|

Powering up European network investment 4D Infrastructure April 2024 When talking about the energy transition, naturally, the focus has been on renewable energy. Many an article has been written on the exponential growth in wind, solar and batteries driven by increasing power demand, fossil fuel replacement, and societal concerns driving government and corporate targets towards net zero. The focus on renewables has thus always overshadowed the complementary need for investment in electricity transmission and distribution networks. This is despite grid operators long being vocal about the importance of accelerating investment to adapt to these essential changes in power generation and energy consumption. Networks lagging generation in the race for net zeroIt's estimated that over 80 million kms of grid infrastructure will need to be added or refurbished worldwide by 2040 if countries are to fulfil their national climate commitments on time and in full - equivalent to double the length of existing grids[1]. Currently, only 20% of the $770b USD invested into clean energy goes into network investment[2]. Investors have focused more on renewables given the outsized attention and higher perceived growth prospects. Renewable companies have marketed their sizeable growth pipelines, whilst utilities as owners of transmission and distribution grids, were more constrained by regulators and policy. They needed to be more prudent in their growth assumptions given their defensive position in the market, and with concerns around affordability. Until recently, the low-rate environment supported this thesis, with the market willing to pay more for longer duration renewable growth. However, in the past couple of years, there has been a shift in investor thinking. Improving policy has supported network investmentRegulators, governments, and policy makers have started to appreciate the importance of, and urgency with which, network investment needs to happen for the energy transition. This has translated into improved regulation, more attractive investing regimes, and overall better policy. These changes have seen a materially improved outlook for most (if not all) European utilities with electricity networks exposure. This trend has accelerated in recent months and can continue to accelerate further with ongoing electrification and generative AI-related power demand, which is only just gaining traction in Europe. Some of the recent developments include:

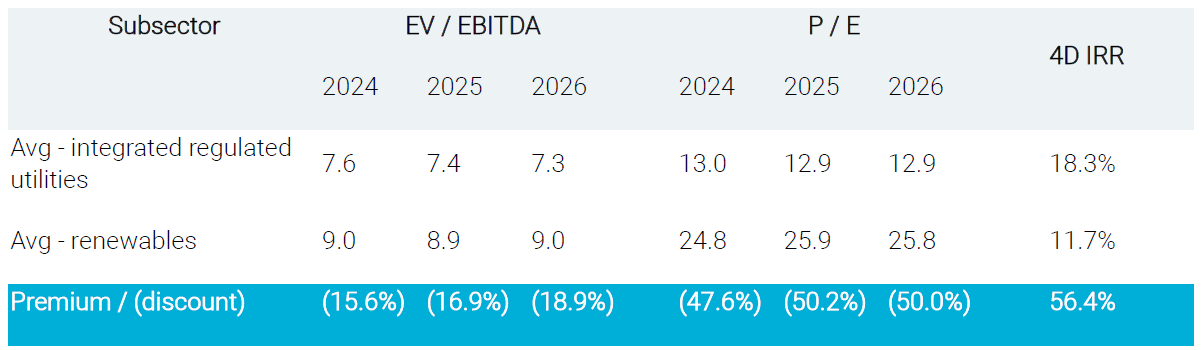

Networks have become more attractive than renewables in a higher rate environmentDespite renewable deployment continuing to accelerate, investors are starting to put more value on the visible, sustainable growth grids offer alongside the more immediate returns on capital. While we invest in both pureplay renewables and network companies, our preference in recent years has been to gain exposure to renewable developers through integrated regulated utilities. These are utilities that operate across the value chain in power generation, networks and in energy supply. We like the higher quality and often diversified (both in terms of renewable technologies and geographies) development portfolios of these companies, along with economies of scale which often provide supply chain advantages allowing for higher returns. Additionally, our research indicates that the market has undervalued and underappreciated both the scale and longevity of growth in their complementary network businesses - which, as mentioned, is only beginning to get more attention and support from governments, regulators, and operators. Capital flexibility in balance sheets, along with the ability to sell / hedge the power generated from renewables directly to retail customers, also provides us with an added level of comfort. Even with the recent outperformance of networks versus renewables, the table below highlights the ongoing disparity between valuations and market multiples across these two sectors.

[4] Integrated regulated utilities are allocating more capital into networksAs the renewables sector has suffered from inflation, cost of capital and power price challenges, we've seen integrated utilities (include some aforementioned) shifting more investment into networks. One of the clearest examples is from Iberdrola - one of our core utility holdings. Iberdrola is an integrated utility operating across power generation, networks and supply in Europe, the Americas and Asia. It's one of the largest renewable developers and network operators globally, and therefore inherently linked to the energy transition. Recognising the challenges in renewables versus the improving outlook for grids - Iberdrola in its 2022 Capital Markets Day started to pivot more towards networks. This foresight and capital allocation flexibility has proved timely. The company doubled down on its network focus in its March 24, taking advantage of policy tailwinds for networks in the UK and US, and reducing its exposure to some of the renewable energy headwinds currently at play (high rates, value creation concerns, supply chain issues, US offshore wind troubles). In doing so, the company highlighted the need to double global annual network investment by 2030 versus 2022, and triple investment by 2030 to work towards global net zero emissions targets[5]. Additionally their analysis revealed the massive long-dated needs for networks, with every 1 euro of renewables spend requiring 1 euro of network spend, and an even higher 1.25 euros in advanced economies[6]. This timely pivot is but one of the reasons we rate the quality of Iberdrola so highly. Utility underperformance provides for greater long-term opportunitiesWhile this growth outlook is unparalleled, the European utility sector has still underperformed the broader market, albeit considerably less than the pureplay renewable companies. Even with these massive growth drivers, the fact remains that utilities are considered a bond proxy and in a high-rate environment with a high opportunity cost of capital, it's difficult for these stocks to outperform. Strong economic data supporting cyclical growth and tech / AI-related trends have amplified this underperformance. While the market currently favours cyclicals over defensive growth, we have used this as an opportunity to increase our positioning in high quality network-focused utilities, such as Iberdrola, National Grid, ENEL and SSE. We believe these are all strong investment propositions given their long-dated defensive growth profiles with a secure regulated returns, which despite increased attention, still aren't being fully appreciated by the market. The content contained in this article represents the opinions of the authors. This commentary in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader. [1] https://www.iea.org/commentaries/the-clean-energy-economy-demands-massive-integration-investments-now> [2] https://www.iea.org/commentaries/the-clean-energy-economy-demands-massive-integration-investments-now>, EMDE refers to advanced, emerging, and developing economies [3] Total five-year investment plan 2024-28 compared to 2023-27 [4] 4D Infrastructure, FactSet [5] Iberdrola Capital Markets Day 2024, IEA [6] Iberdrola Capital Markets Day 2024, IEA Funds operated by this manager: 4D Emerging Markets Infrastructure Fund, 4D Global Infrastructure Fund (AUD Hedged), 4D Global Infrastructure Fund (Unhedged) |