|

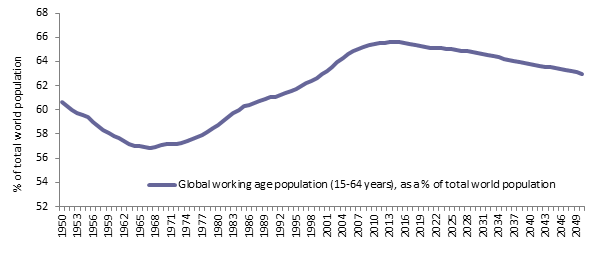

Inflation - higher for longer? abrdn October 2022 Inflation continues to be the dominant economic theme across the globe for governments, central banks and societies at large. The notion of this being a "transitory" phenomenon has been replaced by a realisation that it is much more persistent and far reaching than previously acknowledged. In turn, this has elicited aggressive tightening of monetary policy by central banks in an attempt to tame price pressures. Markets expect policymakers will be broadly successful in achieving this objective. Helpful in this respect are signs that a number of pandemic-related issues, such as supply-chain blockages and labour shortages, are beginning to ease. However, there are a variety of longer term, structural issues at play that should not be ignored as they have the potential to keep inflation elevated for a protracted period. This could further complicate the policy outlook, especially as the economic cycle looks increasingly mature. It's important to remember that the majority of these drivers were evident before policymakers rolled out Covid-induced stimulus packages. They may not be quashed by simply tightening financial conditions alone. It's therefore possible that inflation could become more ingrained globally, and while headline inflation rates may decline from their near-term highs, levels may stay elevated for longer. DeglobalisationA key facet of the mid-1980's 'Great Moderation' in inflation was increasing trade connectivity between countries and growing global interdependence. Ostensibly, developed economies benefited enormously from a liberation of the supply side. Technological advances, political reforms and economic stability allowed companies and governments to more cheaply access key inputs such as labour, raw materials and manufactured goods. In recent years, however, there's been a growing movement away from globalisation. Alarmed by China's increasing global clout, and spurred further by protectionist sentiments, the Trump administration began placing punitive tariffs on Chinese imports in 2018. President Biden has kept many of these tariffs in place. Similarly, political events such as the UK's decision to leave the EU and the embargos on Russian trade and investment are further evidence of the reversal of globalisation. At a corporate level, many firms have been moving towards shorter, more secure supply lines rather than simply the cheapest option. The pandemic exacerbated this trend. We're therefore seeing a reversal of the globalisation trend of recent decades that helped to keep input prices in check. Demographic driversInterlinked with the deglobalisation theme is the evolution of demographic factors, particularly when viewed through the prism of global supply of labour. In the late 1970s, we witnessed the beginning of an upward trend in the global working age population (those aged 15-64). This was led by the baby-boomers and medical advances. It also reflected the liberalisation of global labour markets and access to previously untapped sources of workers. The expanding supply of global labour contributed meaningfully to downward pressure on wages. However, as the chart below shows, this trend has started, and should continue to, reverse. This will potentially lead to a larger proportion of individuals who have little or no productive output but who still consume. In short, we have a situation of reduced labour supply that isn't matched by a material let up in demand. Global working age population (15-64 years), as a % of total world populationSource: UNCTAD e-handbook of Statistics 2021 Exacerbating this demographic trend has been a fall in labour participation rates in a number of developed market economies. There are various theories to explain this phenomenon. For example, large numbers of people unable to work due to 'long Covid,' early retirements and life preference changes. What matters from an inflation perspective is that reduced working age numbers, coupled with reduced participation rates, mean tighter labour markets and increased upward pressure on wages. Greenflation?An increasingly debated potential driver of structurally higher inflation is 'greenflation'. The movement towards a less carbon-intensive economy has been supported by tighter environmental regulations, as well as changing investor and corporate preferences. The result has been much reduced investment in traditional energy infrastructure in areas such as oil and gas. This is felt most acutely when exogenous strains are placed on fragile supply structures, as evidenced by the recent Ukraine conflict. More broadly, it seems unlikely that the transition towards a greener economy will be smooth. Many projects, by their very nature and scale, could take decades if not generations to execute. The implication for energy markets is that they are likely to remain volatile, with potentially increased upside risks to the inflation outlook. Putting everything togetherAlthough there will be regional and country variations, headline inflation in most developed markets appears likely to peak in late 2022 or early 2023. This will give some comfort to central bankers and government officials as it reduces the likelihood of a repeat of the early 1980s where more extreme policy measures were required to tackle excessive inflation. Still, we think inflation will remain a recurring and persistent theme, which will be a significant departure from the trend of the past four decades. With structural patterns apparently shifting, it is crucial that investors consider this evolution when constructing portfolios and recognise the value of real returns alongside nominal equivalents. Author: Adam Skerry, Head of Inflation Rate Management |

|

Funds operated by this manager: Aberdeen Standard Actively Hedged International Equities Fund, Aberdeen Standard Asian Opportunities Fund, Aberdeen Standard Australian Small Companies Fund, Aberdeen Standard Emerging Opportunities Fund, Aberdeen Standard Ex-20 Australian Equities Fund (Class A), Aberdeen Standard Focused Sustainable Australian Equity Fund, Aberdeen Standard Fully Hedged International Equities Fund, Aberdeen Standard Global Absolute Return Strategies Fund, Aberdeen Standard Global Corporate Bond Fund, Aberdeen Standard International Equity Fund , Aberdeen Standard Life Absolute Return Global Bond Strategies Fund, Aberdeen Standard Multi Asset Real Return Fund, Aberdeen Standard Multi-Asset Income Fund

|