News

19 Mar 2026 - Performance Report: Insync Global Capital Aware Fund

[Current Manager Report if available]

19 Mar 2026 - Correlation and How to Think About Diversifying Alternatives

|

Correlation and How to Think About Diversifying Alternatives Fidante February 2026 (7-minute read) Achieving diversification and uncorrelated returns are a common objective when constructing investment portfolios. Understanding what those terms really mean is essential to properly appreciate how alternative investments can contribute to robust long-term portfolios.

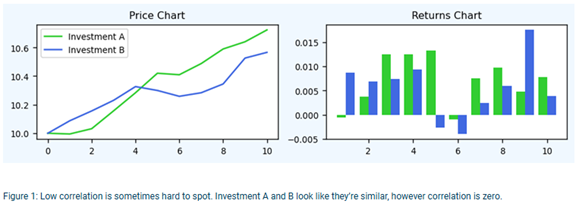

What is correlation?Correlation is a statistical measure of the relationship between the returns of two investments (rather than price levels). It ranges from -1 to +1. Investments with high correlation tend to move in the same direction at the same time, while investments with little or no correlation tend to move independently of each other. Negatively correlated investments tend to move in opposite directions. Importantly, two investments that both deliver positive long-term returns can nevertheless exhibit zero or even negative correlation. Conversely, investments that appear to move in opposite directions over time can be positively correlated. For example, daily price movements may show a very different relationship from the point to point one-year return. In figure 1, at first glance it may appear that the two investments shown in the left-hand chart below are positively correlated. After all, for the period shown, both have increased by about the same amount. Looking at the daily returns in the chart on the right, we can see that most days the two investments do indeed move up together, however, on some days they move in opposite directions. Counterintuitively, the correlation of these two strategies turns out to be zero. An important implication is that investors can derive diversification benefits from two investments that both go up over time.

It's also important to note that statistically high correlation does not imply causation. Just because two return series are highly correlated does not mean one necessarily causes the other to move. As a result, correlation can and does change over time.

Why does correlation matter?By combining uncorrelated investments, we can construct portfolios with lower risk and/or higher returns. This is the power of diversification. The lower the correlation between assets, the greater the potential benefit. This is where alternatives come in - no other asset class offers the same variety and breadth of uncorrelated investments as the universe of alternative investments.

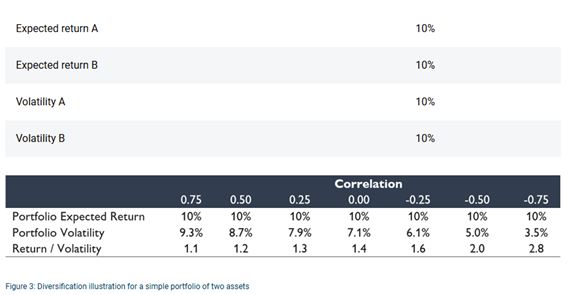

A simple illustrationTo see why uncorrelated assets produce better portfolios, consider two investments, A and B. Both are expected to return 10% per year and each has volatility of 10%.

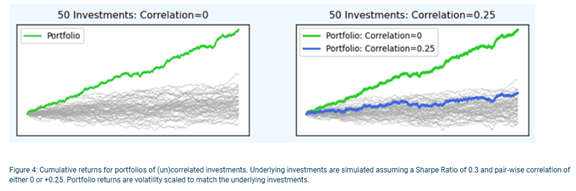

Figure 3 shows that when these investments are highly correlated, combining them does little to reduce portfolio risk. However, when correlation is low or even negative, portfolio volatility drops to levels far below that of either A or B individually, even though expected returns remain the same. This leads to higher risk adjusted returns - the portfolio earns the same return with less volatility. The effect becomes even more powerful in larger diversified portfolios. Consider an equally weighted portfolio of 50 completely uncorrelated investments, all with the same ex-ante expected return and ex-ante volatility and a modestly positive Sharpe Ratio2 of 0.3. The portfolio returns are shown by the green line on the left-hand chart, and the Sharpe Ratio is now 1.94, a significant improvement on any individual investment. However, even a small increases in correlation can significantly dilute these benefits. If these 50 investments now have a pair-wise correlation of 0.25 (still a relatively low correlation), the cumulative portfolio return becomes dramatically lower than when correlation was zero, as shown by the blue line in the right-hand chart. \While the above is a contrived example from a simulation, it illustrates just how powerful the combination of uncorrelated investments can be. This is where alternatives have the potential to play such an important role in investment portfolios.

In practice, it is extremely difficult to find large numbers of investments that are truly uncorrelated at all times. However, each additional uncorrelated investment introduced into a portfolio increases the potential diversification benefits for the portfolio. Alternative investments are often uncorrelated not only to traditional assets like equities and bonds, but also to each other, making a rich hunting ground for investors seeking to maximise the power of diversification. There is, however, an important caveat. Just as low or negative correlation enhances diversification, even small changes in correlation can undermine it, sometimes quickly and unexpectedly. What factors affect correlation?Correlation can increase during periods of market stress, economic shocks or major shifts in monetary policy. Events such as the COVID market sell off in early 2020 saw correlations spike as many assets moved sharply lower at the same time. Even if only temporary, this can have a devastating impact on portfolios if previously uncorrelated investments all move in the same direction at the same time. The experience of 2022 provided another stark example. Rising interest rates negatively affected both equities and bonds, causing the traditional 60/40 portfolio to suffer unusually large losses. Assets that investors expected to diversify one another instead moved together. Understanding the common drivers of returns is therefore critical when thinking about how correlation might change. When many investments rely on similar economic factors, such as low interest rates, correlation can rise sharply when those conditions change, as we saw in 2022. Some investors attempt to anticipate these shifts and rebalance portfolios accordingly. However, this can be difficult, so alternative investments that are less susceptible to correlation changes can be useful as 'anchor' diversifiers in a portfolio. The challenges of measuring correlation While uncorrelated investments can improve portfolio diversification and resilience, measuring correlation is not straightforward. There is no single measure to determine "true" correlation. Investors need to consider:

Useful techniques include examining rolling correlations, analysing how investments behave during market downturns and monitoring whether regime changes have altered the relationship between two investments. It's also worth remembering that correlation is only one part of the investment decision. Some investments may be attractive because of their risk/return profiles, even if diversification benefits are modest. Understanding the role of alternatives in diversification While investors often think about alternative investments as a single category, they can play very different roles within a portfolio. Broadly, alternatives can be grouped into three types based on their primary objective: growth alternatives, which aim to enhance overall portfolio returns; diversifying alternatives, which seek to improve risk adjusted returns by delivering low or uncorrelated performance; and defensive alternatives, which are designed to provide an explicit buffer during periods of market stress. Understanding these distinctions is critical, as the value an alternative investment brings depends not just on its standalone return, but on how it interacts with the rest of the portfolio. Correlation and diversification are particularly central to the second category of diversifying alternatives. Investments with low correlation can materially improve portfolio outcomes by reducing volatility without sacrificing expected returns. Diversifying alternatives can therefore allow investors to achieve better risk adjusted returns rather than simply higher absolute returns, improving the efficiency and resilience of the portfolio as a whole. In this sense, alternatives that consistently deliver diversification benefits can be among the most valuable long term building blocks in a well constructed investment portfolio. Final thoughts Correlation measures how investment returns move relative to one another, but it is not fixed and cannot be relied upon to remain stable. Because correlation is based on historical data, there is no guarantee that it won't change in the future. That said, portfolios constructed with investments with low correlation can deliver higher returns for a given level of risk than those with more highly correlated investments. Correlation can therefore be an essential part of assessing any potential investment and is of particular importance when considering alternative investments. A solid understanding of correlation, its applications and limitations allows investors to unlock the power of diversification. While correlations can change, alternative investments that deliver consistently low correlation to traditional assets can be particularly valuable in building more robust, resilient portfolios. 1Markowitz, H.M. (March 1952). "Portfolio Selection". The Journal of Finance. |

18 Mar 2026 - Performance Report: Seed Funds Management Financial Income Fund

[Current Manager Report if available]

17 Mar 2026 - Performance Report: Glenmore Australian Equities Fund

[Current Manager Report if available]

17 Mar 2026 - 10k Words | March 2026

|

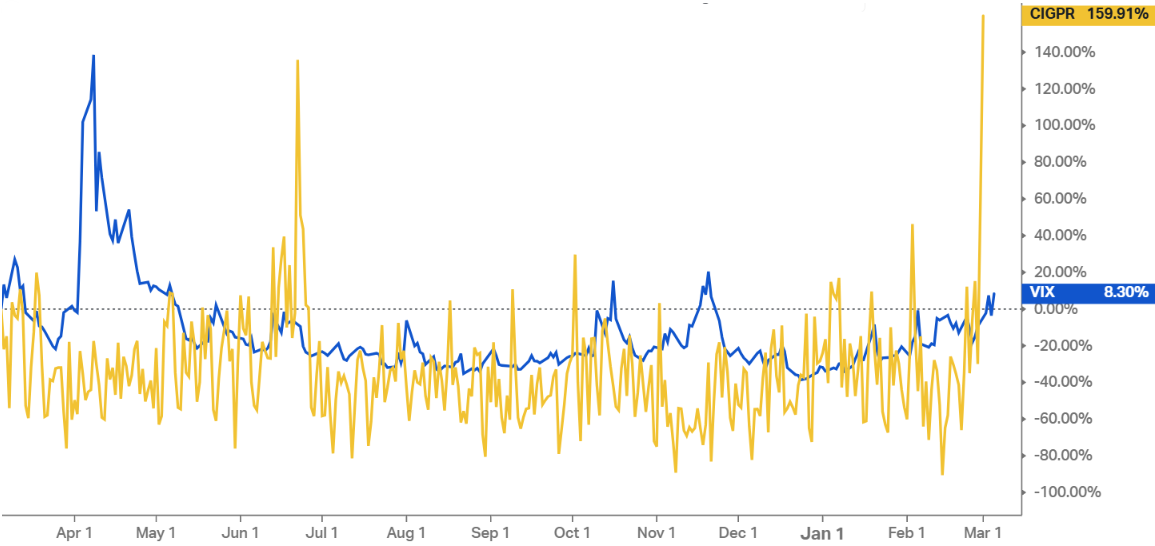

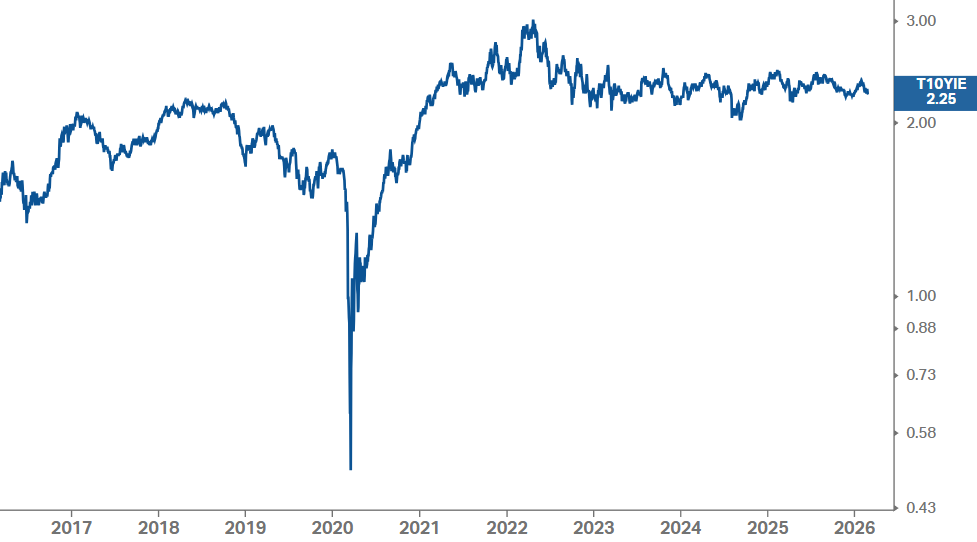

10k Words Equitable Investors March 2026 (2-minute read) Geopolitical risk spikes. After a long period of significant divergence, long term bond yields and forecast earnings yields have reunited. Worth considering alongside the relative performance of "Growth" v "Value". Long-term inflation expectations seem to have stabilised at higher levels than was the case pre-COVID - possibly baking in higher volatility in inflation. Military action swung equity investors straying to emerging markets back to the US. That US market may be concentrated but its a lot less concentrated than the ASX - and in the current period of turbulence concentration has performed very differently relative to equal-weight portfolios in the two countries. There does seem to be more interest in active investing currently. Finally, we can't escape without a chart on the decline of listed SaaS valuations - but in the context of a convergence with unlisted AI valuations. Geopolitical Risk Index relative performance to VIX (US volatility) over 1 year

Source: Caldara and Iacoviello, Koyfin US 10-year bond yield v S&P 500 forward earnings yield

Source: Yardeni Growth relative to Value (iShares Russell 1000 Growth / iShares Russell 1000 Value)

Source: Koyfin US 10-Year Breakeven Inflation Rate - relatively stable for past three years

Source: Koyfin Australian 10-year Breakeven Inflation Rate

Source: Equitable Investors, RBA CPI (Australia) - standard deviation of quarter-on-quarter change (rolling 30 quarters)

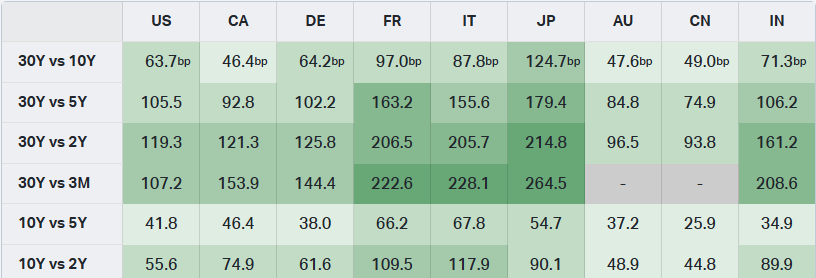

Source: Equitable Investors, ABS Global yield spreads matrix

Source: Koyfin S&P 500 relative to FTSE Emerging Index - reversal post Iran attack

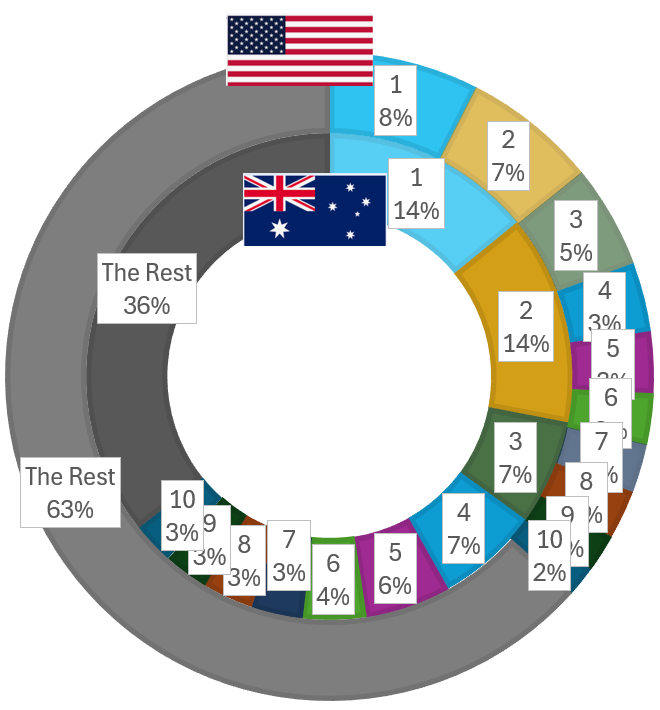

Source: Bloomberg Equities concentration - top 10 holdings' dominance of Aus and US major benchmarks (using iShares ETF proxies)

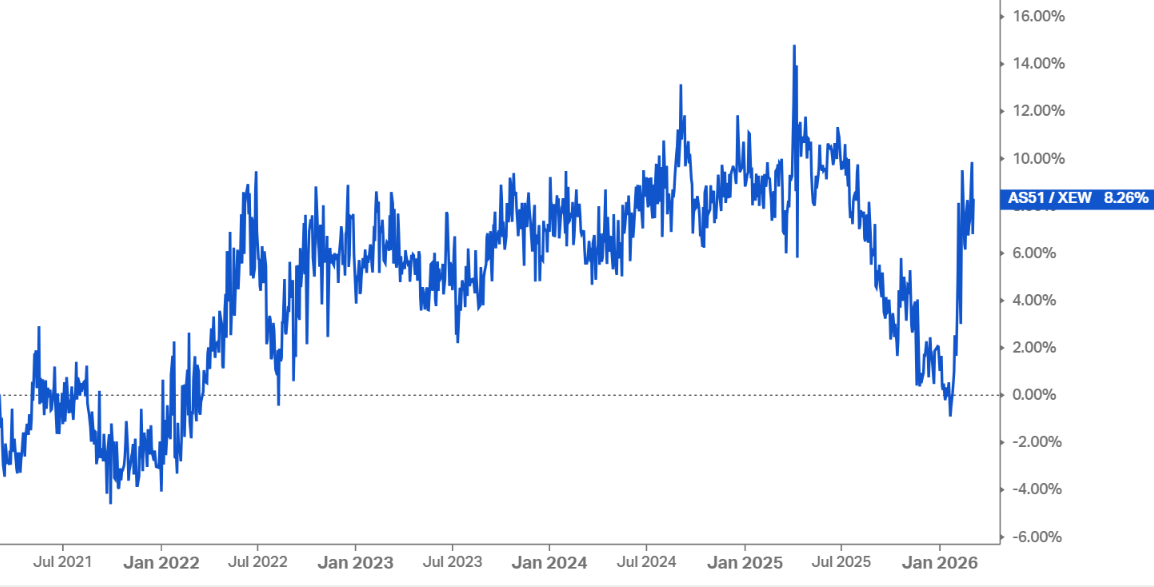

Source: Equitable Investors, Koyfin S&P/ASX 200 - Free-float weighted (AS51) v equal-weighted indices (XEW)

Source: Equitable Investors, Iress, Koyfin S&P 500 ETFs - Free-float weighted (IVW) v equal-weighted (RSP)

Source: Equitable Investors, Koyfin The number of active ETFs launched each year in the US

Source: Morningstar Public SaaS valuations have converged with AI-led software

Source: Arcadia Capital via Archtis Funds operated by this manager: Equitable Investors Dragonfly Fund Disclaimer Past performance is not a reliable indicator of future performance. Fund returns are quoted net of all fees, expenses and accrued performance fees. Delivery of this report to a recipient should not be relied on as a representation that there has been no change since the preparation date in the affairs or financial condition of the Fund or the Trustee; or that the information contained in this report remains accurate or complete at any time after the preparation date. Equitable Investors Pty Ltd (EI) does not guarantee or make any representation or warranty as to the accuracy or completeness of the information in this report. To the extent permitted by law, EI disclaims all liability that may otherwise arise due to any information in this report being inaccurate or information being omitted. This report does not take into account the particular investment objectives, financial situation and needs of potential investors. Before making a decision to invest in the Fund the recipient should obtain professional advice. This report does not purport to contain all the information that the recipient may require to evaluate a possible investment in the Fund. The recipient should conduct their own independent analysis of the Fund and refer to the current Information Memorandum, which is available from EI. |

16 Mar 2026 - Performance Report: Bennelong Emerging Companies Fund

[Current Manager Report if available]

13 Mar 2026 - Hedge Clippings |13 March 2026

|

|

|

|

Hedge Clippings | 13 March 2026

"It never rains, but it pours" is an old phrase that comes to mind when considering markets and global politics at present. AI, which had been driving sections of the market (and the market as a whole) since it was launched in the form of ChatGPT in November 2022, has seemingly turned from being a positive, and now reflects many of the risks (disruption, employment, capex, energy). Market darlings, such as Aussie home grown Atlassian, are indicative as they announced layoffs of 1600 staff this week, and have seen their share price fall from a peak of US$483 in October 2021, to below $75 as of now. Meanwhile, to the end user, AI's benefits are being implemented into everyday business operations at an amazing pace. Closer to home, February's reporting season was one of the most volatile on record. Two thirds (66%) of funds' performance numbers have been received to date, with wild fluctuations thanks to an ASX reporting season which provided plenty of surprises - both to the upside and on the downside. Overall, the ASX 200 Total Return (TR) index rose 4.11%, while the ASX Small Ordinaries (TR) fell by 2.57%. In this environment, many active equity managers struggled, while others, (although only 10% outperformed the ASX 200 TR) produced some impressive numbers. For the month, returns ranged from -21% (digital) through to +13.29% (not surprisingly, a global gold fund, Argonaut) reflecting their respective underlying asset or market sector. Over 12 months that became even more pronounced, with returns ranging from -53% (digital again) through to +233% (gold and key minerals again). While these outliers were obviously driven by headwinds or tailwinds respectively, between the extremes, a combination of strategy, sector, peer group, and most importantly, old fashioned manager skill, determined the outcome. Of interest was the appearance in February's top performers of Japanese Equity funds (average 12.10%), and Infrastructure Funds (average February return of 7.73%), while Managed Futures (Winton +5.05% and ECCM +4.59%) also stood out, alongside the inevitable gold, precious metals, and resources funds. Meanwhile the world suffers financial upheaval. If the rotation out of tech in the US, along with February's reporting season, weren't enough to throw markets into a turmoil, the US and Israeli attack on Iran completed the perfect storm. Somehow ("I'll end all wars") Trump seemed to think US arms and firepower would quickly bring the Iranian regime, and its 90 million + inhabitants to their knees begging forgiveness. He is obviously not a student of history when it comes to US overseas military endeavours, including Vietnam, Iraq, and Afghanistan, all of which (for the US at least) ended badly. This one is yet to play out, but whatever Trump claims, "quick" and "victory" seem a while away. Closer to home. We had the pleasure of interviewing George Bory from Allspring this week, a US$485 billion manager of Global Income funds and strategies being distributed in Australia by the team at Bennelong Funds Management. We managed to cover not only Allspring's and George's approach to bond investing - "Manage risk, rather than avoid it" - through to the current situation in the Middle East and its potential economic outcome, and finally the outlook for the US given the mid term elections which may or may not clip Trump's wings somewhat. You can see the full video here, or view the individual sections. Next week there's an RBA board meeting on Monday and Tuesday. As if things weren't complex and difficult enough already! We'll be joined as usual by our resident experts Nick Chaplin from Seed Funds Management and Renny Ellis from Arculus, to preview what they think the RBA is likely to do, and what they should do - which of course might be completely different. News | Insights Manager Insights | Allspring Global Investments Ben McVicar discusses the data centre effect | Magellan Investment Partners February 2026 Performance News Bennelong Concentrated Australian Equities Fund |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |

13 Mar 2026 - Beyond 'Quality at any price'

12 Mar 2026 - Performance Report: ECCM Systematic Trend Fund

[Current Manager Report if available]

12 Mar 2026 - When Geopolitics Moves Markets, Most Portfolios Aren't Ready

|

When Geopolitics Moves Markets, Most Portfolios Aren't Ready East Coast Capital Management March 2026 3-minute read There is a particular kind of market risk that doesn't show up cleanly in a spreadsheet. It doesn't follow earnings seasons or central bank calendars. It arrives through a headline, a border dispute, a sanctions announcement - and by the time most investors have processed it, the repricing has already begun. Geopolitical risk is not new. But the current environment has a different character to it. What we are seeing is not a series of isolated shocks, but an accumulation of structural pressures: fractured supply chains, sustained conflict, and policy unpredictability operating simultaneously across multiple geographies. That combination has a way of staying in markets longer, and running deeper, than a single event. The question for investors is not whether this will eventually resolve. It's whether their portfolios are positioned to navigate the period before it does. What Markets Are Actually Signalling In periods of genuine geopolitical stress, the signal tends to show up in commodities and currencies before it surfaces in equities. Energy markets become a key transmission mechanism: oil price volatility doesn't just reflect supply anxiety, it flows directly into inflation expectations, corporate cost structures, and consumer sentiment. We have seen exactly this dynamic play out. Supply disruptions have kept energy markets volatile and directional. Currency markets have repriced on shifting capital flows and policy divergence. These are not peripheral markets - they sit at the centre of how geopolitical stress propagates through the real economy. Systematic trend following is well-suited to precisely this environment. Not because it predicts geopolitical outcomes (it doesn't) but because it is built to detect and follow the price trends that geopolitical stress tends to produce. When energy trends, it captures energy. When currencies move on safe-haven flows, it captures that too. The strategy doesn't need to know why a trend is happening. It needs to know that it is. The Diversification Assumption Worth Re-examining Most portfolios carry an implicit assumption: that diversification across asset classes will provide protection when conditions deteriorate. In stable regimes, this assumption generally holds. In stress regimes, it often doesn't. When a single macro force - geopolitical risk, an energy shock, a sudden policy reversal - moves through markets simultaneously, assets that appeared uncorrelated begin moving together. The diversification that looked sound on paper compresses exactly when it needs to expand. This is not a flaw to be corrected with more asset classes. It is a feature of how modern markets behave under stress, and it requires a different solution: exposure to return streams that are structurally independent of traditional beta, rather than just spread more widely across it. "True diversification isn't about just holding more assets," says Simone Haslinger, CEO of East Coast Capital Management. "It's about holding assets that behave differently when conditions become difficult. That's a higher bar -- and it's the bar that matters." A Framework Built for Uncertainty, Not Despite It At ECCM, we are often asked how trend following performs in "normal" markets. The reality is that trend following is designed for the full range of market conditions, but it tends to earn its keep most visibly in environments like the current one. Geopolitical stress produces the extended, directional moves across commodities, currencies, and rates that trend following is built to capture. Elevated volatility, far from being a headwind, is the raw material the strategy works with. And because our approach is rules-based, it doesn't require us to take a view on how a conflict resolves, which policy will be enacted, or how long uncertainty will persist. The price action tells us what we need to know. This matters in practice. When uncertainty is high, discretionary decision-making is most prone to error: anchoring to prior regimes, hesitating at inflection points, or seeking safety in familiar assets regardless of what the trends are telling them. A systematic process removes that vulnerability. Conclusion Geopolitical uncertainty is not a phase to be endured while waiting for markets to normalise. For investors with the right framework in place, it is a productive environment - one that generates the kind of clear, sustained trends that systematic strategies are built to capture. At ECCM, our ECCM Systematic Trend Fund is designed to do exactly that: to respond to what markets are doing, wherever the opportunity arises, and to deliver return streams that remain genuinely uncorrelated to traditional portfolios through periods of stress and stability alike. Wholesale clients can find more information on ECCM and the ECCM Systematic Trend Fund at Australian Fund Monitors and ECCM's website. Funds operated by this manager: |