|

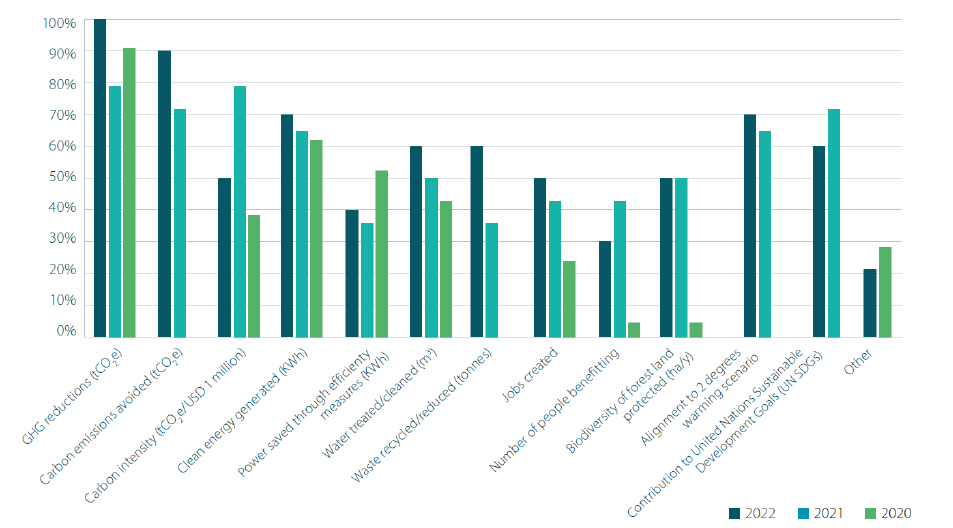

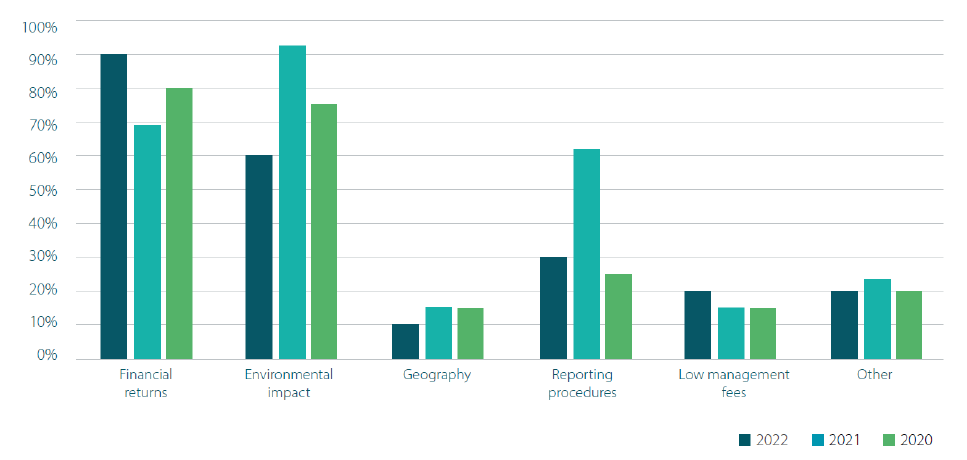

Assessing the impact of green bonds Nikko Asset Management March 2024 The green bond market has experienced tremendous growth since 2007, but despite its rapid success, there are still barriers to overcome. In particular, assessing the impact of green bonds continues to be a contentious topic. Due to a lack of standardisation among both issuers and regulators, gathering, grouping and communicating fund-level impact data is challenging, as are efforts to ensure green bonds continue to represent the interests and requirements of investors. Nonetheless, measuring the impact of green bonds is an essential component in ensuring their continued success. Which metrics matter most to green bond investors?As one would expect given the increasing appetite to understand the real impact of investments, most green bond investors track alignment with the United Nations Sustainable Development Goals (SDGs). SDGs are a great basis for mapping the use of proceeds to clear and understandable environmental and social outcomes. Indeed, many of the most common metrics required by investors - including greenhouse gas reductions, CO2 emissions avoided and carbon intensity--have become established components in impact reports from issuers. Please see an Environmental Finance survey from 2022 in Charts 1 and 2. Green, Social, Sustainability and Sustainability-Linked Bond Principles designed by the International Capital Market Association (ICMA) have been widely accepted as the common framework to provide transparency on the issuance of labelled bonds. All issuers aligned to ICMA Principles are committed to report on the allocation of proceeds, which is generally accompanied by impact metrics. While the IMCA Principles are a useful starting point to gather and compare how proceeds are being used by issuers, and the impact they have, the principles themselves are broad and not prescriptive. This means that the reporting quality and consistency between issuers can still vary widely. Some issuers will report their allocation on an aggregated portfolio basis, rather than on a bond-by-bond basis. Others may not specify what proportion of a specific project is financed by the green bond proceeds--making it almost impossible to measure bond-specific impact. In recognition of this, while adhering to IMCA Principles is a good starting point, investors seeking to meaningfully understand the impact of green bonds and want to be able to compare and contrast between different green bonds, continue to demand better quality impact reporting from bond issuers, and increasingly look to do so through issuer engagement. Chart 1: What environmental metrics are your firm most interested in?

Source: Environmental Finance survey (2022) Chart 2: What are your firm's main criteria when choosing a green bond fund to invest in?

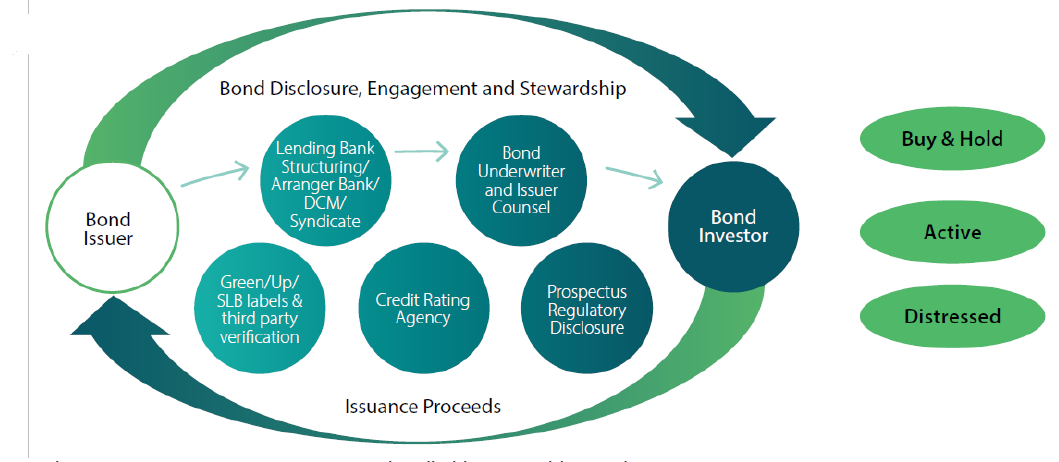

Source: Environmental Finance survey (2022) Engagement throughout the lifecycleThe IIGCC Net Zero Bondholder Stewardship Guidance advocates a long-term financing lifecycle-based approach. This presents a useful illustration on how engagement can support better impact measurement and reporting. The lifecycle includes the following steps:

Chart 3: Bond market ecosystem

Source: https://www.iigcc.org/resources/net-zero-bondholder-stewardship-guidance Regulatory challengesNew 2023 requirements surrounding the introduction of the EU Taxonomy have imposed additional regulatory responsibilities on fund managers. While initially focusing on climate environmental objectives, 2023 revisions have included a wider set of sustainably-orientated economic activities, namely:

Nikko AM's perspective is that although the EU Taxonomy is helpful for determining whether an economic activity can be considered environmentally sustainable, it is not the only approach and is less well adapted to companies beyond the EU. The EU Taxonomy could be considered as sometimes too stringent in its quantitative demands, given the availability and quality of data. Currently we do not use the EU Taxonomy to measure impact in our own funds. That said, we do recognise it has value in terms of monitoring, as well as highlighting certain key elements that any sustainable investment process should possess. What next for green bond fund impact reporting?Although impact reporting among green bond issuers is improving, the quality and consistency of impact reporting can still vary significantly. Without being properly addressed, this lack of standardisation on reporting could have deeper consequences for the industry as a whole. The lack of consistent data is not only an issue for our own analysis but also for our client's reporting expectations. The less transparent an issuer is, the less likely the bond will be included in a sustainable fund. However, progress is being made, and the global significance of green bonds means that specialist data providers are increasingly looking to provide comparable impact data for analysis and reporting, using assumptions and methodology to understand impact. Funds operated by this manager: Nikko AM ARK Global Disruptive Innovation Fund, Nikko AM Global Share Fund Important disclaimer information |