|

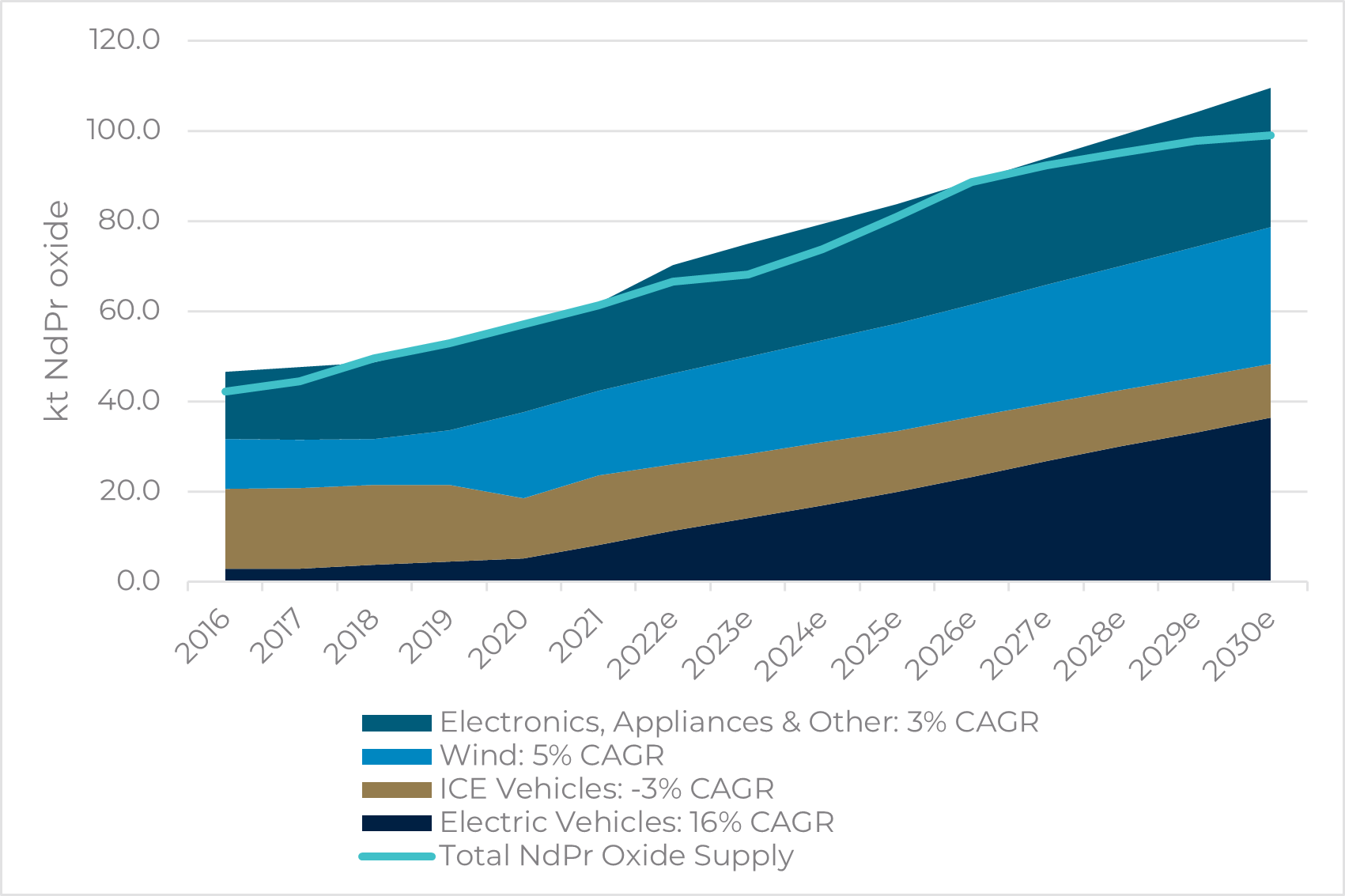

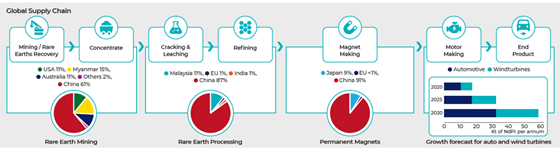

The Value in Securing Critical Mineral Supplies Tyndall Asset Management October 2022 Supply chain risk creates investment opportunities The concentration of supply of critical minerals related to decarbonisation is an issue that has been highlighted by major Western economies as a risk to securing the materials needed to meet climate goals. The US Government acknowledged its concerns around this supply chain risk within the recently passed Inflation Reduction Act. Amongst other issues, this Act outlines potential tax credits for Electric Vehicle purchases if certain conditions have been met, including that no critical mineral used in the vehicle is sourced from a "foreign entity of concern". Figure 1: Rare earths - as Neodymium-Praseodymium Oxide (NdPr) demand - EV's and wind to drive total demand growth of 6% CAGR to 2030 Source: Barrenjoey, Tyndall AM The supply dynamics of key materials needed for decarbonisation are already well understood given they are part of our most consumed metals, including copper and nickel. Others, which form an integral part of the road to electrification, are coming from an almost insignificant demand base relative to their outlook. This includes materials such as lithium, cobalt and rare earths. China's control of these materials needed to transition away from fossil fuels is extraordinary, dwarfing even that of OPEC's control of global oil markets. China controls 80% of battery raw material refining, 80% of solar panel manufacturing and 60% of wind turbine installations. Notably, while the level of market share is high for these manufactured products necessary in the energy transition, China does not dominate the supply of the raw materials needed to produce them. This provides global consumers with the opportunity to support new entrants to these markets to mitigate the risk around supply chains. However, rare earths are an exception. Figure 2: Rare Earths global supply chain

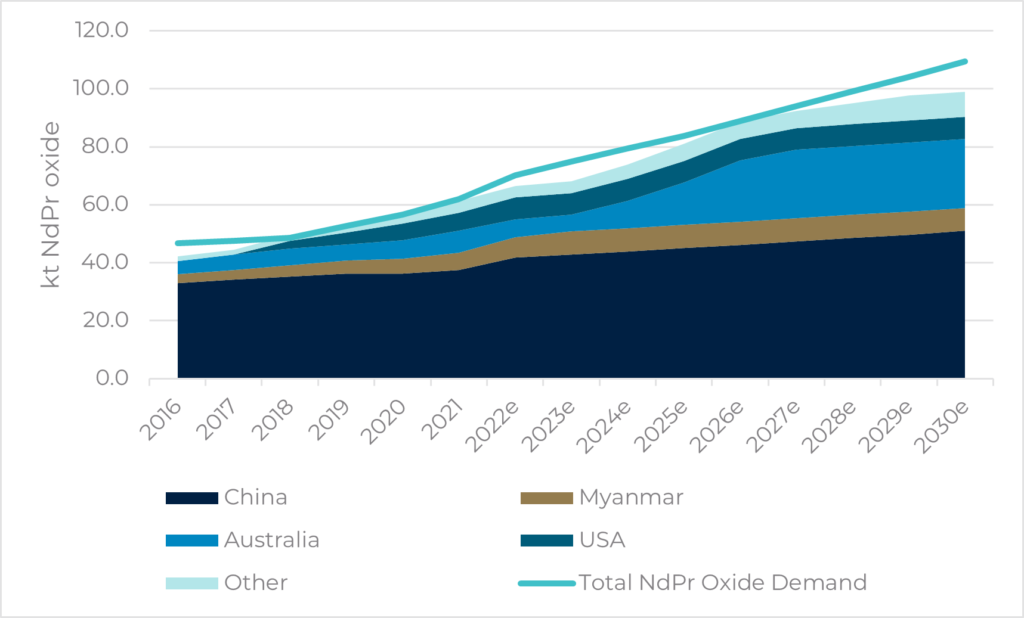

Source: Lynas Rare Earths China controls almost 90% of rare earth processing and over 60% of rare earth mining. This number could be considered closer to 75% when including Myanmar volumes which are generally trucked across the border, implying an element of control over these mines by the Chinese. The high level of market control exerted by China historically has allowed its government to manage rare earth prices to levels that have generally deterred international competition. Figure 3: Rare Earths (as NdPr) supply by region - China expected to remain dominant, but significant growth forecast out of Australia

Source: Barrenjoey, Tyndall AM Environmental risks to supply chains China's growth and dominance in rare earth mining and processing were driven by lax environmental standards which resulted in some exploitation of the country's abundant resources. The Chinese Government's credible environmental efforts saw the introduction of regulations to reduce environmental harm, including through forced industry consolidation to improve monitoring and the introduction of an export quota system to limit over-production. While environmental standards have increased, China's largest producers of rare earths still have low ESG scores. For example, China Northern rare earths is rated by Sustainalytics as "Severe Risk" and ranks the company second last out of the 14,647 stocks covered. Myanmar's nascent rare earth industry is facing substantial claims of environmental and social damage, with an Associated Press exposé highlighting substantial ecological harm and major negative impacts to Myanmar from mining practices. Land of plenty Australia can capitalise on this dynamic. It is already a key supplier of many critical minerals vital for decarbonisation, although current production is only a small fraction of the country's demonstrated resource. This provides significant scope for growth. Figure 4: Key critical minerals on major economy lists and their Australian resource endowment

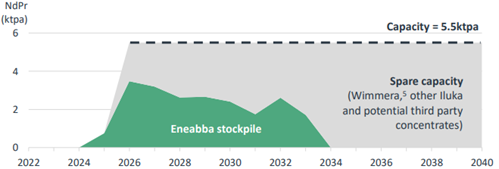

Source: Tyndall AM, Geoscience Australia Iluka's Eneabba project, located some 300km north of Perth in Western Australia, will be Iluka's relatively low-risk entry into rare earth production. It is slated to produce 2.7mtpa NdPr initially, scaling up to 5.5mtpa in later stages which equates to 7% of forecast demand (for reference, Lynas rare earths currently produces 6ktpa NdPr). Figure 5: Iluka's illustrative rare earth (as NdPr) production profile from Eneabba and the expected total capacity of the operation

Source: Iluka Resources While we usually have a healthy amount of scepticism when miners attempt to move beyond core competencies, the Eneabba project has several attributes that make it relatively low risk. These include:

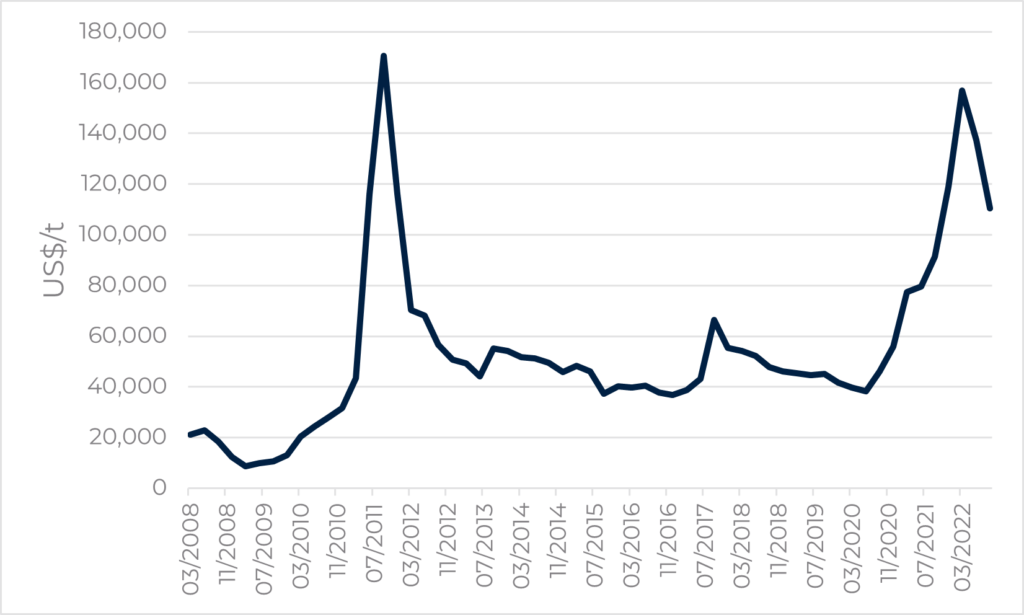

While no new development is ever a lay-down misère, it is rare to find a development in the resources space with relatively low technical and financial risk to the operator. We believe the project could ultimately be worth in excess of A$2bn and account for almost half of Iluka's value, when factoring in contributions from other resources. It is also rare to find a business fully exposed to key critical minerals at material levels of market share including elements so strategically important for decarbonisation. Conclusion As Western economies pivot to ensure supply security along entire decarbonisation supply chains, we expect the market's appreciation of Iluka's rare earth exposure will grow and add significant value to our investment. The US Inflation Reduction Act's rules around critical mineral sourcing away from "foreign entities of concern" creates a strong rationale for Australian rare earths to attract a valuation premium. We expect this will be priced into Iluka over time. Figure 6: NdPr price history (the key rare earth elements used in battery manufacture)

Source: Steelhome Author: Stefan Hansen, Senior Research Analyst Funds operated by this manager: Tyndall Australian Share Concentrated Fund, Tyndall Australian Share Income Fund, Tyndall Australian Share Wholesale Fund Important information: This material was prepared and is issued by Yarra Capital Management Limited (formerly Nikko AM Limited) ABN 99 003 376 252 AFSL No: 237563 (YCML). The information contained in this material is of a general nature only and does not constitute personal advice, nor does it constitute an offer of any financial product. It does not take into account the objectives, financial situation or needs of any individual. For this reason, you should, before acting on this material, consider the appropriateness of the material, having regard to your objectives, financial situation, and needs. The information in this material has been prepared from what is considered to be reliable information, but the accuracy and integrity of the information is not guaranteed. Figures, charts, opinions and other data, including statistics, in this material are current as at the date of publication, unless stated otherwise. The graphs and figures contained in this material include either past or backdated data, and make no promise of future investment returns. Past performance is not an indicator of future performance. Any economic or market forecasts are not guaranteed. Any references to particular securities or sectors are for illustrative purposes only and are as at the date of publication of this material. This is not a recommendation in relation to any named securities or sectors and no warranty or guarantee is provided. |