News

12 Mar 2026 - Performance Report: Altor AltFi Income Fund

[Current Manager Report if available]

11 Mar 2026 - Performance Report: Airlie Australian Share Fund

[Current Manager Report if available]

11 Mar 2026 - Beyond scale: rethinking the engine room of European infrastructure

|

Beyond scale: rethinking the engine room of European infrastructure abrdn February 2026 (4-minute read) The prevailing narrative in infrastructure favours scale. Large funds, large assets, and large ambitions dominate the conversation. Yet, as Europe's energy transition continues and policy reforms reshape the investment landscape, it's increasingly clear that meaningful progress is being driven by the small- and mid-cap segments. Transactions below €500 million account for the majority of European infrastructure deals. This is the centre of gravity for new investment and innovation. Our experience over more than a decade - with around €3 billion invested across energy, transport and digital infrastructure - consistently points to the same conclusion. The lower mid-market is where policy ambition, operational delivery and investor returns align most effectively. There's less need for intermediaries, and it's materially less competitive. This gives space for genuine value creation, rather than simply financial engineering. Policy tailwinds and competitive advantageRecent reforms in the EU's market design for electricity, quicker permit approvals, and the Net-Zero Industry Act have shifted the balance in favour of assets that can adapt quickly and align with local policy priorities. Small- and mid-cap platforms have a structural advantage. In practice, this means utilities that work constructively with municipalities, transport assets embedded within national and regional strategies, and energy platforms that can adapt business models as subsidy regimes and security-of-supply priorities evolve. Large, centralised assets often struggle to respond at this pace. Risk, value and evidenceThe notion that smaller assets are riskier doesn't stand up to scrutiny. In regulated sectors, risk is defined far more by framework stability and governance quality than by asset size. Our utility investments in Finland, for example, operate under the same regulatory regimes as larger peers, yet benefit from more conservative capital structures and greater scope for hands-on asset management. Agility, local solutions and systemic changeSmall- and mid-cap assets move at a different pace. Development timelines are shorter, adaptation is faster, and innovation is less encumbered by bureaucracy. In Finland, this has enabled the rapid deployment of electric boilers to exploit periods of low-cost renewable power, the co-location of data centres to capture waste heat, and the diversification of fuel sources within district heating networks to improve resilience. These initiatives were delivered through close engagement with management teams and local authorities, and implemented within months rather than years. Final thoughts...The infrastructure required to support Europe's changing economy won't be delivered solely by megaprojects or flagship assets. It will be built incrementally, through thousands of local decisions across infrastructure systems. It will also be shaped by those who can combine agility, results, and local insight to deliver measurable outcomes - especially as policy and competitiveness trends continue to evolve. |

|

Funds operated by this manager: abrdn Sustainable Asian Opportunities Fund , abrdn Emerging Markets Equity Fund , abrdn Sustainable International Equities Fund , abrdn Global Corporate Bond Fund (Class A)

|

10 Mar 2026 - Performance Report: Quay Global Real Estate Fund (Unhedged)

[Current Manager Report if available]

10 Mar 2026 - Performance Report: Bennelong Concentrated Australian Equities Fund

[Current Manager Report if available]

10 Mar 2026 - Ben McVicar discusses the data centre effect

|

Ben McVicar discusses the data centre effect Magellan Investment Partners February 2026 (6-minute read) |

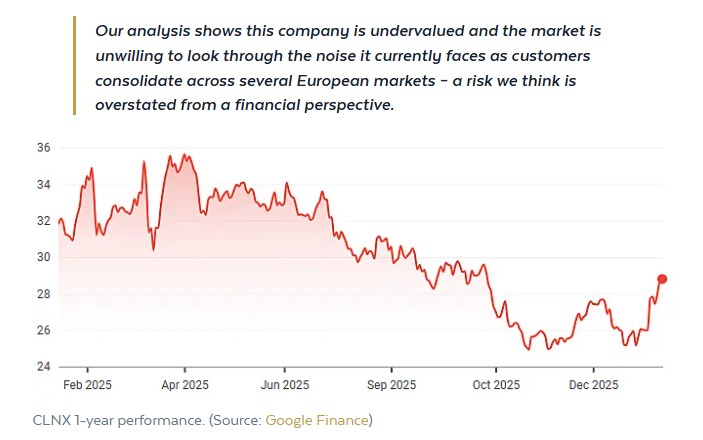

Power demand is rising again. And this time, it is not a short-term cycle.Ben McVicar, Co-Head of Infrastructure and Portfolio Manager at Magellan, sees a decisive shift underway. "There's an upswing in power demand that is data centre related." After more than a decade where electricity demand barely moved, data centres are changing the equation. Systems that once operated in a world of flat consumption are now under pressure to expand capacity and fund the next wave of build-out. That shift matters. In this Q&A, McVicar explains where he believes the market is misreading the landscape, how supply constraints are shaping investment decisions, and why patience remains a competitive advantage. What's your most recent investment and why?We operate a low-turnover portfolio, but one of the more substantial positions we have entered of late is Cellnex (BME: CLNX). The business is the largest mobile tower company in Europe.

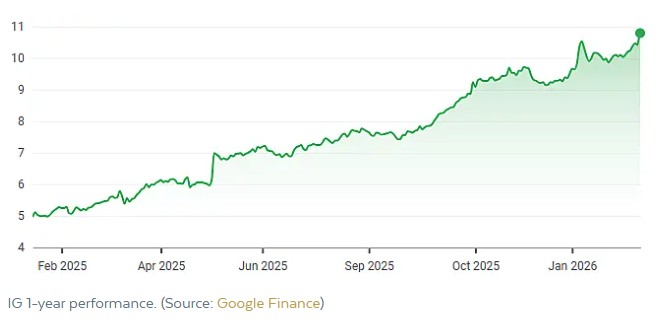

Which investment did you add to your watchlist this week?We have a universe of about 130-140 companies. It's a tightly defined list, so not a lot falls in and out often. These are all high-grade infrastructure companies that have met the quality thresholds we require. So the watch list doesn't change too much. But things move up and down on our radar. The companies highest on our radar are the mobile phone tower companies like Cellnex, but also its peers across the Atlantic. What is the most recent investment you have trimmed or sold and what drove this decision?We have trimmed our position in Italgas (BIT: IG) after a very strong run. This is a gas utility in Italy that is run by a very strong management team. They acquired the second-largest gas network in Italy and expect to create significant synergies from the combined company. But as the price has gone up, the opportunity has narrowed.

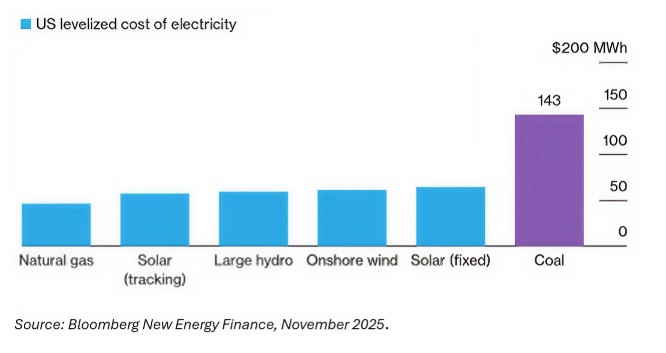

What's your favourite chart or data point from this week?

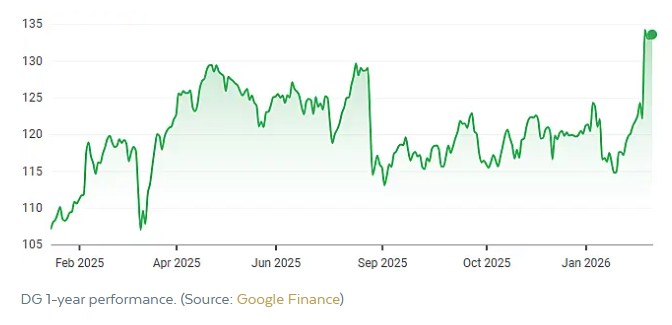

This shows the levelised cost of energy estimates. There's an upswing in power demand that is data centre related. This is a change from the 2005-2020 experience, where power demand growth was limited. This is leading to pressure to develop new power capacity. Gas generation is viable but constrained by supply chain bottlenecks. This makes renewables the most cost-effective and available source of new power. Combined with national and corporate carbon targets, this explains the ongoing investment we're seeing in the technologies. What was your weekly high - a standout market moment or highlightVinci (EPA: DG), a French infrastructure and contracting business, went up almost double-digit on its results. This is a long-standing position, and we've added to it during dips caused by French political turmoil. It's good to see the market focused on the robust fundamentals of this business.

What was your weekly low - a market disappointment or challenge?Customer power prices have gone up as demand has gone up in many regions. In the US utilities, we're diving into the risks and opportunities that come from the outlook of customer rate affordability and the impacts of an election year in many states. What first drew you to markets and what continues to keep you inspired today?I knew I wanted to be an investor before I even started uni. The craft of investing, finding opportunity and building a portfolio to take advantage of these opportunities while managing risk is an endlessly interesting job to be in. What's one piece of advice you'd give to new investors?Be patient, don't overestimate your abilities and wait for the opportunity that jumps off the page at you. You'll know it when you see it. How do you unwind when you're not thinking about the market?Why would you do that? But seriously, exercise. I find I need active 'rest' to stop me thinking about different opportunities or problems I'm focused on in markets. Rapid fire!Favourite investing book? Snowball by Alice Schroeder. Favourite investing or finance/markets-related podcast? I enjoy listening to learn new ideas - the Knowledge Project Podcast (Shane Parish). The first thing you read each morning? I check how the portfolio is trading and then get onto the international press (FT, etc.). Favourite restaurant? Continental Deli - Newtown. Something people are surprised to learn about you? I first started dating my (now) wife when I was 16 and she was 15. I get the impression it's unusual for my generation! |

|

Funds operated by this manager: Magellan Global Fund (Open Class Units) ASX:MGOC , Magellan Infrastructure Fund , Magellan Global Opportunities Fund No.2 , Magellan Infrastructure Fund (Unhedged) , Magellan Global Fund (Hedged) , Magellan Core Infrastructure Fund , Magellan Global Opportunities Fund Active ETF (ASX:OPPT) Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 trading as Magellan Investment Partners ('Magellan Investment Partners') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to a Magellan Investment Partners financial product may be obtained by calling +61 2 9235 4888 or by visiting www.magellaninvestmentpartners.com Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of a Magellan Investment Partners financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. No guarantee is made that such information is accurate, complete or timely and no warranty is given regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Magellan Investment Partners or the third party responsible for making those statements (as relevant). Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Magellan Investment Partners will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material. Any third-party trademarks contained herein are the property of their respective owners and Magellan Investment Partners claims no ownership in, nor any affiliation with, such trademarks. Any third-party trademarks contained herein are the property of their respective owners, are used for information purposes and only to identify the company names or brands of their respective owners, and no affiliation, sponsorship or endorsement should be inferred from such use. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan Investment Partners. (080825-#W17) |

9 Mar 2026 - Performance Report: 4D Global Infrastructure Fund (Unhedged)

[Current Manager Report if available]

9 Mar 2026 - Performance Report: Bennelong Australian Equities Fund

[Current Manager Report if available]

6 Mar 2026 - Hedge Clippings |06 March 2026

|

|

|

|

Hedge Clippings | 06 March 2026

This week we interviewed two small cap managers via Zoom: Dean Fergie from Cyan Investment Management, and Martin Pretty from Equitable Investors, to get their take on the recent reporting season, which in a word, if you hadn't noticed, was volatile. You can view the video here, or from the summary below. Wilsons Advisory noted when only halfway through reporting season that: "Even modest earnings surprises triggered double-digit share-price moves, reflecting stretched valuations, shifting sector leadership, and heightened sensitivity to forward guidance rather than historical results. Several large-cap companies moved sharply on the day of their results, with investors reacting quickly to any deviation from expectations. By the end of the month, as reporting drew to a close, the volatility and market's reactions had only increased, with an overall backdrop of the negative effects of AI - or at least concerns about overly stretched valuations as a result of the euphoria of the past couple of years since Chat GPT and others changed the world as we knew it, along with the ongoing strength of rare earths and precious metals, and the sagging price of Bitcoin and other cryptocurrencies. The consensus - in the true sense of the word as both Dean and Martin were each in agreement on almost all points - was that many companies with "stretched" valuations didn't front up to investors' expectations. On the upside, companies which had possibly been considered boring, or not on the AI wagon, caught the market's attention. The discussion ranged not only from "what's" driving the market, but also the "who" - to what extent are index funds and program trading having an outsized effect, and how much influence are short terms traders seeking a quick killing having? In any event, the ASX 200 total return as a whole rose by 4.11%, taking it to +16.19% for 12 months, (whilst the more volatile Small Ordinaries fell by 2.8%), or the S&P 500 which fell by 0.76% in February, but also rose by 16.99% YoY. From a fund manager's perspective it was either a difficult, or spectacular month, along with plenty in between, based on the ~30% of funds that have reported to date, with returns ranging from -11% through to +11%, further emphasising our point from last week that active management can have an outsized effect on investors returns - provided you choose the right manager, with the right strategy, and at the right time! We originally scheduled the video with Dean and Martin before the US and Israel unleashed their joint air attacks on Iran last Saturday. Since then of course global volatility and uncertainty has also been unleashed, creating a whole different set of uncertainties, and possibly some opportunities for investors and fund managers alike. Uncertainty flowed through to the RBA as well, with Governor Michele Bullock keeping her options open on the chance of a rate rise in less than two weeks time, ahead of the next monthly CPI number due on 25th of March. However, in the current global environment, those two weeks leave an awful lot of variables, and potential outcomes, which could come into play. News | Insights Manager Insights | Cyan Investment Management & Equitable Investors Data demand heats up | Magellan Investment Partners February 2026 Performance News |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |

5 Mar 2026 - From Record Issuance to Renewed Opportunity: European & Australian ABS in Focus

|

From Record Issuance to Renewed Opportunity: European & Australian ABS in Focus Challenger Investment Management February 2026 (9-minute read) 2025 Wrap-up and 2026 Outlook2025 closed as another strong year for the European and Australian ABS markets despite intermittent macro uncertainty. Investors continued to demonstrate robust demand, supporting spread compression amid record issuance volumes. For 2026, we expect elevated funding needs and stable performance across core collateral types, alongside ongoing innovation in new and esoteric asset classes. Regulatory changes in Europe may further encourage issuance and broaden the investor base. Overall, floating rate securitised assets remain a compelling component of diversified fixed income portfolios, continuing to offer an attractive spread pick up to similarly rated corporates, floating rate protection, and structural resilience. Issuance and Market TechnicalsAs we mentioned in our European and Australian ABS 2025 Q3 update, a strong start to 2025 was halted when broader markets faced uncertainty in early April given President Trump's tariff announcements. The ABS markets recovered relatively quickly and despite continued macro and tariff related uncertainty, demand across the capital structure continued to be strong, leading to spread compression across global ABS markets. Sustained investor demand and relatively attractive funding levels continued to keep the asset class attractive for issuers for both funding as well as for credit risk transfer. So...another record-breaking year for issuance? Indeed, although slightly less dramatic than in 2024. European ABS issuance closed the year just over €95bn and Australia continued momentum with another year of strong issuance for the market at just under €41bn, the second highest year of issuance, and a little short of the record set in 2024 of €46.5, according to JPM research figures. The supply we have seen in Europe and Australia over the last couple of years has led to an outstanding market size of just under €700bn publicly available/distributed bonds excluding CLOs. This underlines ABS as a significant sector within fixed income markets. Similarly, since the GFC, the Australian securitisation market has demonstrated steady, consistent growth, but the recent acceleration signals robust investor appetite combined with increased supply from a growing non-bank issuer base. In addition, JPM research notes that both the European and Australian markets finished the year with not just record issuance but also positive net supply: net distributed European and Australian ABS issuance reach +€19.3bn and +€6.4bn, respectively, for FY 2025. A healthy securitisation market is one where innovation and new asset classes emerge, and 2025 did not disappoint. Europe has continued to see stable issuance from traditional mortgage and consumer collateral sectors but there was also a significant number of new deals and issuers which debuted in the market, giving investors a good source of diversity across platforms and collateral types. In Australia, while RMBS continued to dominate supply last year, non-RMBS issuance has grown significantly with sizeable volumes of auto/equipment issuance over recent years and more non-bank lenders in the consumer and SME space adding greater diversity. Liquidity in the asset class, globally, continued to show resilience, demonstrated by secondary market depth and investor demand even through significant bouts of market volatility such as that seen in April. Some examples of this:

For 2026, we anticipate the need for funding and reinvestment to continue and issuance to remain elevated. If the current environment persists all signs are pointing to the potential for another record year! We expect strong demand for the asset class to persist and increased origination in traditional consumer underlying assets as well as newer types of collateral to support growth in the asset class. Despite potential macroeconomic volatility, the sector's resilience and the stable investor base make it well placed for the sector to continue. Asset PerformanceHeadline fundamentals stayed healthy in 2025 year but were accompanied by a side of tiering - both for consumer as well as levered corporate performance. Capital market volatility, macroeconomic uncertainty and credit stories such as Tricolour emerging in the US kept investors on their toes but structured finance ratings were largely stable through 2025 maintaining a stable to positive ratings drift. Looking forward, the performance outlook for most collateral types is expected to be stable but we remain mindful of macro and interest rate uncertainty for consumer and corporate borrowers. Despite global central bank rates continuing to reduce from their 2024 peaks during 2025, interest rates are persisting in a higher for longer phase compared to pre-Covid levels, particularly as inflation has remained somewhat "sticky" during 2025. Investors should be focused on limiting risks around macro-led shocks to borrowers by analysing collateral through the interest rate cycle, keeping in mind the key issue of affordability for customers and the importance of strong, effective underwriting by issuers. Unemployment indicators continue to drift upwards and remain front of mind for investors looking for read across into consumer credit performance. Esoteric and new asset classes were a key theme in 2025Clearly, securitisation continues to be a key funding tool for traditional consumer and mortgage asset classes, but the past few years have seen exciting developments in new collateral types coming to market. Funding levels in structured finance are attractive for issuers and these new sectors have generally been received well by the market. Additionally, through 2025 we noted a number of new issues in sectors with positive ESG characteristics and considerations. These include solar and heat pump ABS as well as later life mortgages and transactions described as shariah compliant RMBS on the social side. EV auto financing continues to be a growing segment within Auto ABS portfolios. Risks and Opportunities in 2026:Macro and geopolitical risks continue: Writing this just a couple of weeks into 2026, political and geopolitical risks continue to be front-of-mind for market participants. We expect this dynamic to persist this year and for investor sentiment to remain sensitive to developments in geopolitics, global trade policy as well as the path of interest rates in the US and in Europe. Consumer performance: Structural protection in ABS structures mitigate risks In Europe, consumers continue to face structural and cyclical risks, being described as financially resilient but behaviorally cautious. However, expectations for unemployment to remain broadly stable maintains a base for low and stable credit card and ABS arrears performance. We do expect tiering to continue between better quality prime collateral and more non prime lenders who support underserved borrowers. Structural protections afford to investors in securitised structures, help mitigate risk, often with increasing protection over time as transactions or assets de-lever. Housing Market Valuations: Asset prices, in particular housing, in the UK, Australia and Europe remain on a stable or improving trend given the consistent undersupply seen in construction of housing seen across the major RMBS markets together with continued increase in demand. Where there has been some slowing in segments of the market, in the UK for example, with London apartment valuations facing pressure, we note that the Buy to Let RMBS performance remains consistent given stable unemployment and rental streams. Any unforeseen shock to unemployment or regulatory impacts are key to performance but, post GFC affordability regulations and appropriate stress testing of borrowers' together with stability in underwriting gives investors comfort beyond the structural features of RMBS. Amongst and despite the risks above we note some significant opportunities for experienced investors in Global structured finance markets: New and Esoteric Asset Classes: As noted above, we have seen issuance beyond traditional platforms over the last couple of years emerging. The use of securitisation as a funding tool beyond "on the run" platforms is valuable to investors. New issuers to the market, including those establish issuers that diversifying their funding via securitisation, and collateral types in Europe and Australia present opportunities to earn a premium over more traditional platforms and provide diversity to portfolios. That said, we should be cognisant of potential additional risks that may need to be considered relating to new lending types as well as the short historical performance available for some types of collateral which is needed to structure, rate and stress transactions appropriately. European Markets give investors depth, diversity and Liquidity We continue to see opportunities in the European ABS and CLO markets with an overall size of over €600bn now, the market gives investors good relative value where diversity of jurisdictional collateral risk alongside strong historical performance. This is all within the context of a dedicated investor base and proven liquidity in the asset class. Regulation, regulation, regulationRegulation will remain a key consideration in 2026, particularly in Europe, where the European Securitisation legislation aims to reduce barriers to issuance and investment in EU securitisation:

Collectively, these developments should improve funding conditions and make securitisation more attractive to a broader investor base albeit with a fluid timeline. Implications of the motor finance commission rulings for UK Auto ABSThe FCA consultation on motor finance broker commissions is still ongoing, but any impact on ABS has been limited and if the redress scheme is as expected, focussed on discretionary commission arrangements, we expect little to no impact on new and outstanding UK auto asset-backed securities (ABS) transactions as a negligible amount of collateral in outstanding securitised bonds would be affected. Secondary liquidity was more challenged until more clarity was reached. Issuance in UK Auto ABS across bank and non-bank lenders, was €3.6bn in 2024 compared to 2025 where no issuance at all was seen until September, when VW opened the market and priced well with strong demand. As we noted in one of our published articles at the time we expected this to be a positive signal for UK non-bank lenders, giving them confidence in execution. Indeed, Oodle came with a Dowson transaction soon after which was taken well by the market. That said, given lower origination volumes over 2025 for the UK non bank lenders, particularly in the non prime space, funding needs may be more muted in 2026. It is also worth noting, that used car prices fell as supply of cars normalised post covid, residual values have also corrected back down; stabilising for ICE vehicles but falling sharply for EVs, where residual values proved significantly over forecast. Looking forward to 2026:The depth and diversity of the European and Australian markets continue to support the role of global securitised products as a strategic allocation within fixed income portfolio; enabling diversification across jurisdictions, collateral types and issuer profiles while maintaining liquidity. Looking forward, regulatory developments, continued innovation in collateral and an expanding issuer base should reinforce market depth and opportunity, making securitised credit not merely a tactical allocation but a durable, scalable and resilient cornerstone of fixed income portfolios in 2026 and well beyond. Challenger IM Credit Income Fund , Challenger IM Multi-Sector Private Lending Fund For Adviser & Investors Only Disclaimer: This material has been prepared by Challenger Investment Partners Limited (Challenger Investment Management or Challenger), ABN 29 092 382 842, AFSL 329 828. This document does not relate to any financial or investment product or service and does not constitute or form part of any offer to sell, or any solicitation of any offer to subscribe or interests and the information provided is intended to be general in nature only. This should not form the basis of, or be relied upon for the purpose of, any investment decision. This document is not available to retail investors as defined under local laws. This document has been prepared without taking into account any person's objectives, financial situation or needs. Any person receiving the information in this document should consider the appropriateness of the information, in light of their own objectives, financial situation or needs before acting. This document is provided to you on the basis that it should not be relied upon for any purpose other than information and discussion. The document has not been independently verified. No reliance may be placed for any purpose on the document or its accuracy, fairness, correctness, or completeness. Neither Challenger Investment Management nor any of its related bodies corporates, associates and employees shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of the document or otherwise in connection with the presentation. |