|

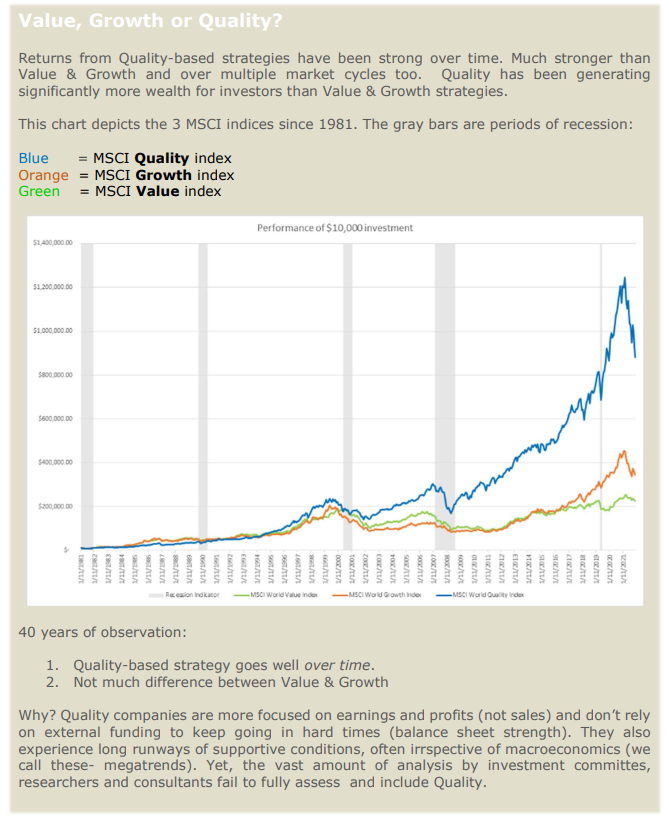

What drives poor returns? Insync Fund Managers October 2022 Most investors do not reap the benefits of compounding wealth that come from equities. Equities grow wealth very well. $100 in the S&P 500 at the start of 1926, three years prior to the great crash, would have boosted your wealth to over $1 Million today. That's 10.05% p.a. Tumultuous macro world events have rained down upon us since then, and so it's not adverse macro events that derail wealth accumulation; it is investors' reactions to them. In short, investor behaviour derails compounding wealth. We've experienced difficult months recently for our quality-based strategy including recessionary concerns. We've also delivered positive annual above market returns recently as well - 2017, 2018, 2019, 2020, & 2021 (December Ending). First to fall: When a recession looms, a Quality company's stock price often falls more than the market initially. Quickest to rise: They are also the first to recover and outperform the other major investment styles during a market recovery.

All roads lead to technology - Accenture Some of our 16 global megatrends are technology based. Despite all the negative noise shouting for our attention today, the reality is that we are in the middle of an unstoppable wave of technological advances impacting every business. From old style utilities and industrials to online payments, construction and retail. Companies must digitise their business to remain competitive, grow their customer base, revenues and earnings. Accenture is a key player assisting in this digital transformation. Accenture posted revenues of $62 billion, a record 22% growth adding $11 billion for the year, and importantly EPS growth of 18%. New bookings were $18.4 billion for the quarter, their second highest ever. A case study on how they do it- EDF French multinational utility company EDF digitizes the construction of nuclear power stations that provide low-carbon energy for more than 6 million UK homes alone. Accenture transformed EDF's digital construction processes by creating a digital factory model on a secure cloud infrastructure. This drives cost efficiencies. Construction methods that relied on thousands of uncoordinated, disjointed paper plans and text are now digitized with contractors accessing and sharing the same view and information. AI then scans and assesses this for problems and opportunities.

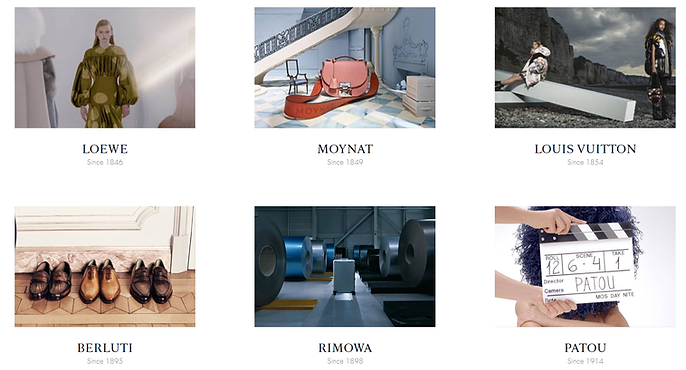

Digital dashboards provide real-time data visibility across a myriad of systems. 'Digital twins' identify areas for automation across power plants, all of which drive safety, efficiency and quality. A 'digital twin' virtually duplicates physical objects, processes & systems, and are used to predict how those elements will respond to different variables. Premiumisation powerhouse - LVMH LVMH is the world's largest luxury conglomerate. Brands include Christian Dior, Givenchy, Louis Vuitton, Tag Heuer, Bulgari, Fendi, and Moët & Chandon - even Cape Mentell wines in WA and Cloudy Bay in NZ. LVMH's products are an expression of creativity and timelessness.

The previous LVMH picture highlights an important facet of their brand strength. They are 6 of LVMH's oldest brands (houses) in the leather goods division with the Loewe brand first established in 1846. History shows heritage brands with a strong leather goods offer, fare best during economic downturns. In today's difficult macroeconomic climate LVMH delivered standout growth. LVMH recorded revenue around €56.5 billion in the first nine months alone. Up 28% compared to the same period last year. Luxury shoppers have not lost their appetite for high-end designer goods, even in tumultuous times. We have often cited the benefits of companies with pricing power and high gross margins in a rising inflationary environment. LVMH is a stand out example.

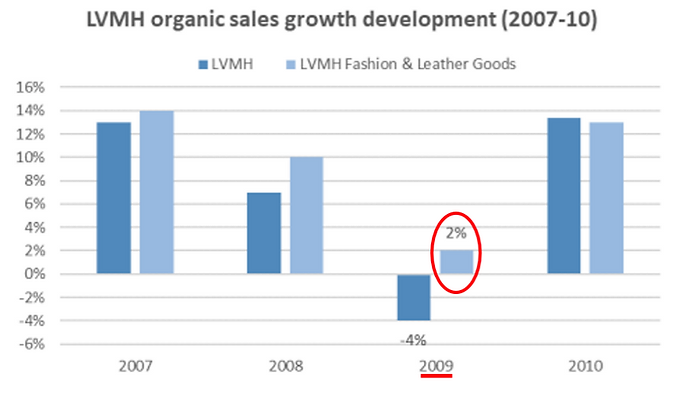

Whilst the luxury sector is not immune to recessionary shocks, the negative impacts do not last very long. The strongest brands tend come out bigger and better on the other side. LVMH offers a proven defensive track record. The GFC period highlights this. Overall sales at LVMH declined by 4% yet Fashion & Leather Goods (F&LG) posted sales growth of +2% in the worst recessionary period we have had in decades. Back then F&LG made up 55% of their total. Today it represents 75% of group profits.

Conventional wisdom pointed to people trying to hide their wealth during an economic downturn. During the GFC, anecdotes spread of shoppers coming out of Bergdorf Goodman in NY with their purchases wrapped in brown paper bags. But a 2010 joint study by the Marshall School of Business and UCLA put paid to this. The study focused on luxury leather goods and how they changed during the GFC. Leading brands substantially trimmed their offering, whilst simultaneously increasing price points. They also featured a higher proportion of items with logos or other brand identifiers. Louis Vuitton and Gucci were charging consumers more to flaunt their brands during a recession. The study explained this by segmenting luxury consumers into "Patricians" and "Parvenus", or "insiders" and "outsiders" to the world of luxury. Parvenus needed to confirm they were still wealthy during a recession by buying more items from the latest collections of lux brands. This created an opportunity for ostentatious luxury designs. The GFC sent the world into a tailspin, mainly because it was the most significant contraction in the global economy since WWII and the last global recession was 18 long years ago. Luxury stocks saw a mass sell-off. From the peak of their performance in May 2007 to trough in March 2009, an index of the top 13 luxury goods companies lost 62 percent of its value. Over the same period, the financial performance of the 13 companies making up the index was the reverse! Sales continued growing; +5.7% in 07', +6.5% in 08' and +2.2% in 2009. Their share prices recovered sharply immediately after the bad news ebbed. Investors rightly appreciated the resilience and strength of their business models. LVMH have delivered a compound annual earnings per stock growth rate of 14% p.a. since the start of the GFC. A compound annual rate of return of 17% p.a. over the same period. Summing things up The global economy is impossibly complex, with billions of moving parts driving demand, consumption and activity. Commentators, most fund managers, consultants and the media earn money trying to predict what all of these billions of consumers and companies are doing, or are planning to do over the next few weeks, months or even years. It's not only foolish but impossible. Funds operated by this manager: Insync Global Capital Aware Fund, Insync Global Quality Equity Fund Disclaimer |