NEWS

24 Jul 2020 - Hedge Clippings | 24 July 2020

|

|||||||||||||

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday

|

24 Jul 2020 - Manager Insights | Spatium Capital

|

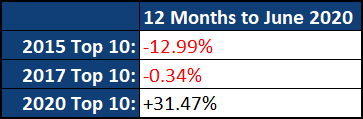

Damen Purcell, COO at Australian Fund Monitors, speaks with Jesse Moors and Nicholas Quinn from Spatium Capital. Jesse and Nicholas manage the Spatium Small Companies Fund, a long-only fund that invests in a portfolio of 25 - 40 ASX300 listed companies. Since the strategy's inception in July 2018, it has returned +15.52% p.a. against the ASX200 Accumulation Index's annualised return over the same period of +1.48%. Over FY20 the Fund rose +29.16%, outperforming the Index by +36.84%. |

24 Jul 2020 - Performance Report: Bennelong Emerging Companies Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | The Fund may invest in securities expected to be listed on the ASX within 12 months. The Fund may also invest in securities listed, or expected to be listed, on other exchanged where such securities relate to ASX-listed securities |

| Manager Comments | Over the June quarter the Fund outperformed the Index by +31.54% as the micro and small-cap stocks held by the Fund recovered even harder than the broader market. However, Bennelong reiterate that, while micro and small-cap stocks can deliver larger returns, they also come with significantly greater risk. This is highlighted by the fund's annualised volatility since inception of 36.54% against the Index's 17.40%. Top contributors included Viva Leisure, BWX, Baby Bunting, EML Payments and Mader. While each of these companies operate in very different industries, Bennelong noted they are all high quality and believe they have very promising growth prospects. As a result of the volatility seen so far in 2020, particularly in the micro and small-cap end of the market, Bennelong have made a number of changes to the portfolio. They believe the portfolio is currently well positioned for attracted returns over the long-term, regardless of the market's short-term movements. |

| More Information |

24 Jul 2020 - Performance Report: Frazis Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | The manager follows a disciplined, process-driven, and thematic strategy focused on five core investment strategies: 1) Growth stocks that are really value stocks; 2) Traditional deep value; 3) The life sciences; 4) Miners and drillers expanding production into supply deficits; 5) Global special situations; The manager uses a macro overlay to manage exposure, hedging in three ways: 1) Direct shorts 2) Upside exposure to the VIX index 3) Index optionality |

| Manager Comments | Of the top 10 ASX stocks over FY20, the Frazis Fund had 3 - Afterpay (#1), Mesoblast and Polynovo. Frazis noted companies with brilliant products and broad customer support are faring significantly better than mature incumbents. Frazis believe there is a strong chance Afterpay will enter the Chinese market with Tencent, or at the very least, Hong Kong, which they expect would add years to the company's current growth runway. Other positive contributors over the quarter included Pinduoduo, Carvana, Tesla, Twist Bioscience and Moderna. Frazis believe the multiples of many technology stocks need to compress by 25-50% to re-enter normal valuation ranges. They noted this could happen quickly tomorrow or slowly over time. With this in mind, they are selectively holding companies that they expect to have 300 - 500% larger revenues in 3 - 5 years. Looking forward, the Fund will continue to be invested across its usual themes: Software, Solar & Renewables, Online Retail, Life Sciences, Fintech, Digital Health and companies that change the way people live. |

| More Information |

24 Jul 2020 - Stimulus Fuels Breakdown Between Markets and Economic Reality

23 Jul 2020 - The Rise of Restoration: A Focus on Oil and Gas Abandonment

23 Jul 2020 - Performance Report: Bennelong Australian Equities Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | The Bennelong Australian Equities Fund seeks quality investment opportunities which are under-appreciated and have the potential to deliver positive earnings. The investment process combines bottom-up fundamental analysis with proprietary investment tools that are used to build and maintain high quality portfolios that are risk aware. The investment team manages an extensive company/industry contact program which helps identify and verify various investment opportunities. The companies within the portfolio are primarily selected from, but not limited to, the S&P/ASX 300 Index. The Fund may invest in securities listed on other exchanges where such securities relate to the ASX-listed securities. The Fund typically holds between 25-60 stocks with a maximum net targeted position of an individual stock of 6%. |

| Manager Comments | Over the June quarter the Fund returned 21.90% against the Index's +16.48%. The main positive contributors to quarterly performance were James Hardie, Breville Group and Fortescue Metals Group. Bennelong noted that, while these stocks were sold off in the market downturn in the previous quarter, their operating businesses have held reasonably well despite covid-related headwinds. The main detractors included CSL and Fisher & Paykel Healthcare, both of which are defensive stocks that significantly outperformed during the previous quarter's downturn but which subsequently underperformed during the June quarter's recovery. Bennelong maintain a reasonably balanced outlook for the market, trying not to be either too bullish or too bearish. They noted that, in this context, they continue to see good prospects for a continued recovery in the economy and market. |

| More Information |

22 Jul 2020 - Performance Report: Cyan C3G Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | Cyan C3G Fund is based on the investment philosophy which can be defined as a comprehensive, clear and considered process focused on delivering growth. These are identified through stringent filter criteria and a rigorous research process. The Manager uses a proprietary stock filter in order to eliminate a large proportion of investments due to both internal characteristics (such as gearing levels or cash flow) and external characteristics (such as exposure to commodity prices or customer concentration). Typically, the Fund looks for businesses that are one or more of: a) under researched, b) fundamentally undervalued, c) have a catalyst for re-rating. The Manager seeks to achieve this investment outcome by actively managing a portfolio of Australian listed securities. When the opportunity to invest in suitable securities cannot be found, the manager may reduce the level of equities exposure and accumulate a defensive cash position. Whilst it is the company's intention, there is no guarantee that any distributions or returns will be declared, or that if declared, the amount of any returns will remain constant or increase over time. The Fund does not invest in derivatives and does not use debt to leverage the Fund's performance. However, companies in which the Fund invests may be leveraged. |

| Manager Comments | Top positive contributors over the month were Quickfee and Kip McGrath. The largest detractor was Jumbo Interactive. Over FY20, top contributors included Quickfee, Swift Networks, Motorcycle Holdings, Afterpay, Alcidion, Atomos, Schrole and Big River. Key detractors included Victory Offices, Murray River Organics, AMA Group, Experience Co, Jaxsta, Raiz and CarbonXT. Cyan remain optimistic of ongoing positive returns, however, they noted they don't believe it's the time to be running a 'set and forget' portfolio. |

| More Information |

22 Jul 2020 - Clarity & Opportunity in a COVID-19 World

21 Jul 2020 - Performance Report: 4D Global Infrastructure Fund

| Report Date | |

| Manager | |

| Fund Name | |

| Strategy | |

| Latest Return Date | |

| Latest Return | |

| Latest 6 Months | |

| Latest 12 Months | |

| Latest 24 Months (pa) | |

| Annualised Since Inception | |

| Inception Date | |

| FUM (millions) | |

| Fund Overview | The fund will be managed as a single portfolio of listed global infrastructure securities including regulated utilities in gas, electricity and water, transport infrastructure such as airports, ports, road and rail as well as communication assets such as the towers and satellite sectors. The portfolio is intended to have exposure to both developed and emerging market opportunities, with country risk assessed internally before any investment is considered. The maximum absolute position of an individual stock is 7% of the fund. |

| Manager Comments | The strongest performer in the portfolio in June was Indonesian toll road operator, Jasa Marga, up +24.4% as it rebounded from an oversold position as traffic starts to recover and the government pledges continued support for the growth of the sector. The weakest performer in June was German airport group, Fraport, down -13.2% as flights remain grounded, COVID-19 continues to spread and expectations of a return to normal travel environments get pushed out further. 4D believe the weak environment has been completely priced into the current share price. 4D noted infrastructure investment delivers a significant economic multiplier when capital is efficiently allocated. Their view is that the prospect of increased need for investment, together with stretched government balance sheets, will inevitably lead to a longer-term trend of increased privatisations and more investment opportunities in infrastructure for the private sector. |

| More Information |