|

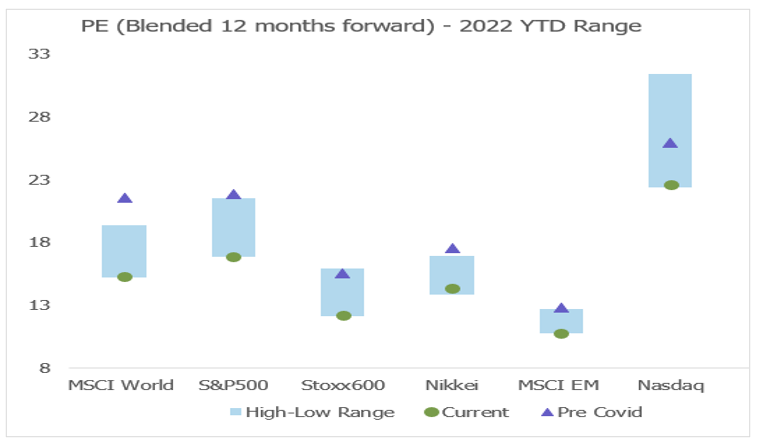

Winning by not losing Alphinity Investment Management May 2022 Investing in global equity markets has felt like playing a game of dodgeball over the last two years. Around every corner investors have been faced with a new surprise to navigate. Just as in dodgeball, where players run for cover to avoid the sting of those dreaded balls, equity investors have flocked to the safety of defensive stocks in 2022. Year to date defensives have outperformed value, growth and cyclical stocks, doing what they are supposed to do in uncertain times: offer equity investors a shield against the onslaught of valuation pressures, slowing earnings growth and increased uncertainty. As we continue to brace ourselves for ongoing volatility in equity markets, we prefer to maintain exposure to selective stocks with defensive characteristics - those that are winning by not losing. Deutsche Boerse and Merck & Co are two such examples. The big de-rating might not be overGlobal equity markets have de-rated since the recent peak in September 2020, with a sharper deceleration in 2022 driven by rising inflation fears as reflected in higher 10-year bond yields. In fact, most major market indices are now trading below their pre-Covid valuation levels. The derating has been particularly evident in the more expensive parts of the market, such as Technology stocks. For example, the Nasdaq Composite Index has fallen by -25% so far this year, with most of this occurring through forward PE multiples contracting from ~32 to ~23x currently. In comparison, the S&P 500 has fallen 16% and contracted from ~22x to ~17x over the same time frame. All major equity markets have derated sharply YTD to below pre-Covid levels

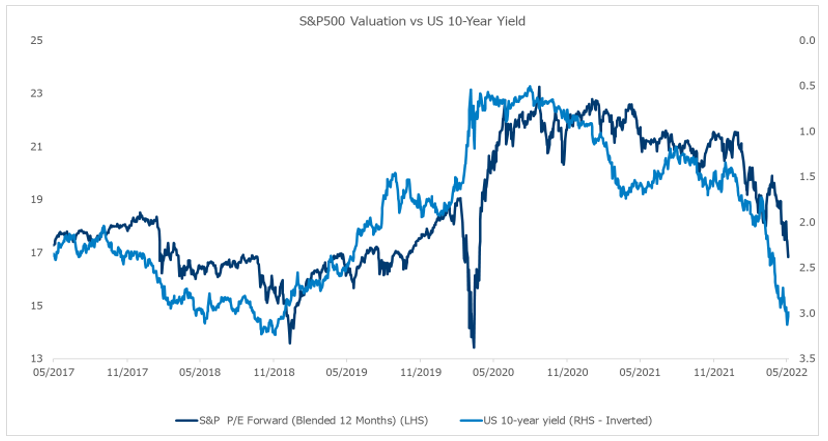

Source: Bloomberg, 10 May 2022 Despite this overall market de-rating, most major indices are still trading in line or above their 20-year averages and remain relatively high when considering the sharp rise in 10-year yields (see chart below). The Russia Ukraine War has also recently pushed commodity prices to new highs, raising inflation risks and potentially placing further pressure on market valuations. Valuations may be at more risk as bond yields continue to surge

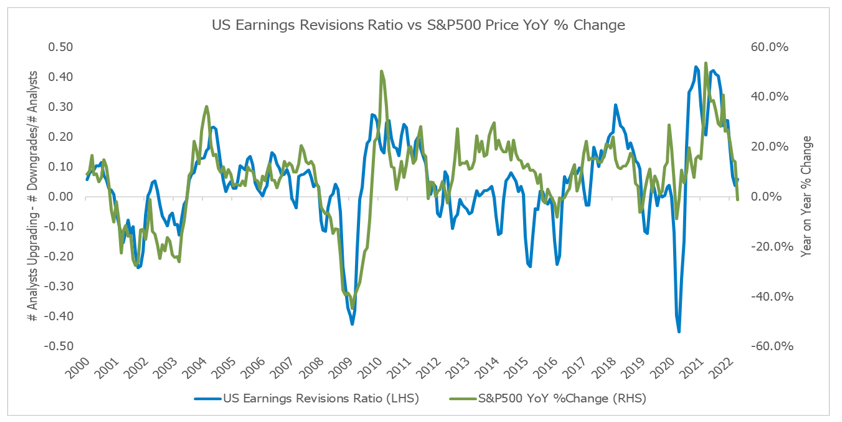

Source: Bloomberg, 10 May 2022 Investors' fears are shifting from inflation to growthUS GDP has surged past prior cycle peaks but is now decelerating sharply. Similarly, while 1Q22 earnings were modestly ahead of expectations on average, management commentary and guidance about the outlook has been increasingly cautious, prompting analysts to downgrade earnings forecasts for both '22 and '23. In fact, earnings revisions breath has been declining since August 2021 and has recently moved outright negative. Given the wide range of headwinds companies currently face, which include cost pressures, supply chain constraints, inventory build ups and potentially weaker demand from higher prices and lower global growth, it's likely that earnings revisions will remain negative for the foreseeable future. This has historically been associated with weak overall market performance (see below). Earnings Revisions and Price are highly correlated

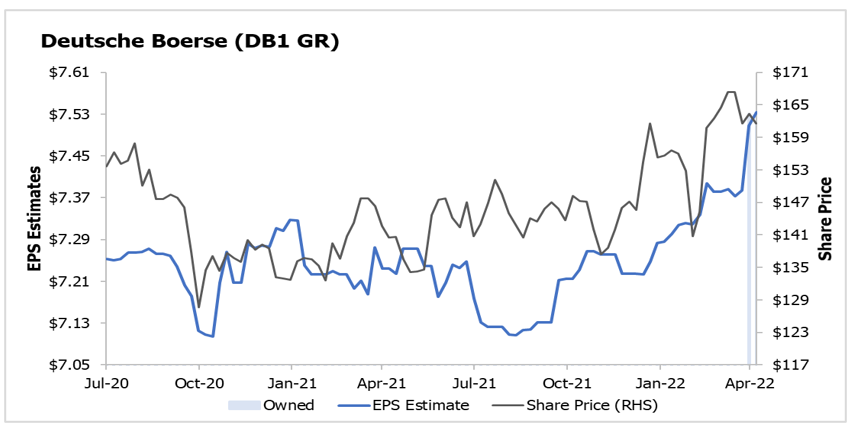

Source: Alphinity, Bloomberg, 3 May 2022 Earnings leadership has taken another step to being more defensiveAt a sector level, we have however seen a sharp contrast with the classic defensive sectors, such as Utilities and Consumer Staples outperforming the overall market year to date, driven by a superior ratings performance as well as better earnings revisions versus their cyclical peers and the broader market (excluding the Energy and Materials). Defensives have a strong track record of outperforming during slowing growth/recessionary periods, a relative safe-haven within periods of market stress. With a broad range of defensives already reflecting these benefits in relatively high valuations, active investors need to remain nimble and look for new opportunities. Some of these might not be seen as typical defensive plays, such as Merck & Co referred to below, but they offer defensive characteristics that should bode well in a volatile environment. One such defensive earnings leader is Deutsche Boerse. Just as in a dodgeball game, there are certain times in the market cycle when it is not always about running the fastest, but also about finding the best places to hide. Deutsche Boerse- Leading stock exchange enjoying multiple cyclical & structural tailwindsDeutsche Boerse (DB1) is a high-quality owner of various key pieces of financial market infrastructure in Europe across pre-trading, trading & clearing and post-trading. These assets include Institutional Shareholder Services (ISS), Eurex (leading European financial derivative exchange), EEX (a commodities trading & clearing exchange), Xetra (cash equities) and Clearstream (a leading European settlement & custody provider). These businesses all tend to command dominant or leading market positions within their segments, and as such enjoy significant barriers to entry and high margins. These diversified businesses generate resilient mid-cycle digit % secular growth, which we expect to be further boosted by various cyclical tailwinds, including both higher interest rates and higher interest rate volatility, as well as further targeted M&A. Consequently, we expect the company to exceed management's net income growth target of 10% (CAGR) for FY19-23E. With positive earnings revisions and a relatively undemanding valuation multiple (current forward PE of ~21x), we continue to see more upside for DB1 in the current environment. Deutsche Boerse - More defensive Earnings supported by several cyclical and structural factors

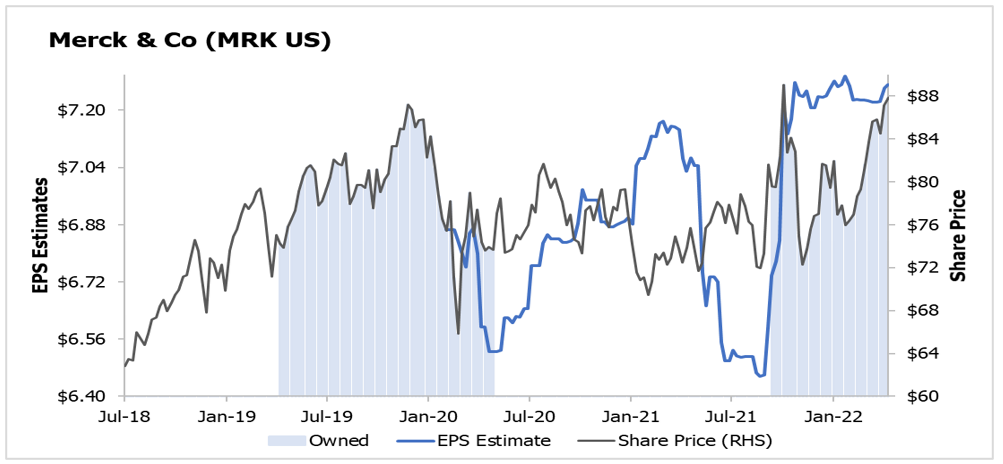

Source: Bloomberg, 10 May 2022 Merck & Co- A high quality defensive with flagship growth products & consistent earningsMerck & Co (MRK) is a global pharmaceutical company that delivers health solutions through its prescription medicines, vaccines, biologic therapies, animal health and consumer care products. MRK recently reported an impressive 1Q22 result with both revenue and earnings beating consensus expectations and the company raising 2022 guidance for both despite an expected FX headwind, driven by strength across the portfolio. Despite the relative outperformance and re-rating from 10x to 12x YTD, we maintain our position in this flagship defensive at this juncture with two main drivers for our investment case: 1) Product growth of the existing portfolio: Both the flagship growth products Keytruda (the largest selling drug in the world, innovative immuno-oncology, 30% of group revenues) and Gardasil vaccine (blockbuster vaccine against papilloma virus/cervical cancer, ~9% of group revenues) continue to grow ahead of expectations with their high quality Animal Health business (the third largest in the world) enjoying above market growth rates. 2) Business development: Management continue to look for new M&A opportunities to expand the business, underpinned by a strong balance sheet, with gearing at only ~2x EBITDA. Earnings growth underpinned by a portfolio of strong flagship products

Source: Bloomberg, 10 May 2022 Author: Elfreda Jonker, Client Portfolio Manager This information is for adviser & wholesale investors only |

|

Funds operated by this manager: Alphinity Australian Share Fund, Alphinity Concentrated Australian Share Fund, Alphinity Global Equity Fund, Alphinity Sustainable Share Fund |