|

The good news? We're avoiding recession. The bad news? Living standards are going backwards Pendal September 2023 |

|

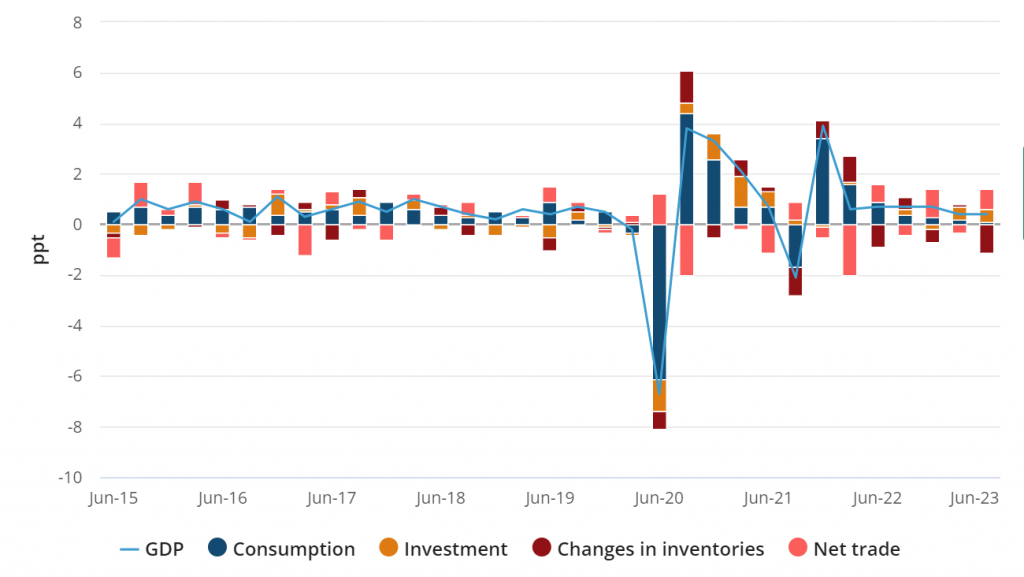

Australia is in a 'per-capita recession', which means economic growth is not keeping pace with population growth. TIM HEXT explains the problem and what's likely to happen next AUSTRALIA'S national accounts -- quarterly estimates of economic flows such as GDP, consumption, investment, income and saving -- land two months after the end of a quarter. Many therefore ignore them as old news. But they are the most comprehensive picture of the Australian economy from a macro and micro lens. So what does the latest data reveal about Australia at the end of June? In short, it is a very mixed picture. More than ever how you are feeling depends on where you sit. This ABS graph below shows the various contributions: First, the good news. We are avoiding a recession. GDP is 2.1% higher than a year ago, though slowing. It's been 0.4% for two quarters now and will likely end the year near 1.2% -- slightly higher than the RBA forecast of 0.9%. Inventories are unlikely to be a drag next quarter, but net trade should also stabilise. Now the bad news. We are clearly in a per-capita recession. In other words, this level of economic growth is not enough to keep pace with population growth. Which means the average person is going backwards in their standard of living. Our population grew by 0.7% in Q2, the economy only 0.4%. GDP per capita is now 0.3% lower than a year ago and 0.6% lower than six months ago. We are importing growth, not growing from within. Per-capita recession Why are we in a per-capita recession? We are seeing more hours worked as employment rises along with our population. But we are going backwards in GDP per hour worked -- down a staggering 2% in the quarter. This is one of the worst results since deregulation in the 1980s. Remember this is a volume measure -- not price or value. Productivity is going backwards. It has now gone nowhere since 2016. Put simply, the RBA is facing labour costs rising at 4% -- with stagnant or even negative productivity. Unless businesses wear the squeeze, inflation is not coming back too far below 4% for some time. Consumers tighten belts How is the consumer holding up in the face of rate rises? Household consumption barely grew in the June quarter at 0.1%. Services were up 0.2% but goods were flat. We are tightening our belts in discretionary spending, which fell 0.5%. This is consistent with a soft landing and is not disastrous, at least for now. Motor vehicle sales are still strong, so maybe cashed-up baby boomers are buying four-wheel drives for their lap of Australia. Pandemic stimulus savings are a thing of the past -- the savings rate has fallen to a cycle low of 3.2%. In the national accounts savings is a residual (income less consumption) and not directly measured -- so it is not always an accurate indicator. But it shows buffers are falling, albeit very differently across age groups. The growth we did have came through a rebound in export volumes and ongoing government investment. This continues a pre-pandemic theme and shows as a country our ongoing reliance on these two sectors, which is concerning. Likely we will commission another productivity report -- having ignored previous recommendations -- and kick the can down the road. The immigration lever In the near term, the RBA would be a little less comfortable about this national accounts picture. But we think labour supply via immigration will push unemployment back up to 4% and ease some wage pressures. This should buy the RBA more time while the full impact of 4% in rate rises in little over a year feeds through. (We are still only 80% of the way there). If Australia was a company these accounts would be causing analysts to downgrade their outlook. Workers are less productive and costs are rising. But some of this may still be the lingering impact of the pandemic. Cue discussions on working from home. The RBA will be hoping this can turn around in the year ahead. Immigration will slow in the next 12 months to around 1%, because the sharp increase in foreign student numbers was a one-off return from the pandemic. An outright recession (not just a per capita one) is not a base case -- but the chances of it will rise. Dr Bullock will be facing the dilemma of a slowing economy under full employment and high wages as she takes over as RBA governor in a fortnight. We wish her luck trying to work out what all this means for rates. Author: Tim Hext, Portfolio Manager and Head of Government Bond Strategies |

|

Funds operated by this manager: Pendal Focus Australian Share Fund, Pendal Global Select Fund - Class R, Pendal Horizon Sustainable Australian Share Fund, Pendal MicroCap Opportunities Fund, Pendal Sustainable Australian Fixed Interest Fund - Class R, Regnan Global Equity Impact Solutions Fund - Class R, Regnan Credit Impact Trust Fund |

|

This information has been prepared by Pendal Fund Services Limited (PFSL) ABN 13 161 249 332, AFSL No 431426 and is current as at December 8, 2021. PFSL is the responsible entity and issuer of units in the Pendal Multi-Asset Target Return Fund (Fund) ARSN: 623 987 968. A product disclosure statement (PDS) is available for the Fund and can be obtained by calling 1300 346 821 or visiting www.pendalgroup.com. The Target Market Determination (TMD) for the Fund is available at www.pendalgroup.com/ddo. You should obtain and consider the PDS and the TMD before deciding whether to acquire, continue to hold or dispose of units in the Fund. An investment in the Fund or any of the funds referred to in this web page is subject to investment risk, including possible delays in repayment of withdrawal proceeds and loss of income and principal invested. This information is for general purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. It has been prepared without taking into account any recipient's personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation. The information may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information is complete and correct, to the maximum extent permitted by law neither PFSL nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information. Performance figures are calculated in accordance with the Financial Services Council (FSC) standards. Performance data (post-fee) assumes reinvestment of distributions and is calculated using exit prices, net of management costs. Performance data (pre-fee) is calculated by adding back management costs to the post-fee performance. Past performance is not a reliable indicator of future performance. Any projections are predictive only and should not be relied upon when making an investment decision or recommendation. Whilst we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections. For more information, please call Customer Relations on 1300 346 821 8am to 6pm (Sydney time) or visit our website www.pendalgroup.com |