|

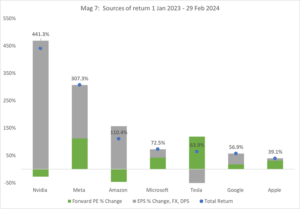

Why 2024 will be a 'show me' year Alphinity Investment Management March 2024 2023 global equity returns were dominated by an alphabet soup of megatrends. From (Chat)GPT shining the spotlight on the lifechanging potential of Generative Artificial Intelligence (GEN AI), to a broader adoption of Glucagon-Like Peptide -1 (GLP-1) diabetes drugs for weight loss and other obesity-related diseases. These megatrends resulted in extraordinary share price movements across multiple sectors as investors crowded into the themes and quickly decided who the winners and losers may be. As we head into the third month of 2024, we continue to see these megatrends dominate equity market returns. In contrast to 2023, there is a clear bifurcation between megatrend beneficiaries that can deliver revenue and earnings growth and those that can't. This is not only evident within the Magnificent 7 ("Mag 7"), but also across other so-called GEN AI and GLP-1 winners and losers. Alphinity continues to have selective exposure across both megatrends. Within GEN AI, we have exposure to early AI winners, such as Nvidia and Microsoft. In addition, we continue to invest in opportunities across the broader AI ecosystem. SK Hynix, ASML, Cadence and Accenture are examples of technology enablers and facilitators where AI is augmenting company performance. Importantly, we continue to look further afield across sectors to companies not only enabling AI but those that will also reap its benefits. We also have a nuanced exposure to the GLP-1 megatrend where the initial market clamour to define "winners" and "losers" delivered some interesting opportunities. While market leader and key GLP-1 winner, Novo Nordisk, has seen strong share price gains, assisted robotic surgery company Intuitive Surgical was initially dropped into the loser bucket on account of minor exposure to gastric banding. The market has since recalibrated ISRG expectations, and the shares have more than recovered the initial knee jerk reaction. A further broadening out of these megatrends should continue to create exciting new "show me" opportunities in 2024 and beyond. GEN AI - Show me the earningsGEN AI truly entered our lives in 2023. OpenAI's humanlike generative AI Chatbot, ChatGPT kicked off a wave of excitement across consumers and companies. What ensued was a whirlwind of AI investments and developments across multiple industries as companies explored different ways of delivering AI building blocks or integrating these technologies into their businesses. During 2023, many companies in the AI ecosystem got swept up in the euphoria. From the enablers and infrastructure providers on the front end (such as semiconductor makers and data centres) to those that design software and provide related services (including end-user applications and cloud computing), amongst others. None more so than the Mag 7. While 2023 saw the rising AI tide lift most Mag 7 boats, year-to-date there has been a large divergence in performance amongst the group, defined by those that can deliver earnings growth to justify high multiples and those who can't. AI posterchild, Nvidia, has added another c60% YTD, to be up more than 440% since the start of 2023. Importantly, during this time the Nvidia forward PE multiple has come down, from 44x to 32x. The stock has got cheaper as earnings have outstripped the remarkable share price growth. Other major enablers such as Amazon and Microsoft have continued to rally supported by strong results from increased AI demand also. Meanwhile Tesla and Apple have been dethroned by GLP-1 winner Eli Lilly and AI winner ASML, who now occupy their top 7 spots in YTD contributors. Both Tesla and Apple are facing a range of challenges, but also recently disappointed investors with the lack of progress with their AI related plans. Bifurcation within the Mag 7 driven by strong earnings power or the lack thereof: Nvidia derated despite 441% return over the 14 months

Source: Bloomberg, 29 February 2024 While industry data suggest a rapid adoption of AI across industries, the enablers continue to lead the charge year-to-date. Recent 4Q23 result releases and capex intentions underscore the longevity of investment intentions across enablers and adopters. AI mentions were at all-time highs as AI diffusion becomes more commonplace and remains a top CIO priority. While AI is emerging as one of the largest innovation cycles in decades, we are only in the early innings of its diffusion. It will take time for AI to impact revenues and margins more meaningfully and more broadly.

ConclusionIn times when the stock market is infused with captivating megatrends, such as GEN AI and GLP-1, there is a tendency for investor expectations to overshoot. Resulting in share prices of perceived beneficiaries running on speculation and the fear-of-missing-out rather than fundamentals. The intense market concentration and diverging price movements of the last 14 months is a good case in point. Looking ahead, we expect to see a continuous evolvement and adoption of both GEN AI and GLP-1. Assessing long term winners and losers along the way will be crucial and fluid. At Alphinity, we will continue to deploy our agile, tested investment process to find "show me" megatrend earnings leaders in 2024 and beyond. |

|

Funds operated by this manager: Alphinity Australian Share Fund, Alphinity Concentrated Australian Share Fund, Alphinity Global Equity Fund, Alphinity Sustainable Share Fund Disclaimer |