The folly of forecasting

27 Aug 2025 - Performance Report: Insync Global Quality Equity Fund

[Current Manager Report if available]

27 Aug 2025 - Recognising a stumble from a fall

|

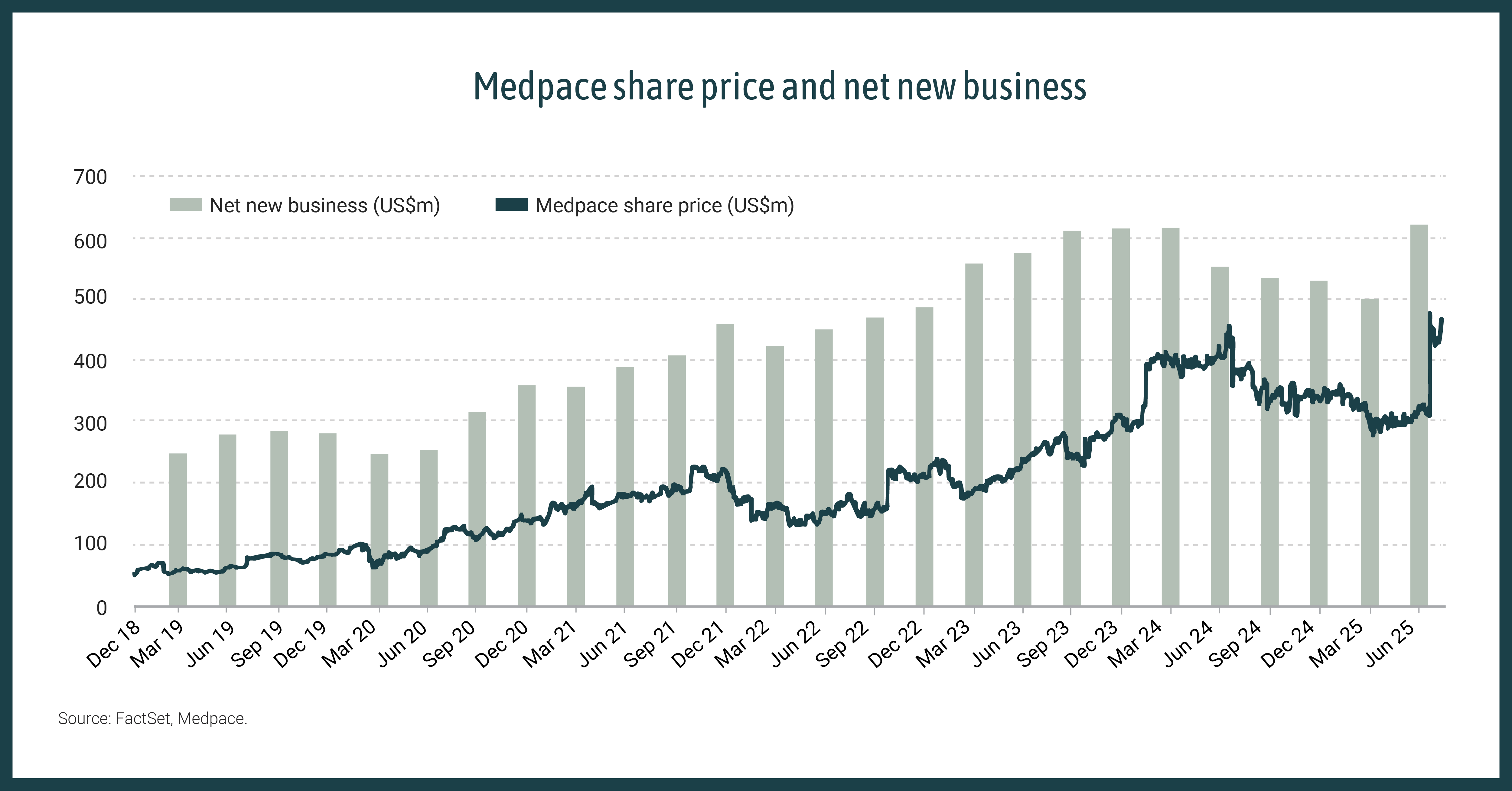

Recognising a stumble from a fall Canopy Investors August 2025 Quality companies typically trade at premium valuations, but when cyclical headwinds are conflated with secular falls, even the best businesses can be dismissed by the market. When heroes stumble excessive negativity can present opportunities to buy quality at a discount. Quality companies are often not hard to spot. The best are well known and trade at a premium valuation as a result. Despite their appeal, quality companies can be risky investments if the price paid is too high. Yet there are times when investors have the opportunity to buy quality at a discounted price, often when cyclical headwinds are conflated with secular concerns, fuelling negative sentiment and fear that the stock is 'dead money' with limited near-term upside. Medpace (MEDP)Take Medpace, for example, an investment in the Canopy Global Small & Mid Cap Fund. This founder-led clinical research organisation focuses on small biotechs and boasts an enviable track record: many years of sales growth exceeding 20%, expanding margins and returns, high cash conversion, and no debt. Its sales represent less than 5% of an addressable market expected to grow 10% pa over the long term. However, from mid-2024 Medpace disclosed lower net new business wins for four consecutive quarters, due to an unexpected increase in trial cancellations by its clients, blamed mostly on a weak funding environment. A litany of additional concerns piled on: potential negative impacts from US drug pricing policy changes, cuts to FDA and NIH funding under the new Secretary of Health and Human Services, and pricing pressure from larger competitors. Despite no fundamental change in the scale of unmet medical need addressed by small biotech, or to Medpace's ability to capture this long-term opportunity, the stock was dismissed by many as 'dead money' with no obvious near-term catalysts, and its share price declined by one-third over the course of a year. At Canopy, we believe investing in high-quality companies at the moment of maximum market pessimism can deliver high returns with relatively low risk. Our Fund holds positions in several companies at various points in their dead money journey. In this instance, we increased our investment in Medpace as investor concerns mounted and the share price fell, improving its return potential, even as the recovery timing remained uncertain. Eventually, the fundamentals reasserted themselves. In Q2, Medpace delivered a surprisingly strong result, with cancellations reverting to normal levels, driving higher net new business growth, which should support higher revenue growth over the coming years. When a positive surprise occurs in a so-called dead money stock, the reaction can be dramatic: Medpace's share price increased 50% the day after the Q2 result. While there was probably no way of predicting the result in advance, the Medpace experience highlights how long term investors can recognise a stumble, as opposed to a fall, and with conviction in the company's long-term prospects, buy quality at a discount.

Source: FactSet, Medpace |

|

Funds operated by this manager: |

26 Aug 2025 - Performance Report: DAFM Digital Income Fund (Digital Income Class)

[Current Manager Report if available]