|

Oil drops to lowest level of 2022 but supply-demand is likely to tighten over the medium term Ox Capital (Fidante Partners) December 2022 The low oil price today is a result of weak demand (global economic malaise) and increased supply (US strategic oil reserve release). These factors will likely normalise in coming quarters. Over the longer term, demand is set to pick up driven by China opening up and the secular economic growth of other emerging economies. Demand is likely to significantly outstrip supply given the lack of investment that has gone into the sector.

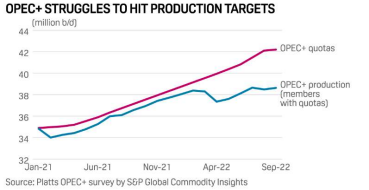

Oil price has pulled back from over US$120 per barrel in June to less than US$80 per barrel over the last week. The oil market is factoring in a short-term slowdown in demand as rising interest rates start to impact real economic activities globally. We remain optimistic about the return potential of the energy sector in the coming years. Approximately 100M barrels of oil are consumed globally each day. A surplus or deficit of 1% or ~1M barrels can lead to significant price move. At present, oil demand is artificially low and is still below pre-covid levels. In China, oil demand is ~1M barrels per day below 2021 levels because of Covid lockdown, and global jet fuel consumption is ~2M barrels per day below 2019 levels. In terms of supply, the US government has been releasing its strategic petroleum reserves, adding 0.8M barrels a day to global supply since March 2022. This will slow as we go into 2023. As a result of the short-term demand and supply distortions, OPEC+ is cutting output by 2M barrels per day by the end of 2023 to support prices, illustrating supply discipline that can be flexibly applied to uphold a quasi-price floor if required going forward. Over the longer term, it has been evident that the members of OPEC+ has been struggling to produce to their quotas over 2021 and 2022. This is likely a result of a lack of investment in oil projects over the last decade. The upside for oil price can be significant as China opens up and other emerging economies continue to grow. Supply will struggle to keep up. Major oil companies in Europe are attractively valued and are trading at a significant discount to many of the oil majors in the US. Even at an oil price of US$70, European energy companies are typically trading on 5xPE, 15% free cash flow yield, compared to 14xpe and 7.5% free cash flow yield for the Americans. Ox has selective investments in some of the leading players in this space. The current pullback in oil can create additional investment opportunities for 2023, of which we are on the lookout. Funds operated by this manager: |