|

Tim Toohey: Banking crisis far from over Yarra Capital Management March 2023 Tim Toohey, Head of Macro and Strategy, looks at the the key factors behind the collapse of Silicon Valley Bank (SVB) ($209bn of assets) and Signature Bank ($110bn in assets), and notes that there is one thing we know for certain amid a banking crisis: the cost of credit will rise and the availability of credit will fall sharply. Tim details the likely implications for Australia and concludes that despite the coming headwinds, Australian banks will remain resilient. Jay Powell declared to the US House Financial Service Committee on 9 March 2023 that there was no evidence that suggests the US Fed has overtightened policy. Instead he declared that "the ultimate level of interest rates is likely to be higher than previously anticipated. Within 24 hours the 2nd largest retail bank failure had commenced. Collectively the collapse of Silicon Valley Bank (SVB) ($209bn of assets) and Signature Bank ($110bn in assets) exceeds the biggest bank collapse in 2008 (Washington Mutual, $307bn). We are rapidly closing in on the 2008 collective peak of $374bn. Should First Republic Bank, whose share price has fallen 90% from mid-February 2023, also fail then a further $213bn of assets can be added to the total. Despite the size of these collapses, it is important not to confuse the collapse of several regional US banks as a harbinger of the next Global Financial Crisis (GFC). It was the excessive leverage, excessive risk taking and poor regulation of the investment banks that led to the GFC, not a collapse of regional and retail banks. The US does have a long history of bank crises. Most of these crises were a function of excessive speculation in real estate and financial markets and occasionally the cause could be traced to a collapse in commodity markets:

It is the savings and loans (S&L) failures of the 1980s and early 1990s that have the most similarity to today's failures. Simply put, long-dated housing loans written at low interest rates rapidly become uneconomic if funding is short dated and interest rates are rising sharply. The small and fractured natured of most US retail and commercial banks means there is no ability to turn to the equity market to raise capital which makes for fertile ground for bank runs. What has marked the failure of SVB and Signature was that instead of lending recklessly for the purposes of commodity, equity market, or housing market speculation that had brought down banks in the past, it was large falls in the value of 'long duration' crypto and tech start-up assets that proved the source of the failure. The railway bonds and Florida swamp land that had brought down banks decades earlier had merely been replaced by some equally dubiously long duration tech assets. The other relatively interesting aspect about SVB was that it seemingly forgot to do what banks normally do. Instead of making loans to purchase homes and to finance business expansions, it seems to have feasted on cheap money and start-up capital for tech entrepreneurs and purchased Mortgage-Backed Securities and Treasuries at relatively low yields and financed venture capital investments at expensive multiples. As the Fed jacked up rates, tech values fell, investors became nervous and deposits declined slowly. And then they moved very quickly. Being forced to liquidate MBS and Treasury securities at a large loss merely helped expedite the decline. Social media did the rest. Indeed, SVB is likely to be the first bank run played out almost exclusively in digital space. To be clear, this is not likely to be reflective of the average bank in the US banking system. It is not evidence of a systemic threat to the system. And importantly, depositor insurance and the preparedness of the US Treasury to provide selective guarantees for bank deposits for non-systemically important banks does make these type of banking collapses less economically painful. Nevertheless, the failures are incredibly important events for financial markets. Chart 1: US Retail and Commercial Bank Leverage & 'Greed'

To gain an insight on the vulnerability of other regional US banks, the above Chart 1 provides a broad measure of bank leverage plotted against how fast banks have attempted to expand their balance sheets. The banks that have failed or are under immediate stress are highlighted in red. What should be clear is that although the commonality of lending to tech and crypto assets may have been the source of the initial phase of the crisis, it is unlikely that the names with higher leverage and just as rapid balance sheet growth will all prove to have sufficient loan quality and the asset and liability mismatches that have created bank stresses in the past. The unique feature of the current crisis is the speed at which deposits have been shifted from the smaller regional banks to the large US banks. Electronic transfers make a bank run far more immediate, and social media has been an amplifier of fear and contagion. The other unique feature of this crisis is that the proximity to the GFC has seen major banks and policy makers act far quicker and aggressively than in the GFC. For instance, short term loans made by the Fed to the major banks in exchange for cash has surged well past the peak of 2008, a time where banks were afraid of the stigma of being seen tapping the Fed's emergency liquidity facilities. No such stigma this time around! Meanwhile, commitments from policy makers that they stand ready to do whatever is necessary to support the banking system have come much faster than during 2008, which was marked with successive failures to secure the legislature authority to make emergency funding available. In short, it is unlikely that the US banking crisis is complete and a raft of consolidation of regional banks is feasible, but it is also unlikely to be marked by the same level of confusion, inaction and liquidity shortfalls that prevailed in 2008. Of course, the banking crisis becomes more global in nature if it spreads to the 'globally systemic' banks. In the Chart 2 below, the same analysis is repeated for international listed banks. The gleeful adoption of Quantitative Easing (QE) which fuelled the surge in global money supply and bank lending has helped create plenty of other potential sources of contagion. Chart 2: Global Banking System Leverage & 'Greed'

For a central bank task with controlling inflation and economic stability, these failures and the build-up of excessive leverage are embarrassing. But they are no accident: central banks are at least partly complicit. Why?

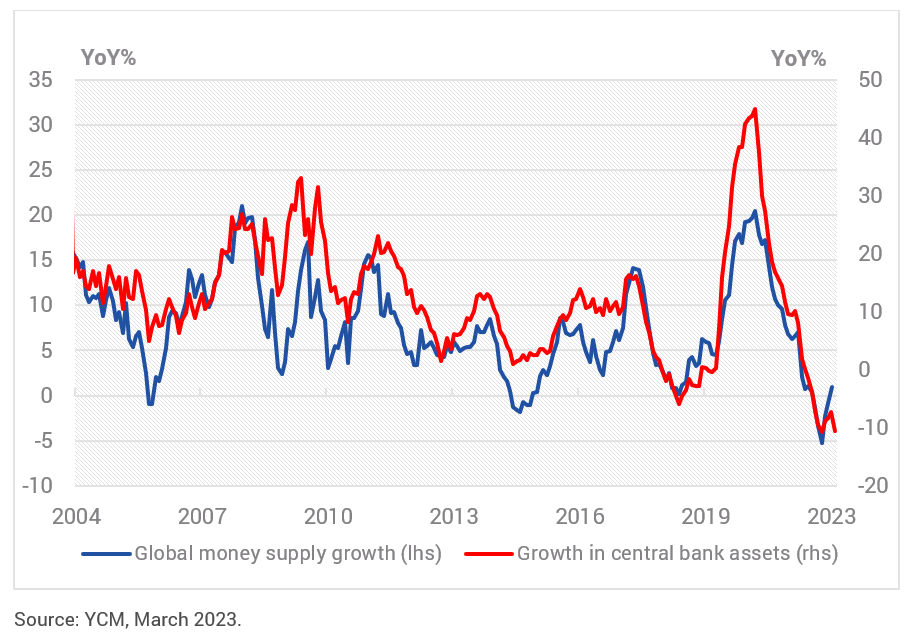

Chart 3: Central Bank Asset Growth and Global Money Supply'

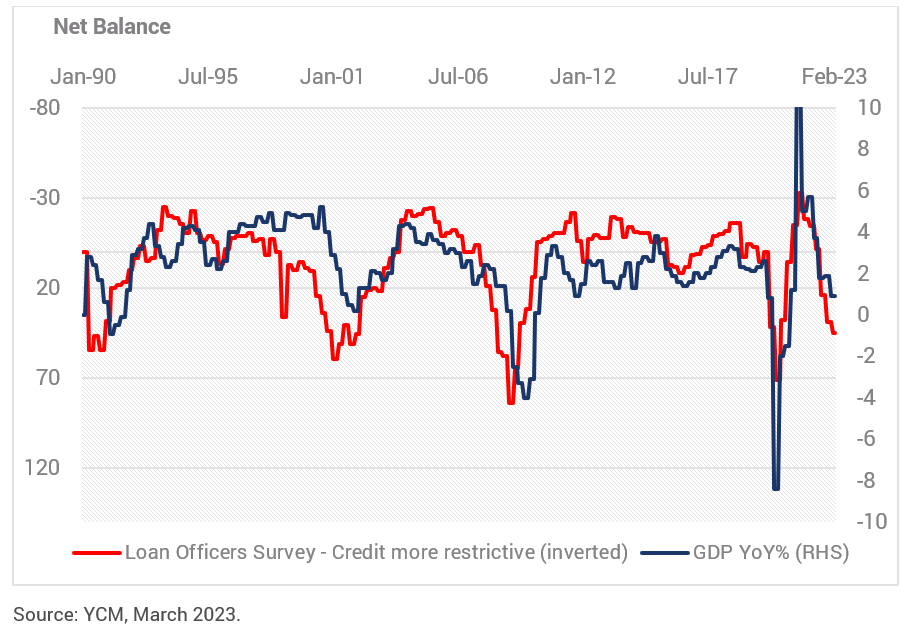

The recent rapid movement in interest rates has been sufficient to unveil some spectacular asset and liability mismatches in some US regional banks and has cast doubts on whether other banks are also sitting on large unrealised losses. Suffice to say, 'good' policy is typically marked by hiking early and in large increments at the start of the cycle and then slowing and spreading out the hikes towards the end of the cycle as incoming information is accessed for signs of a turning point. That is not what central banks have done this cycle. They did the exact opposite. Given central banks know they are already in the restrictive zone for monetary policy, given economic growth is well below trend, given inflation peaked months ago and given long dated inflation expectations are falling, then continuing to hike at this point of the economic cycle risks breaking more than just a few US retail and commercial banks. It continues to risk recession. In this respect, there is one thing we know for certain amid a banking crisis: it is that the cost of credit will rise and the availability of credit will fall sharply. The next several surveys from the US Fed's Loan Officers Survey will show a marked tightening in the availability of credit, and this has always been a rather accurate precursor to US recession (refer Chart 4). So much for the "no-landing" optimists of January and February. Chart 4: Central Bank Asset Growth and Global Money Supply'

To be clear, after its latest 25bps hike, we believe the Fed and the RBA have now completed this hiking cycle. It had been our position since mid-2022 that the economic data would not allow the Fed nor the RBA to persist with their stated interest rate intentions into mid-2023. The fractures in the banking system are by themselves sufficient to guarantee a pause in the hiking cycle, but the reality is the data is telling the central banks that the monetary tightening task is complete even if the central banks have yet to fully acknowledge it. In the case of the Australian banks, most would agree that they have some natural advantages. Capital ratios are higher - and that is a good thing - but by itself this is not a necessary or sufficient reason to avoid contagion. The real security of the big four Australian banks is fivefold: 1. The Australian banks have transformed to be primarily home loan lenders The days of the banks taking on large single loan exposures to big corporates or taking proprietary risk positions on the balance sheet are long gone. Australia's banks are boring by international banking standards, and in times of crisis that is a good thing. In the context of our chart on leverage and asset growth, the Australian banks are in the zone shown by the oval shape. The leverage is only slightly higher than it has been over the past five years and balance sheet growth has been between 11% to 29% since 2019. That's significantly below the offshore banks that experienced difficulties so far. 2. Australia's banks are homogenous To create a genuine bank run, a link with poor asset quality, poor risk controls and poor governance typically becomes the catalyst for a crisis. While Australian banks are not perfect, they do manage asset and liability risk religiously and in the post-Royal Commission period governance has been given a higher priority. But more importantly, the banks are all pretty much the same. Smaller banks were absorbed into the big banks around the GFC, and the lack of competition and underlying profitability of the back book of mortgages makes it difficult to propose a sufficient shock to the system that would see depositors flee any of the major banks. 3. The banks co invest in each other One of the underappreciated aspects of the Australian banks is that they hold large amounts of each other's paper on balance sheet. This creates an additional level of security to the oligopoly. In some ways it is a form of insurance whereby any stresses in the paper of one of the majors is diluted by the ability of the remaining banks to ensure sufficient liquidity and functioning of bank paper. 4. Government backing is clearer in Australia There is a difference between depositors having a formal government guarantee (that exists in Australia) and industry-provided depositor insurance (that exists in the US). In Australia, depositors are protected by a government guarantee up to $250,000 for each deposit holder at each bank, building society or credit union. There is very little risk to the vast majority of household deposit holders given the mean level of deposits at Australian financial institutions inclusive of offset accounts is $82,000. 5. Australian banks have stable funding sources Bank funding is overwhelming sourced from deposits. Almost two-thirds of all bank funding needs are currently met from deposits, up from 52% in 2011. Whilst it is common to think of deposits as merely household deposits, the deposits by corporate Australia, Government, Superannuation funds and other financial institutions holding deposits in banks easily exceed the level of deposits held by households. In other words, to destabilise the deposit base of Australian banks it would take more than fear amongst households. Moreover, the share of bank funding reliant on offshore issuance has declined in recent years, in part due to the cheap access to the government's term funding facility (TFF). Should stresses in international funding markets again become acute, we have the blueprint of the 2008-15 Australian Government Guarantee Scheme where the Government's AAA rating was lent to the banks to issue bonds. Australia is one of only nine countries to be rated AAA by all three major credit rating agencies, and the scheme proved highly successful in mitigating offshore funding difficulties during 2008 and 2009. In addition the Australian banks retain easy access to equity markets to maintain equity buffers. Equity remains less than 10% of bank funding requirements, however, in times of crisis the combination of offering discounted equity placements with fully franked dividends tends to find very ready recipients from both retail and institutional investors. It is worth noting that the big four banks currently offer yields of between 6.1% and 9.0% before franking benefits. Typically, US regional banks offer dividend yields of less than 2%. The combination of large, sticky deposits and ready access to capital markets with attractive yields for Australian banks provides a stark contrast to smaller US banks who are subject to deposit flight and poor access to alternative funding sources. Although Tier 1 bonds will likely remain under some pressure whilst overseas concerns are highest, we see this as more of an opportunity to selectively buy some securities at opportunistic prices. While we expect the Australian banks will underperform the broader equity market as credit growth slows, funding costs rise and P/E ratios de-rate on global concerns, we are not fearful of anything that approximates a banking run amongst the major banks. |

|

Funds operated by this manager: Yarra Australian Equities Fund, Yarra Emerging Leaders Fund, Yarra Enhanced Income Fund, Yarra Income Plus Fund |

Some familiar 2008 players are back again - i.e. Lloyds, Barclays and Credit Agricole - it is the emergence of a new batch of banks ranging from Japan, the Nordics, Canada and the Middle East that could be new sources of contagion. Nevertheless, few of these banks have attempted the same sort of balance sheet growth as the US banks that have already failed.

Some familiar 2008 players are back again - i.e. Lloyds, Barclays and Credit Agricole - it is the emergence of a new batch of banks ranging from Japan, the Nordics, Canada and the Middle East that could be new sources of contagion. Nevertheless, few of these banks have attempted the same sort of balance sheet growth as the US banks that have already failed.