|

Airlie Insight: The dominant narrative of 2022 for stocks Airlie Funds Management April 2022

|

|

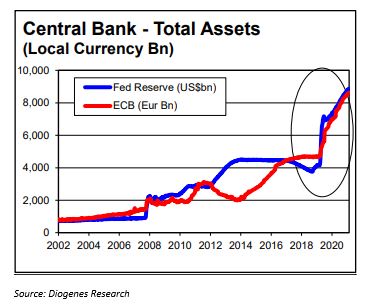

Last quarter we talked about the danger of following blindly (and reacting to) the 'dominant narrative' that is prevalent at any time in the market. However, there is no denying we are at the crossroads where inflation plus central bank tapering equals higher interest rates. Nothing encapsulates the excesses of the past decade better than the chart below showing central bank asset growth (i.e., buying assets/money printing). It seems unlikely that the similarity in the growth of global equity markets over this period is a coincidence.

Is this inflation spike transitory or structural? Some of it is clearly transitory driven by covid-19-affected supply chain issues; however, add in the energy and commodity price shock from the Russian invasion of Ukraine and suddenly 2022 looks different from most of the past decade. The 'dominant narrative' is all-encompassing, and the first impact is an increase in volatility in equity markets. In 2021, the S&P 500 Index had the fewest market drops (or 'drawdowns' in the professional lexicon) in recent history. It seems reasonable that the uncertainty of just how high rates will go will lead to a lot more volatility, and this has certainly been the case thus far in fiscal 2022. From recent peaks, the NASDAQ and S&P 500 fell 22% and 13% respectively but have now rallied 13% and 9%. The S&P/ASX 200 has done even better - falling 10% from the January high only to rally 10%, leaving it only 1% from the all-time high set in August 2021. The Australian market has been bolstered by its high weighting to banks and energy and resource companies. Many pundits are calling this sudden snap-back rally a 'dead cat bounce' due to perhaps a view that the Russian-Ukrainian situation evolves into some sort of truce hopefully soon. At that time the 'dominant narrative' will then return and take charge leading to slowing economic growth and possibly recessions. The chart below shows that it's certainly been the case that markets do not do as well when inflation is both rising and is above 3%. This is the exact opposite situation of the past decade where we've had falling inflation and below 3%. Not shown on the chart is that markets produce negative returns when inflation persistently exceeds 6%.

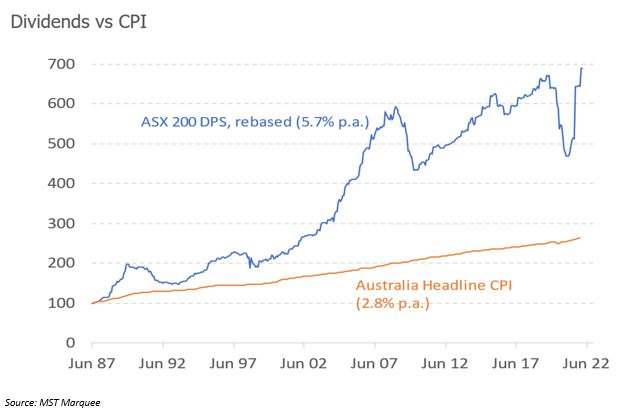

So, what does it all mean and what to do? Unfortunately, it's impossible to answer. We've met investors this year who have proudly told us they've gone to cash as the market hit the 10% drawdown because the 'dominant narrative' is obvious - equity markets will fall, economies will falter. They may ultimately be right, but I've wondered what they make of the rally back to within 1% of all-time highs? The performance of non-profitable tech, the return of so-called value stocks, and the valuation implication of higher rates lead us to think that the one-way trip of the market over the past decade and the return of volatility may mean stock-picking comes to the fore and there are increasing opportunities for active managers to differentiate themselves. Also not forgetting the fact that the equity market is the best place to counter inflation. The chart below shows that just the dividends alone from listed Australian equities have preserved investors' buying power over the long term.

With all the doom and gloom and headline fodder provided by the above debates it's easy to forget that the Australian economy remains in good shape. The strength is widely spread across the economy: from households enjoying strong employment prospects with wage rises, increasing house prices, falling mortgage repayments (for now), to miners reaping solid commodity prices, farmers rebounding from the drought, and banks experiencing renewed credit growth. So where to from here? The case for further strength in equity markets is a relative one. Absolute valuations are high relative to history and are vulnerable overall to higher interest (discount) rates. The energy shock brought about by Russia's invasion of Ukraine and higher commodity prices generally are supportive in the short term to our resources-heavy market. Also, as the chart below shows; equally supportive is the forecast dividend yield available from the ASX 200 - a healthy dividend return of 4.0% - making it the equal-highest-yielding equity market in the world. Calendar year 2021 was a year of significant capital return for investors, as many ASX companies were carrying surplus capital: banks, miners, retailers, and many industrials had seen dramatic balance sheet improvements over the past 18 months. We expect continuing healthy capital returns to shareholders, notwithstanding the global uncertainty.

By Matt Williams, Portfolio Manager Funds operated by this manager: Important Information: Units in the fund(s) referred to herein are issued by Magellan Asset Management Limited (ABN 31 120 593 946, AFS Licence No. 304 301) trading as Airlie Funds Management ('Airlie') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to an Airlie financial product or service may be obtained by calling +61 2 9235 4760 or by visiting www.airliefundsmanagement.com.au. Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of an Airlie financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. Airlie makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Airlie. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. Any third party trademarks contained herein are the property of their respective owners and Airlie claims no ownership in, nor any affiliation with, such trademarks. Any third party trademarks that appear in this material are used for information purposes and only to identify the company names or brands of their respective owners. No affiliation, sponsorship or endorsement should be inferred from the use of these trademarks.. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Airlie. |

.JPG)