News

4 Mar 2026 - Volatility Is Information: Reading the Signals Beneath the Surface

|

Volatility Is Information: Reading the Signals Beneath the Surface JCB Jamieson Coote Bonds February 2026 (3-minute read) The investment outlook this year remains shrouded by uncertainty, accompanied by elevated volatility in expected returns. Markets are searching for direction, and investors are navigating an environment where conviction feels harder earned. Volatility, of course, wears many faces. We can observe it in the lived experience of asset price return variability across securities, sectors and markets. Or we may deduce the anticipated range of returns over the next week, month or quarter from options prices. Either way, the direction, size and interdependencies (correlations) of movements in market pricing at all frequencies can provide important signals for astute investors. Volatility is not simply noise, it is information. Right now, equity prices, cryptocurrencies, and precious metals are relatively more volatile. Yet in contrast, most bond markets remain curiously subdued. Yields remain broadly rangebound, only tentatively challenging the edges of recent ranges, reticent to enter an elusive new regime or steady state. That restraint in bond markets is notable, and perhaps more revealing than the visible turbulence elsewhere. After hiking rates earlier this month, RBA Governor Michelle Bullock stopped short of offering explicit forward guidance, indicating that the Monetary Policy Board is heavily data dependent. This suggests further policy restriction may have limited efficacy in controlling persistently above-band inflation back to the target range. Australian government bond yields decreased markedly in response, and the market is paring back pricing for hikes and beginning to tentatively pre-empt future rate cuts next year. The tone has shifted, from further restriction to a growing debate about how long policy will need to remain restrictive at all. More broadly, attention is turning to the Government for direction ahead of the upcoming Federal Budget. There is growing recognition that boosting labour productivity through innovation, enhanced competition and meaningful structural and tax reform remains the only sustainable path to higher national income and improved living standards for all Australians. Meanwhile, across the Pacific in the U.S., economic activity continues to show surprising resilience. January brought unexpectedly strong employment growth, thanks in part to seasonal factors (despite large historical downward revisions). Price pressures, meanwhile appear to be cooling, although the data remains messy and influenced by lingering U.S. federal government shutdown-related disruptions. The result? Short-dated Treasury yields have drifted to multi-year lows, reflecting cautious optimism among investors. The market has almost priced for three U.S. Federal Reserve rate cuts this year under U.S. Federal Reserve Chair nominee Kevin Warsh, although the upcoming midterm elections loom large over the U.S. macro outlook and the Trump administration's near-term policy priorities. In Europe, inflation appears to be well controlled and the European Central Bank comfortably on hold, but recent geopolitical events have raised existential questions around the protection and advancement of national and regional interests, and defence and security strategy. While this may be the quintessential European moment to rebalance the world order away from U.S. dominance if traditional allegiances like NATO are set to be dissolved, there have been fundamental disagreements between Germany and France around policy priorities to restore competitiveness and how to fund quickly growing defence expenditures. Yields on German government bonds have also dropped materially in recent weeks. In Japan, the Liberal Democratic Party lead by Sanae Takaichi has emerged victorious from lower house elections. Takaichi's expanded mandate and firm command over political and economic power (for instance, Japan's central bank is not independent of government) after her historic win, combined with a sense of renewed optimism across global markets that the realisation of her vision for Japan will not unduly impact interest rates and exchange rates beyond what is already envisaged, has led to a relief rally in Japanese Government Bonds after a tumultuous January. What signal can we draw from the subdued historical measures of volatility across bond yields, especially when viewed against the domestic and global macro backdrop? There are three key takeaways. First, periods of volatility and uncertainty (whether obvious or hidden) can bring significant opportunity to generate attractive returns for those who act thoughtfully. Second, fortune rewards the diligent and there are only downside risks to complacency. And third, and most importantly, diversification, both within and across asset classes and sectors is the primary means with which to dampen the effects of volatility and protect long-term investment outcomes. Volatility may rattle markets, but it also sharpens our focus, driving better portfolio construction and smarter asset allocation decisions. Funds operated by this manager: CC Jamieson Coote Bonds Active Bond Fund (Class A) , CC Jamieson Coote Bonds Dynamic Alpha Fund This information is for professional and wholesale investors only and has been prepared by JamiesonCooteBonds Pty Ltd ACN 165 890 282 AFSL 459018 ('JCB'). Channel Investment Management Limited ACN 163 234 240 AFSL 439007 ('CIML') is the Responsible Entity and issuer of units for the CC JCB Active Bond Fund ARSN 610 435 302, CC JCB Global Bond Fund ARSN 631 235 553 and the CC JCB Dynamic Alpha Fund ARSN 637 628 918 (collectively 'the Funds'). Channel Capital Pty Ltd ACN 162 591 568 AR No. 001274413 ('Channel') provides investment infrastructure and distribution services for JCB and is the holding company of CIML. |

3 Mar 2026 - Phil Strano: Levered credit back from the dead

|

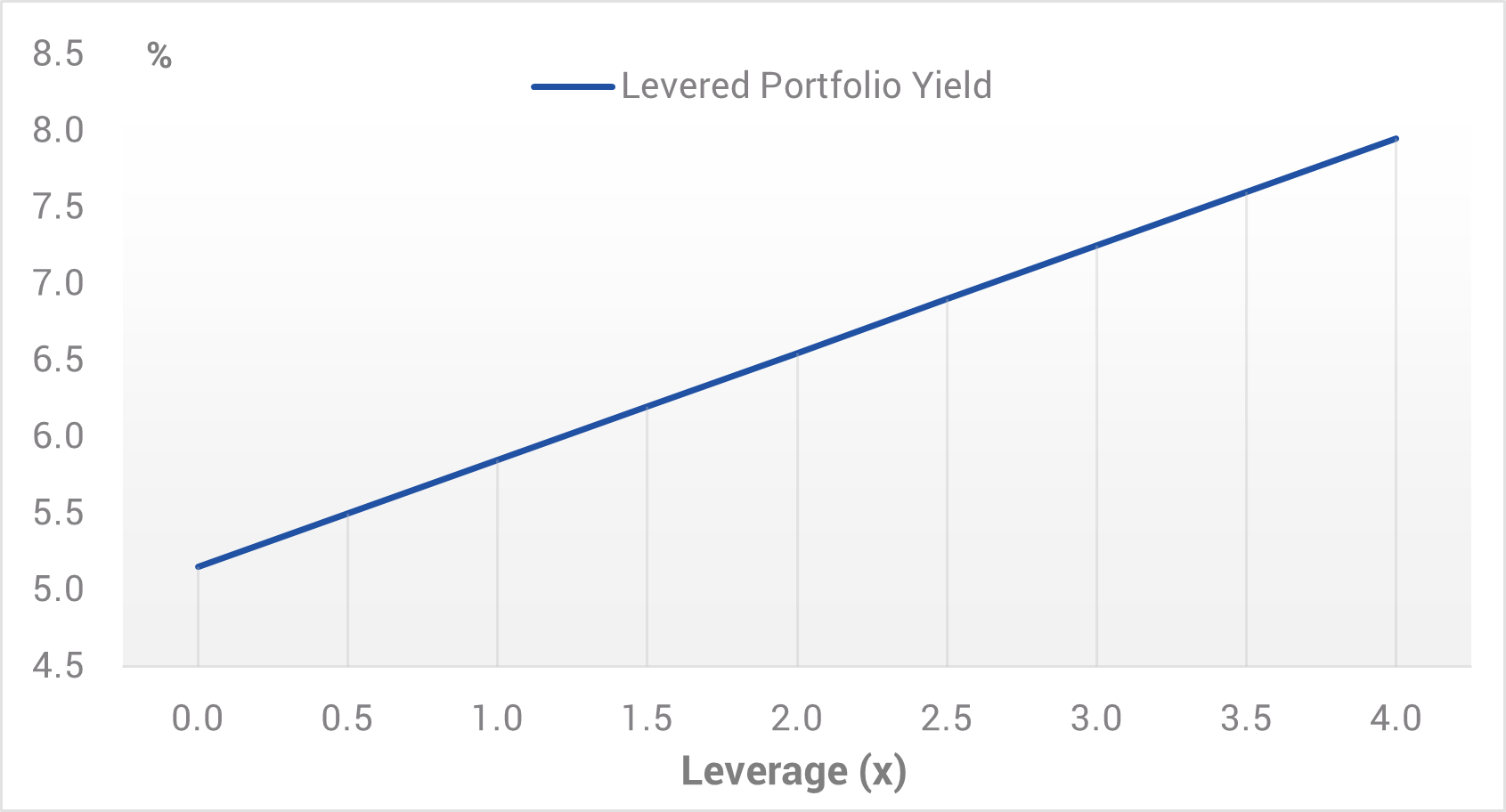

Phil Strano: Levered credit back from the dead Yarra Capital Management February 2026 (8-minute read) In 2025, with credit spreads normalising, and in some segments moving below long-term averages, a number of yield hungry credit investors responded by adding risk to meet investment objectives. These additional risks to sustain portfolio yields of 6%+ varied from increasing credit risk, interest/spread duration and/or leverage. While mostly still at manageable levels, increased debt funding of credit securities is nonetheless a throwback to the heady pre-GFC era where synthetic and physical leverage was more commonplace. Indeed, we are now also hearing of less sustainable practices once again creeping into the credit investment lexicon. From our discussions in the marketplace towards the tail-end of 2025, the use of leverage is principally occurring through the use of repurchase agreements (repo) of eligible collateral up to an eye watering 15-times for AAA rated securities, as well as via placement of senior secured leverage to enhance portfolio yields in both private and public credit portfolios. New levered investment products that have recently entered the market offer a floating rate running yield from a portfolio likely comprised of major bank T2 hybrids (T2s) and investment grade (IG) corporate bonds. Products such as these typically seek to enhance yield by deploying 3-3.5-times leverage. Leverage enhances yields and amplifies performance (both positively and negatively) from changes in spreads and any impairments/defaults. Working off current pricing, an IG portfolio yielding ~5.0-5.5% p.a. with ~3-times leverage moves what is an already enhanced yield into a yield in the 7%+ range (refer Chart 1). Chart 1: YCM estimate: Levered IG portfolio yields

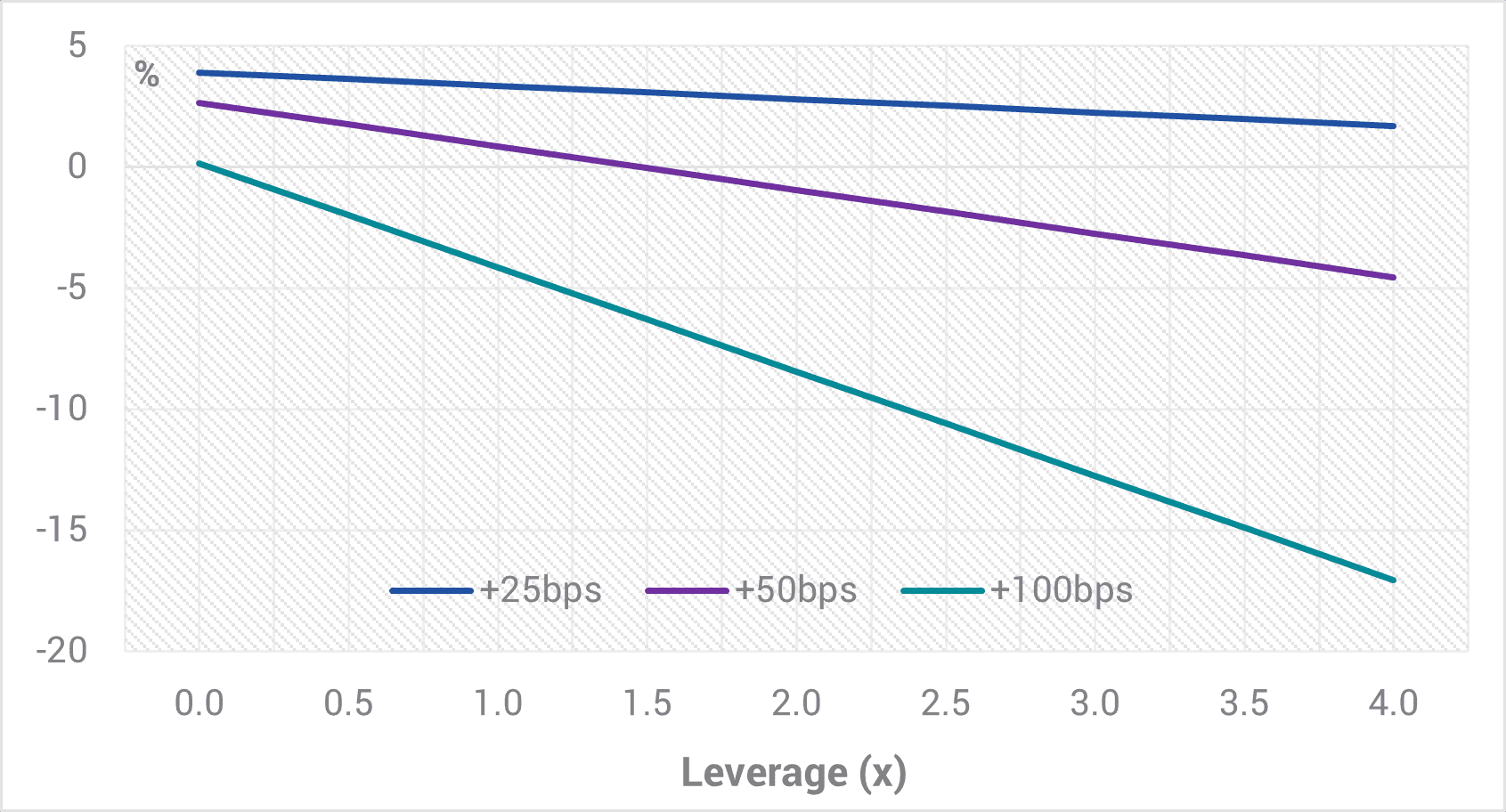

Source: Yarra Capital Management Feb 2026.The use of leverage to enhance returns can work very effectively in environments of stable or contracting credit spreads. It is a double-edged sword, however, with the combination of widening credit spreads and leverage usually resulting in significant drawdowns. For instance, working off an estimated credit spread duration of ~5 years, a widening spread environment would quickly overwhelm underlying yields, with a ~100bp spread expansion on 3-times leverage generating a negative total return in the range of 10-15% from what is an underlying low risk IG credit portfolio (refer Chart 2). Chart 2: YCM estimate: Levered total returns and widening credit spreads

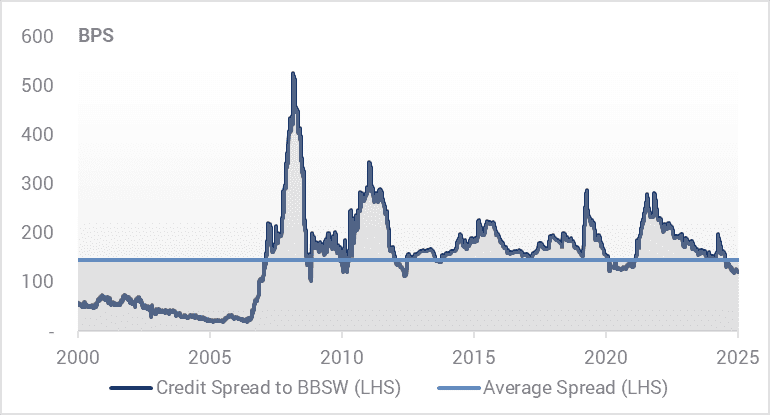

Source: Yarra Capital Management Feb 2026.Given fixed income investors generally have a low tolerance for negative returns over a 12-month period, the use of significant leverage to enhance returns could be somewhat of a dubious exercise, especially when you consider today's starting point. As evidenced by major bank T2s, credit spreads have performed over the last 2-3 years and now sit around their long term averages across most segments of Australian credit and significantly below the previous peak in 2022 (refer Chart 3). Chart 3: Major Bank Tier 2 5-year FRNs (credit spreads and yields)

Source: Yarra Capital Management Feb 2026.At current spread levels, the probability of a +/-100bp move is weighted to the positive and in the current macroeconomic environment is entirely possible over the near to medium term. In such an event, which can occur two to three times each decade, the prospect of equity like drawdowns from levered credit funds should give credit investors pause for thought. Put more simply, credit investors in these levered structures should be thinking hard about whether they are comfortable taking what is effectively equity drawdown risk for a miserly 1-2% in additional yield. We would suggest that this represents incredibly poor compensation for the risk assumed at this point in the cycle. In contrast to levered credit funds, both the Yarra Enhanced and Higher Income Funds are still providing attractive 6-7% yields with precisely zero leverage. Moreover, while it is true that a 100bps widening in credit spreads would lead to value diminution for both these funds, high unlevered yields combined with active management should protect against negative returns over any 12-month period. We do not believe the same can be said of levered credit funds running a similar mix of underlying credit assets. |

|

Funds operated by this manager: Yarra Australian Bond Fund , Yarra Australian Equities Fund , Yarra Emerging Leaders Fund , Yarra Income Plus Fund , Yarra Enhanced Income Fund , Yarra Australian Smaller Companies Fund , Yarra Ex-20 Australian Equities Fund , Yarra Global Small Companies Fund , Yarra Higher Income Fund |

2 Mar 2026 - Data demand heats up

27 Feb 2026 - Hedge Clippings |27 February 2026

|

|

|

|

Hedge Clippings | 27 February 2026 Wednesday's January monthly CPI figure, which came in at an annualised 3.8%, unchanged over the previous month, was not the news that either Jim Chalmers or Michelle Bullock would have wanted, nor, for that matter, anyone with a mortgage. Worse still was the trimmed mean result, the RBA's preferred inflationary measure, which edged up to 3.4% from the previous month's result of 3.3%. Amongst the details, but certainly not hiding, was an increase in electricity prices of over 32%, up from 21% in the previous month, and various government subsidies and handouts expired. Chalmers will be hoping that the effects of the RBA's rate rise earlier this month will kick in quickly, although it probably won't come quickly enough for the February number, due out on the 25th of March to have any influence on the RBA when they meet the week before. It's looking decidedly as if inflation of 3-4% is in danger of becoming entrenched, so the decision for Bullock and her board will hinge between biting the bullet and hiking rates again - either in March, and if not then in May - or hoping for the best. Unfortunately, "hope is not a strategy", and history indicates that rate rises seldom occur in isolation. What must now be clear to the RBA, albeit with the benefit of hindsight, is that they moved too soon - or too quickly, or both - when cutting rates three times last year. Moving on... There has been renewed focus recently on the benefits or otherwise of "active" fund management, compared with "passive" management via an index or ETF. The case for passive seems simple on the surface: Why pay "active" fees when the returns of the average fund struggle to exceed the index, or the low fee ETF, which tracks the weighted average return of all companies in the index? The argument becomes more compelling in times of strong equity markets, when the underlying market (and therefore the ETF) is, or has been, providing above long term average returns. For instance, in the Australian small and mid-cap space, the average 12-month return in AFM's Peer Group of 99 funds to the end of January was 13.38%, against the S&P/ASX Small Ordinaries Index of 22.75%, although the result was closer over 3 years at 11.62% and 12.08% respectively, and almost level pegging at 7.77% and 7.48% over 5 years. The data covering large-cap funds vs. the ASX 200 is similar, although returns from the smaller end of the market are significantly higher. The problem or catch is the term "average". Just as the index comprises companies that have performed significantly better (and in some cases many times) or worse than the market average, the same goes for managed funds. In the small mid-cap space, more than 10% of the funds returned over 30% (after fees), with the top 2, Aliwa Alpha, and SGH Emerging Companies, both returning over 50%, or double the index return of 22.75%. Over 3, 5, and 7 years, the same trend is apparent. This applies across all equity peer groups. Manager and fund selection are critical to performance. Equally critical is the consistency of performance, as well as, when it occurs, the length and depth of any negative returns or drawdowns. Taking a single year or term, particularly looking through the rear-view mirror seems simple, and can be misleading and dangerous. For clear analysis of fund performance and risk across all peer groups, log on to FundMonitors.com to compare funds using our quant Star Ranking analysis across any of 16 different peer groups. Choose funds with a consistent rank of five, four, or even three stars across multiple time frames - particularly 5 or 7 years if applicable, to select an above "average" return. News | Insights Manager Insights | East Coast Capital Management 2025 Responsible Investment and Stewardship Report | 4D Infrastructure Property Update | Australian Secure Capital Fund January 2026 Performance News Bennelong Emerging Companies Fund DAFM Digital Income Fund (Digital Income Class) Insync Global Capital Aware Fund |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |

27 Feb 2026 - Performance Report: Equitable Investors Dragonfly Fund

[Current Manager Report if available]

27 Feb 2026 - Performance Report: Insync Global Quality Equity Fund

[Current Manager Report if available]

26 Feb 2026 - Performance Report: Insync Global Capital Aware Fund

[Current Manager Report if available]

26 Feb 2026 - How investors can still ride the gold surge

How investors can still ride the gold surgePendal February 2026 (5 minutes read time) |

|

GOLD and silver prices have been riding a rollercoaster since the start of the year, but Pendal portfolio manager Brenton Saunders -- who has worked as a geologist -- argues there are still plenty of opportunities in midcap equities exposed to these metals. Total gold demand in 2025, including over-the-counter sales, exceeded 5,000 tonnes for the first time, according to the World Gold Council (WGC). Last year, the safe-haven metal set 53 new all-time price highs which yielded an "unprecedented value" of US$555 billion - a 45 per cent year over year increase, WGC data shows. The reason: heightened investment activity driven by safe-haven and diversification moves that culminated in the second strongest year on record for exchange traded fund-inflows and elevated central bank buying. Although central bank purchases slowed from their recent pace, they hit the upper end of the WGC's forecast, totalling 863 tonnes for the year. Bar and coin buying also reached a 12-year high. This led to the gold price marking its highest annual average at US$3,431 an ounce - a 44% spike year over year. "Central banks have been buying it hand over fist; retail investors have been buying it hand over fist, the dollar has been weakening, and geopolitics have been pretty elevated," explains Saunders, who manages Pendal's MidCap Fund. "If you go back to the late 90s/early 2000s central banks were all selling gold. It was an old asset. Nobody needed it anymore. It was defunct," explains Saunders. "Most of the OECD countries sold most of their gold reserves. The US was probably the only one that didn't. "But now you've seen a very broad-based and especially emerging market purchase of gold. So it's re-legitimised gold in a major way in terms of its role as a reserve asset the world over." Silver, meanwhile, is also a beneficiary of the market ructions, hitting its highest point on record in late January when it rose above US$120 an ounce. An additional key driver of the recent price surge in gold's poorer cousin is the high demand for silver as an industrial metal input for solar panels. "We now use a lot of it, especially in solar panels," says Saunders. "That's probably the biggest industrial use for silver now, but it's always been a second-tier reserve currency investment product that has done the rounds. "So it's move more recently is obviously being helped by the fact that solar manufacturing is still elevated and now we've seen some investment demand come to the fore." But while gold and silver prices have run hard, this hasn't necessarily been reflected in the share prices of gold and silver stocks. 'Scepticism gap'Saunders points to the 'scepticism gap' between the price of the physical metals versus the equities exposed to them. "Because the move in the gold price has been so rapid the market has been highly sceptical of pricing in that scenario because they're constantly questioning what will happen if the gold price comes back. "So the equities, not just gold equities but especially in gold, have been quite reticent to reflect in their share prices the full move in the gold price." However, Saunders argues that the price could drop by US$1,000 and still be at a "bonanza level", meaning gold-exposed companies "could weather quite a big correction in the gold price without much impact to the value of the company's operational considerations". A "bonanza-level" gold price affords operations more flexibility, allowing them to mine areas that historically were not economic to consider. This increases reserves and profitability. "That is the one thing that gives me a bit of comfort, and I think investors ultimately a bit of comfort," says Saunders. "If I look at consensus earnings for gold companies, they're still reflecting a significantly lower gold price than prevails today. "So that should mean if the gold price stays at the current level, we'll continue to see earnings upgrades and that normally underpins share prices. "Those are the things that make me hopeful that it should still be a fairly constructive sector from an investment perspective." |

|

Funds operated by this manager: Pendal MicroCap Opportunities Fund , Pendal Global Select Fund - Class R , Pendal Sustainable Australian Fixed Interest Fund - Class R , Pendal Focus Australian Share Fund , Pendal Horizon Sustainable Australian Share Fund , Regnan Credit Impact Trust Fund , Pendal Sustainable Australian Share Fund , Pendal Sustainable Balanced Fund - Class R , Pendal Multi-Asset Target Return Fund |

|

This information has been prepared by Pendal Fund Services Limited (PFSL) ABN 13 161 249 332, AFSL No 431426 and is current as at December 8, 2021. PFSL is the responsible entity and issuer of units in the Pendal Multi-Asset Target Return Fund (Fund) ARSN: 623 987 968. A product disclosure statement (PDS) is available for the Fund and can be obtained by calling 1300 346 821 or visiting www.pendalgroup.com. The Target Market Determination (TMD) for the Fund is available at www.pendalgroup.com/ddo. You should obtain and consider the PDS and the TMD before deciding whether to acquire, continue to hold or dispose of units in the Fund. An investment in the Fund or any of the funds referred to in this web page is subject to investment risk, including possible delays in repayment of withdrawal proceeds and loss of income and principal invested. This information is for general purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. It has been prepared without taking into account any recipient's personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation. The information may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information is complete and correct, to the maximum extent permitted by law neither PFSL nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information. Performance figures are calculated in accordance with the Financial Services Council (FSC) standards. Performance data (post-fee) assumes reinvestment of distributions and is calculated using exit prices, net of management costs. Performance data (pre-fee) is calculated by adding back management costs to the post-fee performance. Past performance is not a reliable indicator of future performance. Any projections are predictive only and should not be relied upon when making an investment decision or recommendation. Whilst we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections. For more information, please call Customer Relations on 1300 346 821 8am to 6pm (Sydney time) or visit our website www.pendalgroup.com |

25 Feb 2026 - Performance Report: DAFM Digital Income Fund (Digital Income Class)

[Current Manager Report if available]

25 Feb 2026 - The rise of grounded sustainability and why it's here to stay

|

The rise of grounded sustainability and why it's here to stay abrdn February 2026 (4-minute read) In the five years since the Glasgow-based COP26, sustainable investment initially surged. Expectations were high, pledges were ambitious, and many believed capital markets could play a decisive role in addressing climate change and broader environmental and social challenges. But more recently, geopolitical shocks, legal scrutiny and market realities have tempered that optimism. In its place, a more durable approach is emerging, which we describe as grounded sustainability. It's a framework for incorporating sustainability factors into investment decisions, where those factors are financially material and aligned with client mandates. It's evidence-led and recognises inherent trade-offs. Importantly, it's clear about the limits of what investors and companies can achieve within the constraints of public policy. Mandates and market realitiesOver the past five years, conflicts, the global energy crisis, and the resurgence of populist politics have created a more fragmented, unpredictable and idiosyncratic environment. For example, coal use rose during the energy crisis, even as renewable deployment consistently exceeded expectations. This highlights the growing regional and thematic divergence. With this complex backdrop, sustainable investment must balance long-term systemic goals with the constraints imposed by mandates, markets and regulation. Ambition alone isn't enough. It must be combined with pragmatism. Importantly, it must also align with clients' financial objectives and constraints, otherwise commitments risk becoming empty promises - or worse, reputational liabilities. Climate law gets real: from global duties to corporate liabilityLegal frameworks are catching up with climate ambition. The International Court of Justice's (ICJ) recent advisory opinion [1] clarifies that states have a legal duty to prevent environmental harm, including to the climate system. It also clarifies that a lack of regulation doesn't absolve other actors - whether companies, asset managers or investors - from managing foreseeable risks. This shifts climate accountability from voluntary action to legal risk. Policy as a catalystThis is where effective policy matters. Recent European initiatives to align climate objectives with industrial competitiveness and energy security reflect growing recognition that markets alone cannot deliver the transition at scale. Together, they signal a shift from fragmented initiatives to coordinated, state-backed action, while offering companies and investors the long-term policy clarity that has been missing. This is why we are calling for greater long-term policy certainty, which retains strategic intent while limiting unnecessary complexity. This is the essence of grounded sustainability: integrating environmental and social factors when they are material to value, and doing so with clarity, discipline, and alignment to mandates. What does this mean for investors?Sustainability concerns need not be sidelined in financially focused mandates. Forward-looking considerations of material environmental and social risks are fully consistent with long-term value creation. What cannot be justified is pursuing sustainability outcomes that are disconnected from financial objectives, unless explicitly agreed with clients. This is the essence of grounded sustainability: integrating environmental and social factors when they are material to value, and doing so with clarity, discipline, and alignment to mandates. Policy is the missing link. Without it, companies struggle to act without breaching fiduciary duties or losing market share. With it, sustainability themes become investable, scalable, and defensible. Looking forwardWe expect that the rise of climate risks - coupled with increasing energy and mineral demands to facilitate technology advances and the energy transition - will mean that sustainability themes will remain at the heart of many geopolitical tensions. This will apply whether they are presented as energy transition, resilience or strategic government objectives (such as economic competitiveness or national security). Overall, we expect the policy landscape to remain uneven, with less support than previously. But where outcomes align with strategic government objectives, policy support will surely follow. Final thoughts...A recalibration is needed to find an equilibrium, where sustainability is seen as a fundamental tool for making better investment decisions, rather than being wrapped up in unrealistic expectations. The sector needs to evolve from idealism to pragmatism, grounded in legal clarity, mandate alignment and financial materiality. Despite the potentially gloomy outlook, we've seen record investment in the energy transition - twice as much as in fossil fuels. So it's not about abandoning sustainability themes. Rather, it's about doing it deliberately and within real-world constraints. |

|

Funds operated by this manager: abrdn Sustainable Asian Opportunities Fund , abrdn Emerging Markets Equity Fund , abrdn Sustainable International Equities Fund , abrdn Global Corporate Bond Fund (Class A) |