|

China - the re-opening trade that never quite was 4D Infrastructure September 2023 In this article, we explore why China's re-opening has proven to be more fizzle than fireworks.

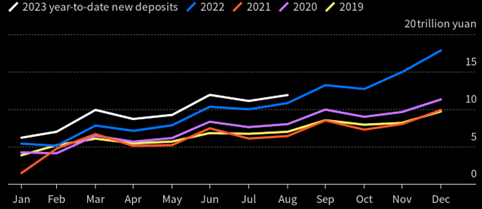

So, what went wrong? The data China's economic re-opening initially followed the expected trajectory. However, it sputtered out in the second quarter, and by July, activity numbers looked terrible. Some stabilisation has occurred in the latest August releases, but most key measures are still well below pre-COVID levels. The expectation of a pent-up consumption wave has been replaced by a more cautious household approach, marked by a higher savings rate than the four years prior. Chinese household savings

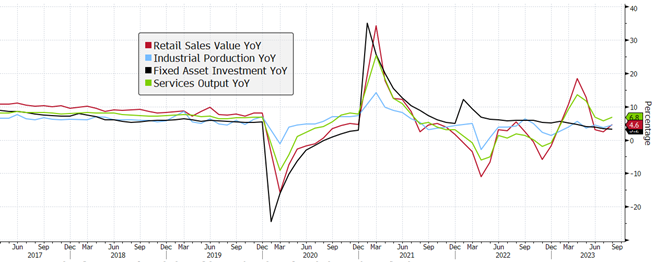

One of the main sectors that did benefit from the re-opening was restaurants (+19.4% YTD), as Chinese consumers embraced 'activities' post-extended COVID lockdowns. This was at the expense of spending on household goods (home and office appliances, and building materials). The chart below shows China's retail sales growth. Key activity data

Since re-opening, other activity, loan and survey data has also been mixed:

The slowdown in sales has put pressure on developer cashflows, with Country Garden, the largest developer outside of Tier-1 cities, under bankruptcy clouds in August. Any further signs of stress in the property market will have a detrimental effect on consumer confidence. Real estate measures (trended, mil m2, CNY bil)

Policy response and stimulus The Chinese government understands that stabilising the property market is crucial to shifting the consumer mindset towards a more spending-oriented approach, not just in the short term but as part of a long-term transition from heavy investment and export-driven growth to domestic consumption and value-added sectors. Initially, investment markets expected substantial stimulus measures when signs of weakness emerged in Q2. However, during their July politburo meeting, the People's Bank of China (PBoC) opted for more targeted fiscal stimulus across specific sectors and smaller policy measures. The government has refrained from providing cash handouts, a stance endorsed by western governments. In essence, the Chinese government is prioritising boosting consumer sentiment and spending over pursuing indiscriminate growth, especially given the significantly higher Chinese government debt compared to previous periods of stimulus, such as the Global Financial Crisis (77.7% of GDP vs. 29.3% in 2007). To date, triggers that have been pulled include:

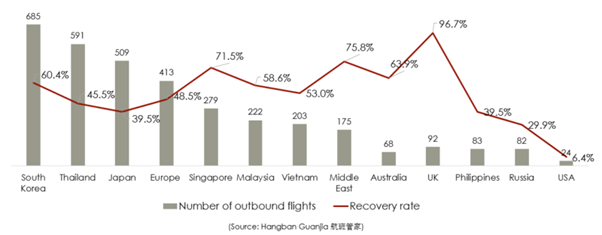

Our infrastructure exposure Within 4D's investment universe of core infrastructure, notably airports, ports, toll roads and utilities, the fundamental outlook has been mixed, with significantly overdone equity market moves. Travel demand in China has been a story of two markets. Domestically, flights are now above pre-pandemic levels, while, as at July, international travel is only at 46.9% of pre-pandemic levels. The slower-than-expected international recovery is due to the slow easing of restrictions (access to new passports and visas, group travel). Flight capacity has also been patchy regionally, and highly political, with capacity negotiated bilaterally between countries. However, we believe the demand is there. As consumer confidence increases, we expect an increase in Chinese tourists in European and Asian airports. European operator, Fraport, highlighted that there had been a steady recovery since re-opening from 18% of pre-pandemic levels in January, to 52% in June, with expectations this will continue to ramp up in the second half of the year. It has left its outlook unchanged for the financial year, anticipating Q3 will be back to 50-60% of 2019 while Q4 is expected to reach 80%, with December at 90%. Adding to the positive international momentum, in August, an additional 78 countries were added to the list where travel agents were allowed to sell group tours and package travel. Outbound flights from China (July 2023)

In the Chinese toll road sector, network traffic is now exceeding pre-COVID levels at 100- 120%. Some government policies on consumption are also benefiting the sector, such as reducing the tax on passenger vehicles and increasing subsidies for electric vehicles. Domestic car ownership maintained steady growth in the first half of 2023, reaching 328m vehicles (+5.8%). Further, the balance sheets of the listed toll road operators are in a very strong position to take in new assets should the provincial governments look to raise capital through asset sales. The port sector has seen muted volumes at both an export and import level, while yields have been solid. The volume story should not be a shock to the market - as flagged by operators - it's partly structural due to factors other than the stalled re-opening (e.g. global onshoring). The gas sector has fundamentally been slower to rebound. There has been some loss in volume growth given the slower economic activity, especially for those exposed to factories and manufacturing regions. There is also some concern over the slowing property market and a loss of new-connection revenue. However, the market has completely over discounted what we believe to be short-term shocks, and the sector is currently offering very attractive value. On our stress testing, we would have to assume zero volume growth for the next 25 years and a huge jump in the risk premia to get close to current prices. Conclusion The COVID re-opening boom and revenge-spending that was witnessed globally did not eventuate or persist as expected in China. Whilst activity data, credit growth, and consumer and business confidence has been weak, there have been signs of stabilisation in recent data points. However, one month doesn't change a picture, and market sentiment remains very poor, with foreign investor outflows still elevated. At an infrastructure sector level, domestic activity on toll roads and domestic air travel are already ahead of 2019 levels. Furthermore, the easing of travel restrictions and opening of travel capacity with key travel markets will positively impact European and Asian-based airports relying on Chinese travellers. Regardless, Chinese equities are pricing in multi-cycle low valuations, and some stocks are trading as if the re-opening never happened. We continue to be highly selective in our portfolio and continue to invest on fundamental value and assess investment opportunities that are beneficiaries to the Chinese economy, both directly and indirectly. |

|

Funds operated by this manager: 4D Global Infrastructure Fund (Unhedged), 4D Global Infrastructure Fund (AUD Hedged), 4D Emerging Markets Infrastructure Fund For more information about 4D Infrastructure, visit https://www.4dinfra.com/ The content contained in this article represents the opinions of the authors. This commentary in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader. |