|

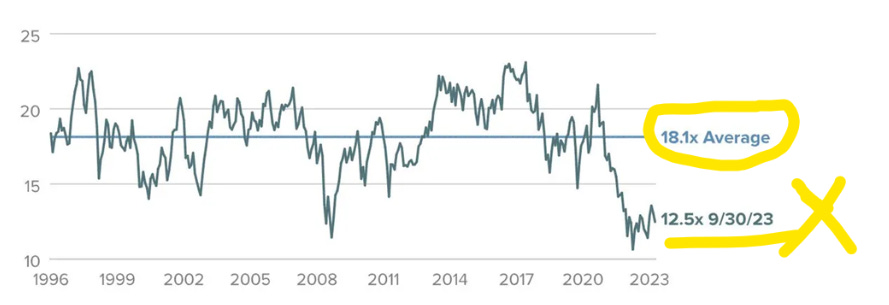

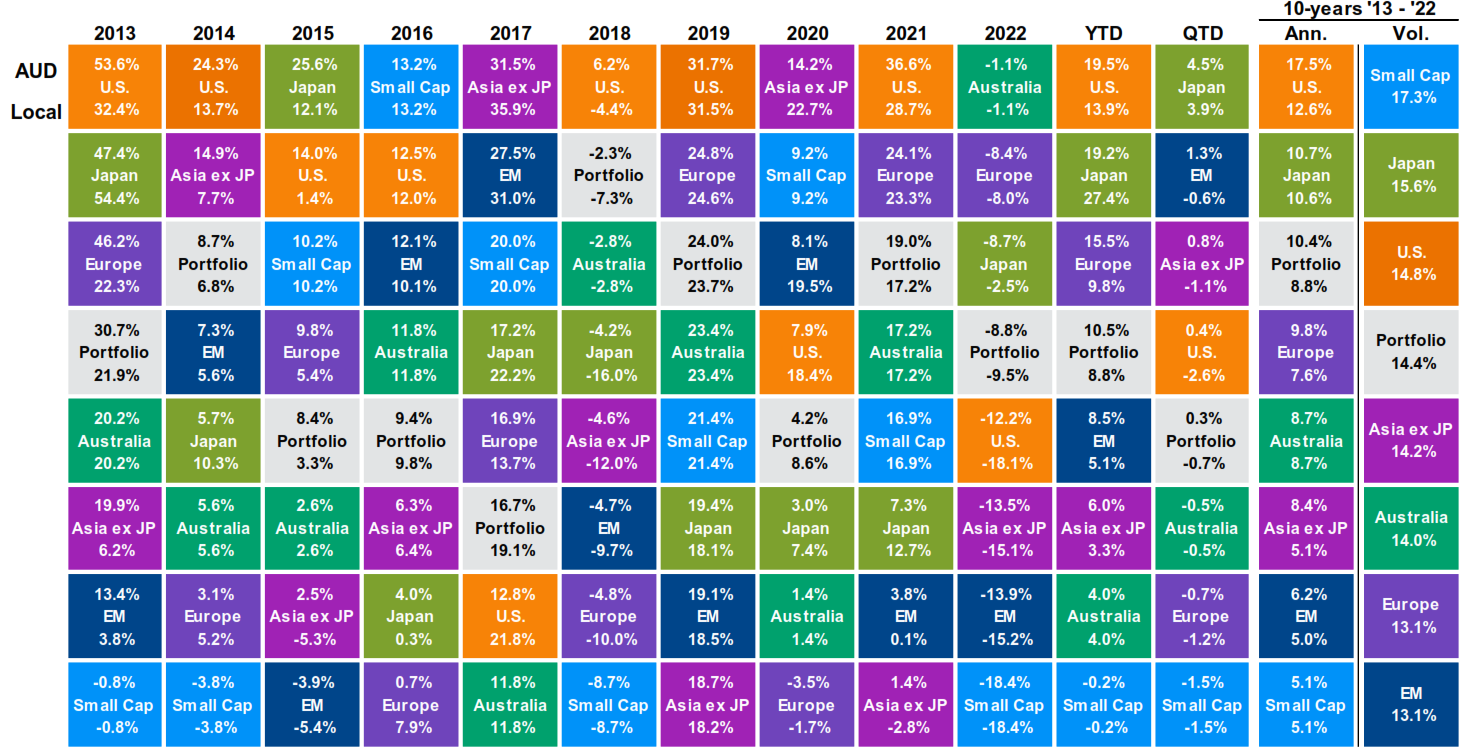

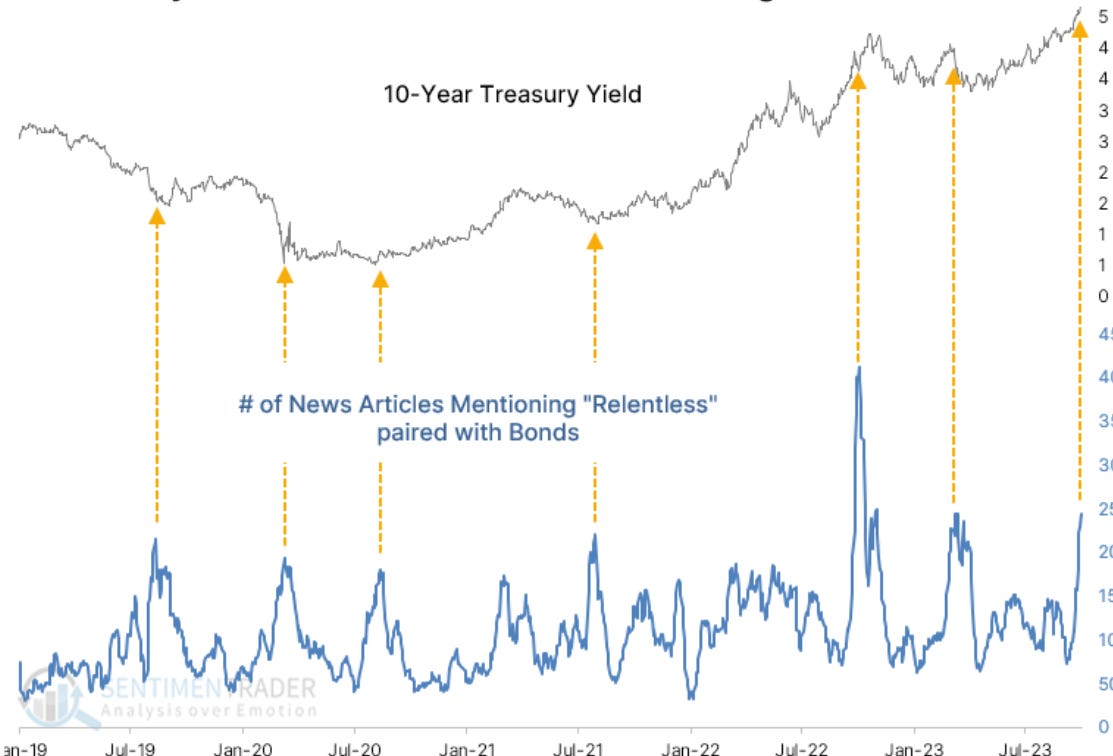

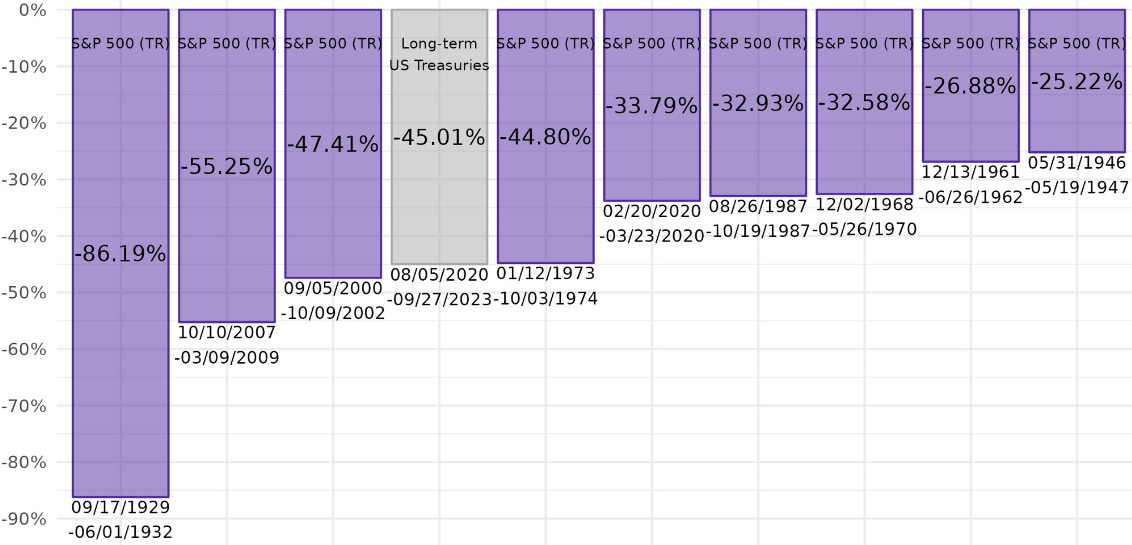

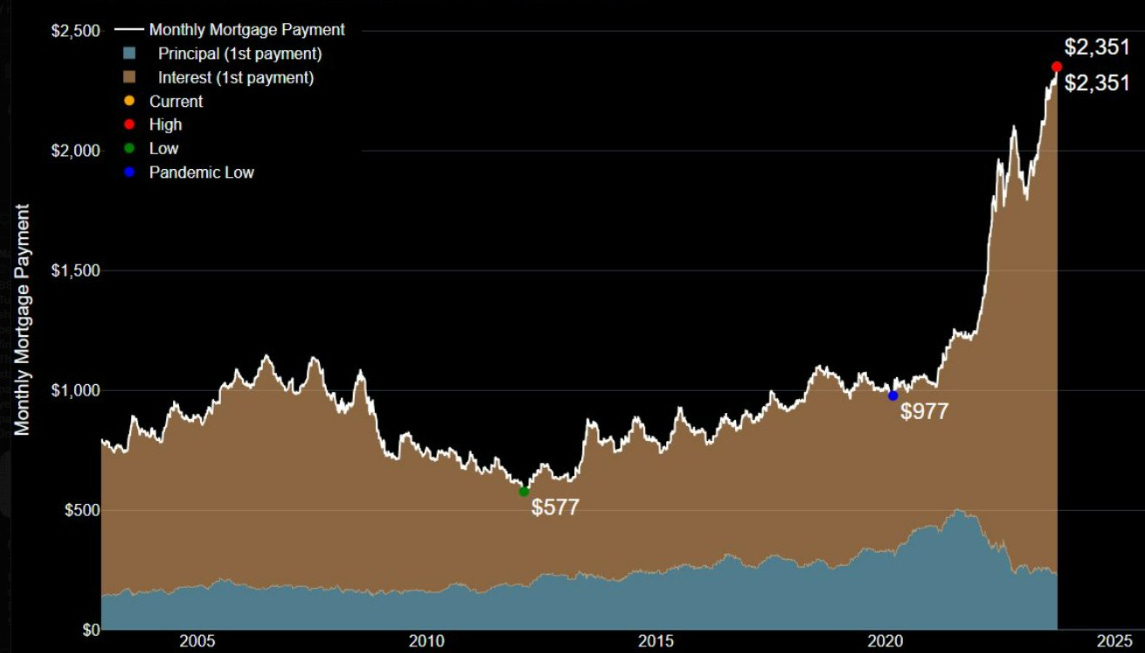

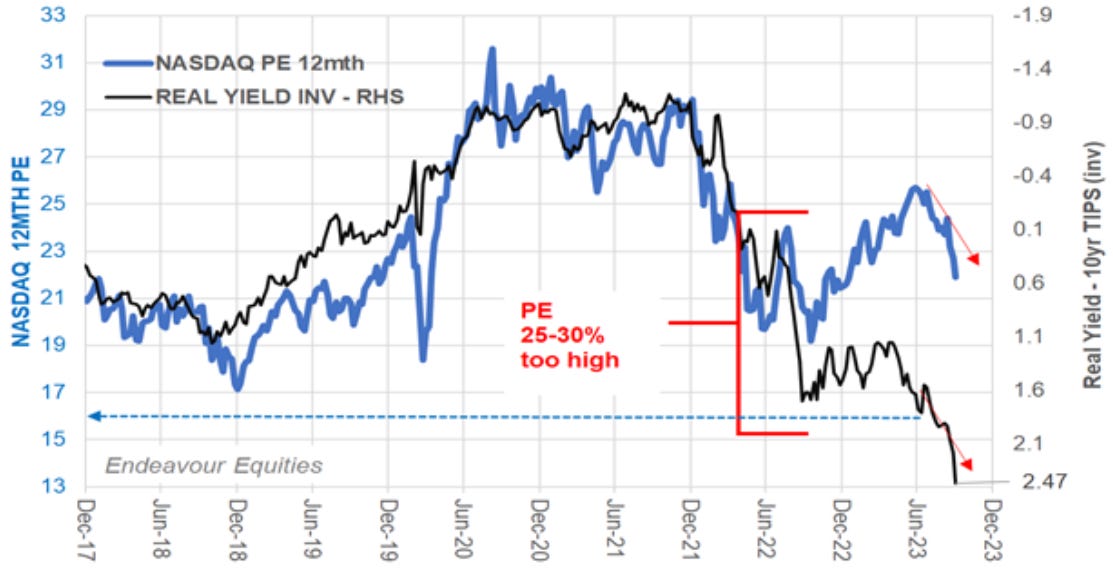

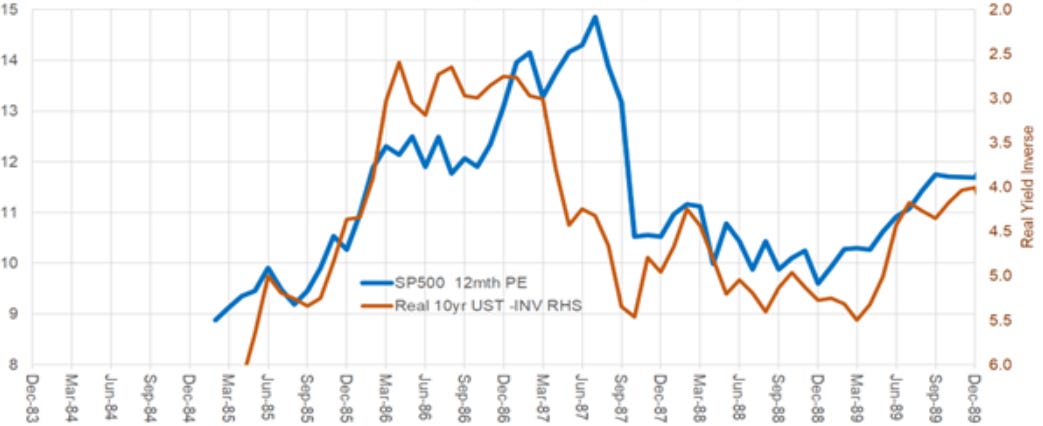

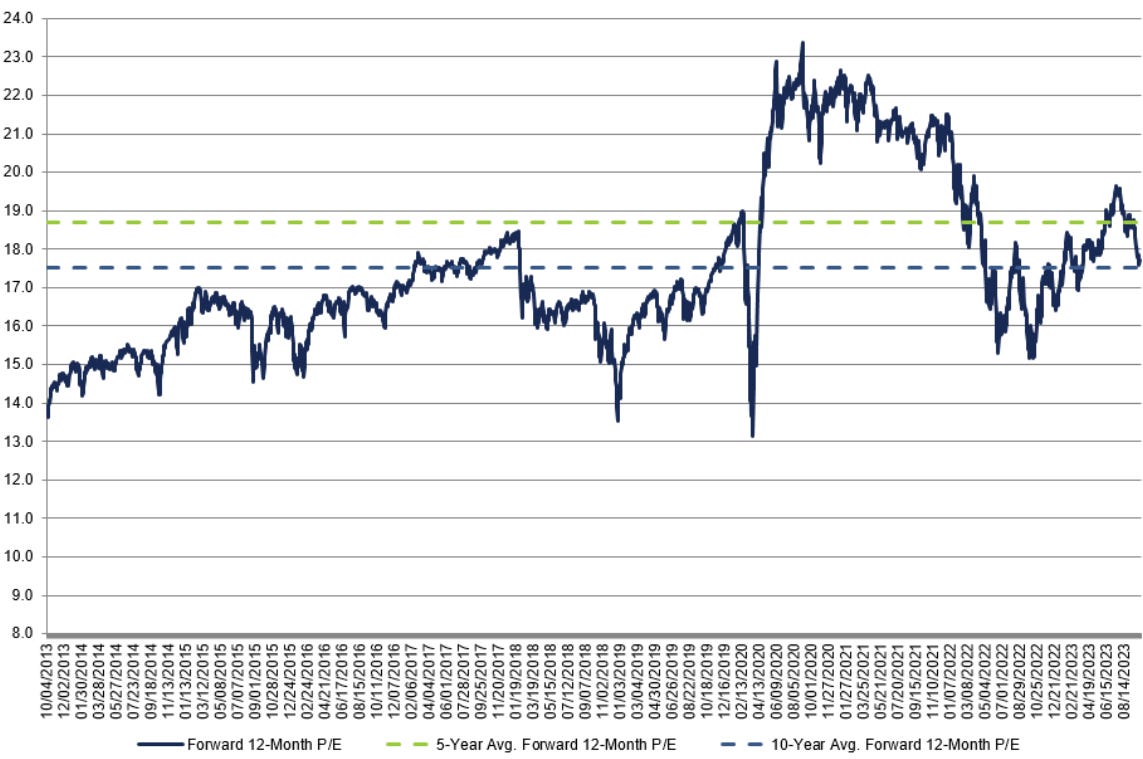

10k Words Equitable Investors October 2023 "Small caps have gone through scotched earth in the US & here," Bell Potter highlights, with JP Morgan showing small caps to be the most volatile and lowest returning asset in the past ten years. JP Morgan also shows us inflation still running above trend in developed markets, leading to a "relentless" rise in bond yields according to SentimenTrader - the flipside of which is a massive equity-like drawdown in bonds charted by @leadlagreport. Mortgage repayments, @cullenroche notes, have rocketed up. But P/E multiples haven't really responded to the shift in rates yet - Endeavour Equities charts the gap between the Nasdaq's P/E and real yields - then points out that in 1987 a P/E derating lagged higher real yields. Factset has the S&P 500's forward P/E at 17.7x, just above the 10 year average of 17.5x (calculated over a period of lower interest rates). Equitable Investors looked at Australia's 10-year government bond hitting a high not seen since 2011 as the spread between the bond yield and the ASX 200 dividend yield turned negative. We also looked at the spread between corporate "high yield" debt and the earnings yield in the US. That's as credit ratings agency Fitch sees corproate interest coverage declining "modestly" as rates stay higher for longer. Finally, Morningstar charts how Australian consumers are spending more of their income and saving less. Weighted harmonic average P/E (excluding non-earners) for the Russell 2000 Source: Bell Potter World equity market returns

Source: JP Morgan Asset Management Headline consumer prices year-over-year, quarterly data

Source: JP Morgan Asset Management US bond yields rise as news articles label the move "relentless"

Source: SentimenTrader, Bloomberg 2020-2023 - 20+ year US treasury drawdown compared to largest stock Source: @leadlagreport Monthly mortgage payment using median existing home pirce in US with a 20% down payment & average 30Y mortgage rate

Source: @cullenroche, Bloomberg Nasdaq P/E v inverse of the real yield on 10 year inflation-protected treasuries

Source: @EquitOrr / Endeavour Equities In 1987 P/Es derated as a delayed reaction to higher real yields Source: @EquitOrr / Endeavour Equities S&P 500 forward 12 month P/E ratio - 10 years

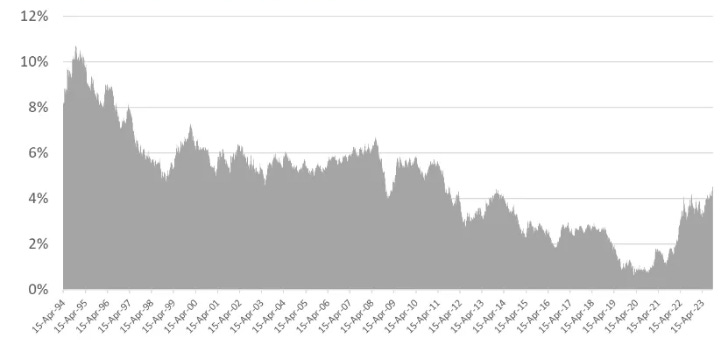

Source: FactSet Australian government 10-year bond yield

Source: Iress, Equitable Investors Spread between S&P/ASX 200 dividend yield & 10 year bond yield

Source: Iress, Equitable Investors Spread between US BBB corporate bonds and the S&P 500 earnings yield Source: GuruFocus, Equitable Investors US "high yield" corporate bond default rates rising

Source: S&P Change in Fitch's forecast for 2023 inveterst coverage (EBITDA / interest) Source: Fitch Real household incomes declining and saving rates low

Source: Morningstar, ABS October Edition Funds operated by this manager: Equitable Investors Dragonfly Fund Disclaimer Nothing in this blog constitutes investment advice - or advice in any other field. Neither the information, commentary or any opinion contained in this blog constitutes a solicitation or offer by Equitable Investors Pty Ltd (Equitable Investors) or its affiliates to buy or sell any securities or other financial instruments. Nor shall any such security be offered or sold to any person in any jurisdiction in which such offer, solicitation, purchase, or sale would be unlawful under the securities laws of such jurisdiction. The content of this blog should not be relied upon in making investment decisions. Any decisions based on information contained on this blog are the sole responsibility of the visitor. In exchange for using this blog, the visitor agree to indemnify Equitable Investors and hold Equitable Investors, its officers, directors, employees, affiliates, agents, licensors and suppliers harmless against any and all claims, losses, liability, costs and expenses (including but not limited to legal fees) arising from your use of this blog, from your violation of these Terms or from any decisions that the visitor makes based on such information. This blog is for information purposes only and is not intended to be relied upon as a forecast, research or investment advice. The information on this blog does not constitute a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. Although this material is based upon information that Equitable Investors considers reliable and endeavours to keep current, Equitable Investors does not assure that this material is accurate, current or complete, and it should not be relied upon as such. Any opinions expressed on this blog may change as subsequent conditions vary. Equitable Investors does not warrant, either expressly or implied, the accuracy or completeness of the information, text, graphics, links or other items contained on this blog and does not warrant that the functions contained in this blog will be uninterrupted or error-free, that defects will be corrected, or that the blog will be free of viruses or other harmful components. Equitable Investors expressly disclaims all liability for errors and omissions in the materials on this blog and for the use or interpretation by others of information contained on the blog |