No events currently listed.

Find a Fund

Peer Group Analysis View All»

| Index Selector Links | 1 Year | 3 Year | 5 Year |

|---|---|---|---|

13.11% |

8.94% |

8.41% |

|

3.94% |

4.79% |

2.54% |

|

-17.81% |

19.33% |

6.15% |

|

7.15% |

7.37% |

2.40% |

|

10.94% |

7.63% |

6.05% |

|

22.58% |

12.46% |

9.16% |

|

6.18% |

10.38% |

6.62% |

|

18.67% |

12.22% |

4.89% |

|

5.61% |

6.85% |

6.32% |

|

12.88% |

13.46% |

8.29% |

|

8.85% |

8.32% |

4.17% |

|

21.32% |

15.17% |

7.09% |

|

13.68% |

10.37% |

10.19% |

|

10.93% |

8.05% |

5.65% |

|

7.03% |

8.32% |

7.11% |

|

-0.18% |

-0.64% |

1.23% |

|

8.56% |

8.92% |

7.82% |

Hedge Clippings

5 Jun 2026 - What a Structural Shift in Yields Means for Portfolios

|

What a Structural Shift in Yields Means for Portfolios JCB Jamieson Coote Bonds May 2026 (6-minute read) Government bond yields around the world have reached decade highs, driven by higher energy costs and potentially ongoing inflationary pressures stemming from the U.S.-Iran conflict and disruption to global oil supply routes. Beyond the immediate conflict, there are structural reasons yields may stay elevated. Government balance sheets across many advanced economies are increasingly stretched, with debt-fuelled expenditure supporting ambitious policy reforms - from defence to energy transition. Beyond determining government borrowing costs, yields play a central role within the financial system. As the risk-free rate of interest, they underpin the cost of capital across the economy, meaning the current move higher in yields has implications well beyond bonds, reshaping valuations across equities, credit and real assets. If government bond yields stay higher for longer across most of the world, the cost of capital will also rise inexorably. Higher yields translate directly into higher discount rates, and that matters for every asset in a portfolio. Whether its equities, credit or property, valuations are derived by discounting future cash flows at the risk-free rate plus a premium for investment risk. When that base rate moves higher, asset prices adjust lower. A higher cost of capital will likely prompt investors to revise their hurdle rates higher for all investment opportunities and may suggest a more cautious approach to investment risk in general. This could reveal vulnerabilities across asset classes which have benefited from a secular decline in interest rates, and therefore the cost of capital, over the past several decades. Infrastructure, private credit and private equity have benefited from the valuation effects of a relatively low cost of capital, but this is now set to change as higher hurdle rates and revaluations unveil which asset classes and investment strategies can continue to sustain and deliver compelling risk-adjusted returns, and which will struggle to do so going forward. "When the risk-free rate rises, every asset is repriced." Higher bond yields increase discount rates across equities, credit and property--resetting valuations and raising hurdle rates for all investments. Turning to domestic developments, this month's Commonwealth Budget brought significant tax reform and policy announcements alongside a compositional change in revenue and expenditure forecasts that led to modest improvements in the budget balance over the next decade. Drilling into the tax policy changes, reforms to capital gains tax (CGT) and negative gearing may make property as an asset class less attractive to investors and dampen investment activity in the property market. Some analysts forecast a consequent moderation in house prices across the country and frame the contractionary economic effects of the tax reforms as akin to that of one or two RBA rate hikes, foreshadowing the conclusion of an already well progressed RBA rate hike cycle. As investors reassess their portfolios for tax efficiency under the new CGT regime, fixed income and other income generating assets such as high dividend domestic equities could be well placed to benefit from this shift in focus. Ultimately, the budget forecasts depict Australia's fiscal conditions in a highly favourable light relative to our peers, and re-affirms that Australia's government debt remains very low by global standards. For investors, this environment calls for a fundamental reassessment of portfolio construction - where return is coming from, what risks are being compensated, and whether allocations built in a low-rate world remain fit for purpose in a higher-rate one. Funds operated by this manager: CC Jamieson Coote Bonds Active Bond Fund (Class A) , CC Jamieson Coote Bonds Dynamic Alpha Fund This information is for professional and wholesale investors only and has been prepared by JamiesonCooteBonds Pty Ltd ACN 165 890 282 AFSL 459018 ('JCB'). Channel Investment Management Limited ACN 163 234 240 AFSL 439007 ('CIML') is the Responsible Entity and issuer of units for the CC JCB Active Bond Fund ARSN 610 435 302, CC JCB Global Bond Fund ARSN 631 235 553 and the CC JCB Dynamic Alpha Fund ARSN 637 628 918 (collectively 'the Funds'). Channel Capital Pty Ltd ACN 162 591 568 AR No. 001274413 ('Channel') provides investment infrastructure and distribution services for JCB and is the holding company of CIML. |

8 Apr 2026 - Q&A: Four forces currently shaping equity markets

|

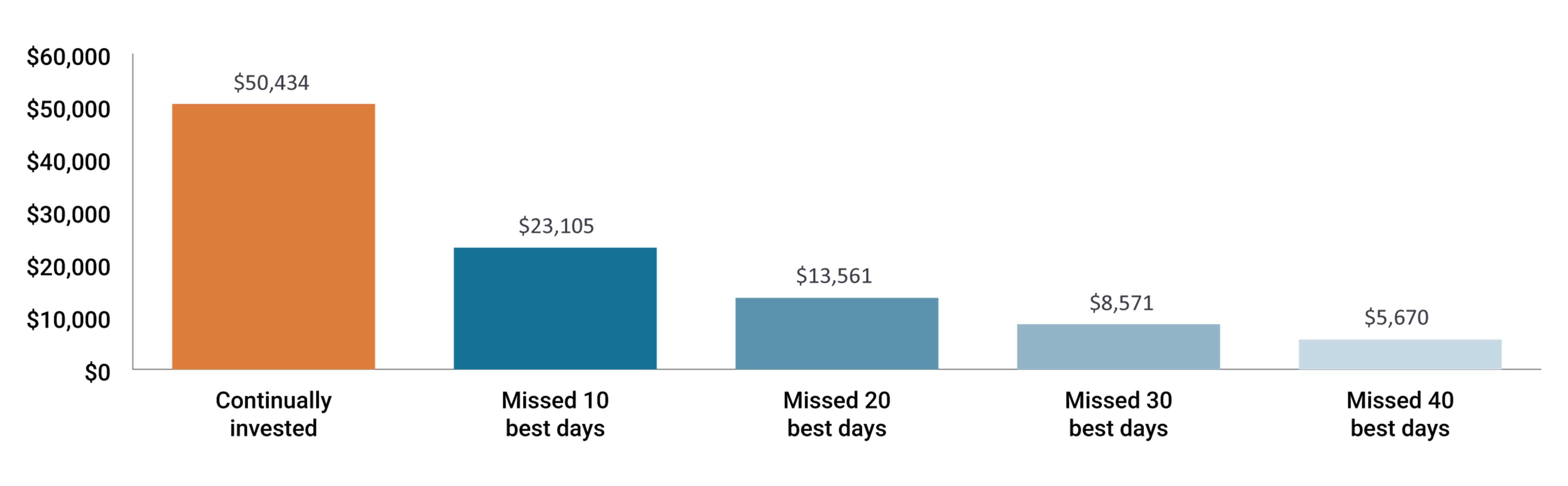

Q&A: Four forces currently shaping equity markets JCB Jamieson Coote Bonds March 2026 (6-minute read) In this Q&A, Portfolio Managers Jeremiah Buckley and Michael Keough share their perspectives on geopolitical uncertainty, why they remain constructive on earnings growth, where they see inflation settling, and what AI disruption means for software. Q: Geopolitical events like the war in Iran can move markets quickly. How do you approach investing through that kind of uncertainty? Michael Keough: Geopolitical events can carry real tail risks that are hard to model, but the key question is what will the sustained economic impact actually be? Often, it's more limited than the initial reaction suggests. Our current read is that this appears to be a shorter-duration campaign focused on specific military infrastructure rather than broader energy systems. If the Strait of Hormuz reopens in the near future and energy infrastructure is not significantly disrupted, we expect the oil price spike is likely to be temporary but potentially lasting the first half of the year. We are also mindful that the administration must balance their objectives for this campaign with the upcoming midterm elections. It also helps to consider where we started. Oil had been at fairly low levels, around $50 to $60 a barrel, and the world was already oversupplied by roughly 2 million barrels a day heading into this. Iran produces about 3 million barrels a day, and we do not expect a sustained removal of that supply. More broadly, our approach during periods like this is to lean into quality and use volatility as an opportunity. In our asset allocation portfolios, we came into 2026 with a meaningful overweight to equities based on our view that earnings growth would remain positive. We didn't anticipate this level of geopolitical disruption, but we don't see it materially changing the fundamental picture for the year, which is supported by a number of tailwinds. If markets continue to sell off, our bias is to add to equities selectively. It's worth noting the opportunity cost of becoming too defensive. Over the last couple of years, being too conservative, such as holding too much cash or underweighting equities, meant missing the recoveries that drove the bulk of returns. Historically, a handful of strong market days have contributed an outsized share of long-term equity returns, and investors need to be positioned to capture them. Exhibit 1: Value of a hypothetical $10,000 investment in the S&P 500® Index from 1999 - 2024.

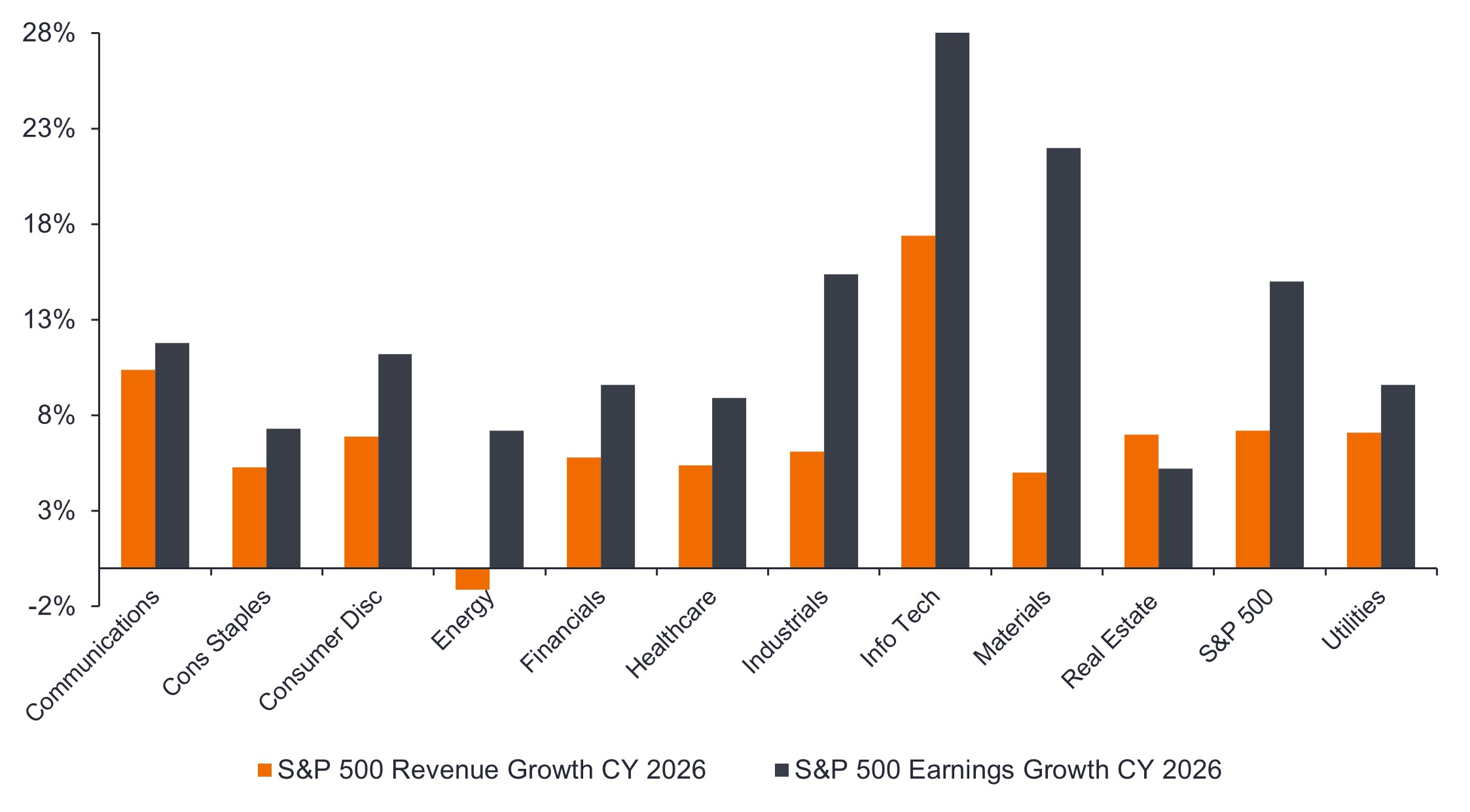

Q: You mentioned the fundamental picture remains intact. What gives you confidence, and where are you seeing the opportunity? Jeremiah Buckley: The earnings story has broadened considerably, and that's central to our constructive view. AI infrastructure and large internet platforms have been growing strongly, but they are no longer carrying the market alone. Other sectors have started contributing meaningfully, including biotech, healthcare equipment, digital payments, and financial services. Innovation in these areas is translating into earnings. Technology-related capital expenditures are contributing roughly a third of GDP growth in 2026, and the benefits are flowing well beyond the infrastructure build itself. Exhibit 2: Strong revenue and earnings growth is expected broadly across sectors for 2026

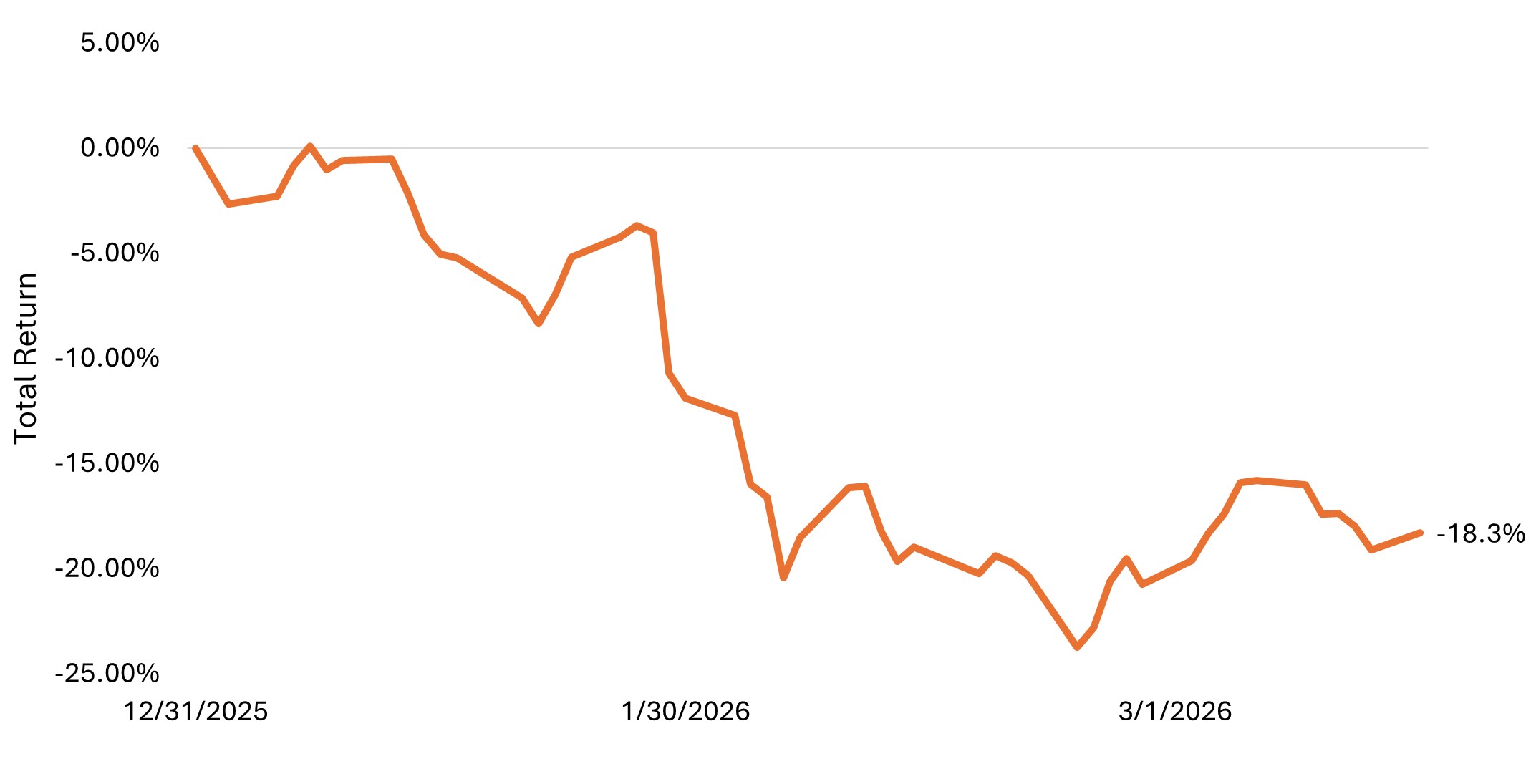

Source: Bloomberg, as of January 2026. CY=calendar year. There are also tailwinds that tend to get overshadowed by headlines from geopolitical events. Tax reform, deregulation, and the early productivity gains from technology investment are all constructive for corporate earnings and haven't gone away. We can also be active in how we are positioning through near-term volatility. In 2025, we used periods when cyclical sectors were being indiscriminately sold off to rotate into more cyclical exposure. We think a similar dynamic may be developing now, and we'll be looking for opportunities to act on it. Q: There's been a lot of debate about whether inflation can get back to 2% or whether 3% is the new normal. What is your view? Keough: We think getting back to 2% is going to be difficult to sustain. Structural pressures remain, including supply constraints, a modest degree of deglobalization, higher energy prices, and slower population weighing on labor. AI could help offset that last point, but probably not enough on its own unless productivity gains substantially exceed current expectations. That said, some of the forces that held inflation elevated are fading. Tariff-related goods inflation is being lapped, year-over-year comparisons are getting easier, and some tariffs have since been reduced by court rulings. Those headwinds are becoming less of a factor as the year progresses. Our base case is around 2.5%, with long-term inflation expectations closer to 2%, and we'd argue that's a reasonably healthy environment for equities. It gives companies a bit of pricing power without forcing the Federal Reserve to tighten. Given the other tailwinds supporting earnings growth, it fits into what we still see as a constructive backdrop. Q: As AI is adopted more broadly, risks to certain parts of the market are becoming clearer. How are you thinking about those risks, and what does it mean for software? Buckley: Having watched many technology cycles, we do think there is some degree of overhype embedded in this one, and we're watching returns on invested capital closely across the infrastructure build. Spending will plateau at some point, and the market will need to digest it. The early evidence on returns is encouraging. Meta's advertising revenue growth is perhaps the clearest example of AI investment generating real, measurable results, but that is one data point in an evolving story. Where we're seeing the hype manifest most acutely is in the market's treatment of software. The software index is down roughly 18% year to date as investors price in disruption from AI. Some of that concern is legitimate, but we don't think the market is distinguishing well between companies that will be genuinely disrupted and those that are adapting effectively. Exhibit 3: S&P Software & Services Industry Index, year-to-date through 16 March 2026

Source: Bloomberg, as of 17 March 2026. The S&P Software & Services Select Industry Index comprises stocks in the S&P Total Market Index that are classified in the GICS Application Software, Interactive Home Entertainment, IT Consulting & Other Services and Systems Software sub-industries. For high-quality software businesses, there's more to their competitive position than the software itself - distribution, customer relationships, and implementation support all factor into the equation. Those advantages don't disappear overnight. We're starting to see some stabilization in the space, but the longer-term sorting out process is underway, and we expect it to create real opportunities for active management. IMPORTANT INFORMATION Artificial intelligence ("AI") focused companies, including those that develop or utilize AI technologies, may face rapid product obsolescence, intense competition, and increased regulatory scrutiny. These companies often rely heavily on intellectual property, invest significantly in research and development, and depend on maintaining and growing consumer demand. Their securities may be more volatile than those of companies offering more established technologies and may be affected by risks tied to the use of AI in business operations, including legal liability or reputational harm. Equity securities are subject to risks including market risk. Returns will fluctuate in response to issuer, political and economic developments. Funds operated by this manager: CC Jamieson Coote Bonds Active Bond Fund (Class A) , CC Jamieson Coote Bonds Dynamic Alpha Fund This information is for professional and wholesale investors only and has been prepared by JamiesonCooteBonds Pty Ltd ACN 165 890 282 AFSL 459018 ('JCB'). Channel Investment Management Limited ACN 163 234 240 AFSL 439007 ('CIML') is the Responsible Entity and issuer of units for the CC JCB Active Bond Fund ARSN 610 435 302, CC JCB Global Bond Fund ARSN 631 235 553 and the CC JCB Dynamic Alpha Fund ARSN 637 628 918 (collectively 'the Funds'). Channel Capital Pty Ltd ACN 162 591 568 AR No. 001274413 ('Channel') provides investment infrastructure and distribution services for JCB and is the holding company of CIML. |

Past performance is no guarantee of future results. Investing involves risk, including the possible loss of principal and fluctuation of value.

Past performance is no guarantee of future results. Investing involves risk, including the possible loss of principal and fluctuation of value.

4 Mar 2026 - Volatility Is Information: Reading the Signals Beneath the Surface

|

Volatility Is Information: Reading the Signals Beneath the Surface JCB Jamieson Coote Bonds February 2026 (3-minute read) The investment outlook this year remains shrouded by uncertainty, accompanied by elevated volatility in expected returns. Markets are searching for direction, and investors are navigating an environment where conviction feels harder earned. Volatility, of course, wears many faces. We can observe it in the lived experience of asset price return variability across securities, sectors and markets. Or we may deduce the anticipated range of returns over the next week, month or quarter from options prices. Either way, the direction, size and interdependencies (correlations) of movements in market pricing at all frequencies can provide important signals for astute investors. Volatility is not simply noise, it is information. Right now, equity prices, cryptocurrencies, and precious metals are relatively more volatile. Yet in contrast, most bond markets remain curiously subdued. Yields remain broadly rangebound, only tentatively challenging the edges of recent ranges, reticent to enter an elusive new regime or steady state. That restraint in bond markets is notable, and perhaps more revealing than the visible turbulence elsewhere. After hiking rates earlier this month, RBA Governor Michelle Bullock stopped short of offering explicit forward guidance, indicating that the Monetary Policy Board is heavily data dependent. This suggests further policy restriction may have limited efficacy in controlling persistently above-band inflation back to the target range. Australian government bond yields decreased markedly in response, and the market is paring back pricing for hikes and beginning to tentatively pre-empt future rate cuts next year. The tone has shifted, from further restriction to a growing debate about how long policy will need to remain restrictive at all. More broadly, attention is turning to the Government for direction ahead of the upcoming Federal Budget. There is growing recognition that boosting labour productivity through innovation, enhanced competition and meaningful structural and tax reform remains the only sustainable path to higher national income and improved living standards for all Australians. Meanwhile, across the Pacific in the U.S., economic activity continues to show surprising resilience. January brought unexpectedly strong employment growth, thanks in part to seasonal factors (despite large historical downward revisions). Price pressures, meanwhile appear to be cooling, although the data remains messy and influenced by lingering U.S. federal government shutdown-related disruptions. The result? Short-dated Treasury yields have drifted to multi-year lows, reflecting cautious optimism among investors. The market has almost priced for three U.S. Federal Reserve rate cuts this year under U.S. Federal Reserve Chair nominee Kevin Warsh, although the upcoming midterm elections loom large over the U.S. macro outlook and the Trump administration's near-term policy priorities. In Europe, inflation appears to be well controlled and the European Central Bank comfortably on hold, but recent geopolitical events have raised existential questions around the protection and advancement of national and regional interests, and defence and security strategy. While this may be the quintessential European moment to rebalance the world order away from U.S. dominance if traditional allegiances like NATO are set to be dissolved, there have been fundamental disagreements between Germany and France around policy priorities to restore competitiveness and how to fund quickly growing defence expenditures. Yields on German government bonds have also dropped materially in recent weeks. In Japan, the Liberal Democratic Party lead by Sanae Takaichi has emerged victorious from lower house elections. Takaichi's expanded mandate and firm command over political and economic power (for instance, Japan's central bank is not independent of government) after her historic win, combined with a sense of renewed optimism across global markets that the realisation of her vision for Japan will not unduly impact interest rates and exchange rates beyond what is already envisaged, has led to a relief rally in Japanese Government Bonds after a tumultuous January. What signal can we draw from the subdued historical measures of volatility across bond yields, especially when viewed against the domestic and global macro backdrop? There are three key takeaways. First, periods of volatility and uncertainty (whether obvious or hidden) can bring significant opportunity to generate attractive returns for those who act thoughtfully. Second, fortune rewards the diligent and there are only downside risks to complacency. And third, and most importantly, diversification, both within and across asset classes and sectors is the primary means with which to dampen the effects of volatility and protect long-term investment outcomes. Volatility may rattle markets, but it also sharpens our focus, driving better portfolio construction and smarter asset allocation decisions. Funds operated by this manager: CC Jamieson Coote Bonds Active Bond Fund (Class A) , CC Jamieson Coote Bonds Dynamic Alpha Fund This information is for professional and wholesale investors only and has been prepared by JamiesonCooteBonds Pty Ltd ACN 165 890 282 AFSL 459018 ('JCB'). Channel Investment Management Limited ACN 163 234 240 AFSL 439007 ('CIML') is the Responsible Entity and issuer of units for the CC JCB Active Bond Fund ARSN 610 435 302, CC JCB Global Bond Fund ARSN 631 235 553 and the CC JCB Dynamic Alpha Fund ARSN 637 628 918 (collectively 'the Funds'). Channel Capital Pty Ltd ACN 162 591 568 AR No. 001274413 ('Channel') provides investment infrastructure and distribution services for JCB and is the holding company of CIML. |

6 Feb 2026 - 2026: A Year of Calm Before the Market Storm?

|

2026: A Year of Calm Before the Market Storm? JCB Jamieson Coote Bonds January 2026 (3-minute read) Top of mind this summer, more so than any other recent summer, is the extent to which the recent remarkable streak of performance across almost all asset classes powers ahead, or loses momentum. As we enter 2026, markets are tinder-dry with risk, and for now the winds are calm. Since last month, global markets have seemingly settled into a tranquil yet uneasy holding pattern, having made considerable progress to date in navigating the turbulence presented by tariffs, policy uncertainty, geopolitical travails, and stagflation. What might occur in the year ahead to potentially ignite a sparkcould it be another policy surprise from the U.S. Administration, geopolitical tensions, or macroeconomic developments? Let's map out and break down the key risks that might cast a long shadow over current pricing in global markets. In the U.S., markets appear to be much less responsive than usual to surprises in economic data after the U.S. Federal Government shutdown late last year. This stands to reason the U.S. Administration has challenged the independence of not only the U.S. Federal Reserve, but ostensibly also the civil servants at the Bureau of Labor Statistics and the Bureau of Economic Activity who produce the data releases. Some believe, and there is very little evidence that contradicts their view, that President Trump intends to do what he sees as necessary to frame the macro outlook and asset price dynamics in the best possible light for the Grand Old Party ahead of this year's midterm elections. In China, authorities have held back on announcing significant fiscal stimulus, instead preferring to outmaneuver the U.S. on trade and foreign policy, particularly with respect to rare earths supply. All the while President Xi has tirelessly advanced China's economic and strategic interests, most recently allowing the renminbi to reach its strongest level against the U.S. dollar in the past several years, and applying ever-increasing pressure on Taiwan's independence (given its semiconductor fabrication infrastructure after the U.S. set a dangerous precedent in Venezuela, which has the world's largest oil reserves). In Japan, Prime Minister Sanae Takaichi has just called snap elections in an effort to shore up support for planned fiscal stimulus and policy support intended to ease the cost of living. However, she must also contend with a lack of macro policy coordination with yen weakness; a reticence from the Bank of Japan to continue tightening policy and preserve its "virtuous cycle" between activity, wages and prices; and ceaselessly rising Japanese government bond yields. This is a potent combination that also indirectly led to the downfall of the Prime Minister's predecessor, Shigeru Ishiba. And these thematic patterns are repeated in kind throughout Europe, Canada and the UK: unsteady political leadership, complex macro and broader policy challenges, and the fragmentation of the regional and international order via superficial cooperation amid divergent national interests. All the while, risk assets are priced for continuing material gains, and valuations are stretched to record levels, whilst central banks globally are making marginal adjustments to gradually recalibrate policy towards the elusive, ever-shifting mirage of neutrality loosening here, tightening there all second order given the macro backdrop described above. When could valuations adjust and risk potentially be adjusted or even repriced? It is the critical question we are all focused on this year in global markets. Pricing may well continue its onward march higher this year, but after a period of such impressive asset market performance, history would suggest the largest gains are behind us. Coupled with the possibility of complacency amongst market participants who have become accustomed to outsized gains in recent times, this sets the stage for an interesting and eventful year ahead and does create opportunities for those prepared to question the current consensus that underpins market pricing. Funds operated by this manager: CC Jamieson Coote Bonds Active Bond Fund (Class A) , CC Jamieson Coote Bonds Dynamic Alpha Fund |

28 Nov 2025 - Markets Brace for Patchy US Data and Policy Uncertainty

|

Markets Brace for Patchy US Data and Policy Uncertainty JCB Jamieson Coote Bonds November 2025 (3-min read) The latest official U.S. macroeconomic data readings, to be imminently released, are front of mind for central banks and global financial markets. The U.S. federal government shutdown has had the effect of delaying several significant data releases on inflation, labour markets and economic activity. However, with the shutdown ending, many anticipate a flurry of data. Global markets are closely watching the imminent release of delayed official macroeconomic statistics from the Bureau of Economic Analysis, the Bureau of Labor Statistics and other key agencies. That said, the scope of the releases is yet to be determined, and some data may never be released, perhaps due to the lack of staffing to conduct surveys and collect information. In the latest developments, the White House has indicated that the October consumer prices index and employment situation reports (which includes the critical figures on the change in non-farm payroll employment) likely will not be released. This leaves policymakers and markets in a quandary - does the U.S. administration have something to hide, or is it simply not possible or feasible to produce retrospective data during the circumstances of a record government shutdown? There are a range of views on what might transpire in the months ahead. Some surmise that the U.S. economy is poised to pick up, with private sector measures of payroll growth slowing but remaining resilient. On this view, sticky services prices and goods reflation are driving persistent upside risks relative to the U.S. Federal Reserve's inflation target. Asset prices are adding fuel to the engine of growth - exuberant stock market and credit valuations are buoying confidence and driving a continuation of U.S. dynamism and exceptionalism. Others highlight that U.S. economic activity remains remarkably concentrated in capital expenditures relating to the AI sector, without which the U.S. is either staring down a recession or has already entered one. Pervasive and widespread downside risks to the labour market are seen as the justification for further policy easing to support a fragile and fractured heartland, with the American dream only barely alive for many lower and middle-class families facing hardship and an uncertain future. Caught somewhere in the middle between these polarised narratives, markets are nervously awaiting official readings on the underlying pulse of U.S. macroeconomic conditions, and the likely policy responses from the Federal Reserve and U.S. Administration. Sound risk management principles suggest that U.S. fiscal and monetary policymakers are likely to discount individual data points on employment growth and core inflation �' even if they prove benign �' in order to sure up consumer and investor confidence. This is an oft-repeated dynamic at times of heightened uncertainty - policymakers tend to focus on their (admittedly subjective and error-prone) interpretation of the underlying momentum and pulse from the data. Markets don't necessarily fare any better. Pricing often over-reacts on immediate attention-grabbing headlines. The unambiguously strong domestic employment figures for October are another manifestation of this phenomenon, and followed an unquestionably weak print in September. The RBA will undoubtedly be encouraged by the fact that, inflation aside, its near-term forecasts have been progressively realised to date, as markets reprice away from further policy easing. As always, the truth is somewhere in the middle of all of these competing forces, and it pays to take out insurance against tail risks being realised. Following the same principles of risk management and least regret alluded to above, investors searching for stability in these uncertain times may wish to consider defensive allocations as part of their investment strategy, while staying grounded in fundamentals and attentive to policy signals to make informed, confident decisions. Funds operated by this manager: CC Jamieson Coote Bonds Active Bond Fund (Class A) , CC Jamieson Coote Bonds Dynamic Alpha Fund |

26 Mar 2025 - Trump's 'Period of Transition': Economic Reset or Market Risk?

|

Trump's 'Period of Transition': Economic Reset or Market Risk? JCB Jamieson Coote Bonds March 2025 Park your politics at the door, the changes that are occurring in the US, and thereby global markets - rightly or wrongly - are reshaping the financial market landscape at a frightening speed. Market uncertainty has surged following recent developments in US President Donald Trump's trade and economic policies. Investors hoping for US government support are likely to be bitterly disappointed by US Treasury Secretary Scott Bessent's remarks, as he dismissed the 10% equity selloff as "healthy" and "normal." Bessent further suggested that a market correction was necessary to prevent against euphoric markets, which he warned could trigger a financial crisis. He also cautioned that there were "no guarantees" that the US economy would not fall into a recession. These comments follow on from President Trump's comments last week, in which he asserted that the economy had to go through a "period of transition," arguing that previous growth had been "fake" under excessive government spending. This insistence ― that some 'short term pain for long term gain' has been sighted as the cause for weakness in equity markets. The Trump administration's efforts to slow the economy by cutting government spending and disrupting global relationships and trade agreements continue to unsettle investors. These developments have seen market and economic forecasters rapidly slashing their estimates for 2025, chopping any kind of positive outcomes from the suggested economic path. Status quo, or a weakening in the economy now seems to be the destination ahead if the current policy combinations remain in play - and potentially a significant weakening at that. This has been jolting for many market watchers who felt 2025 would be a constructive year under the business-friendly administration of Trump, especially given previous claims that the US economy was "exceptional." After a surge of optimism in post-election data, fuelled by expectations that tax cuts and deregulation would herald a new economic boom--sentiment has taken a sharp turn. Soft survey data has completely collapsed, taking the widely watched Atlanta Federal Reserve GDPNow tracker, a predictive tool which tries to read the health of the current economy in real time without the usual lags, to a scary -2.4% reading. This suggests the economy has hit stall speed and then some. Future outlook and investor cautionWe are yet to see such deterioration in the 'hard' data, but it does require close attention for investors, as the market will likely be punishing of anything suggestive that growth is slipping, such as falling retail sales or rising unemployment. While there is still a collective concern around the inflation outlook, especially as inflation expectations have risen, incoming inflation data shows signs of moderating, supported by declining oil prices and weaker demand for travel. However, falling growth indicators are likely to overtake inflation concerns in driving market sentiment. Historically, when growth falters, inflation is usually snubbed out very quickly due to demand destruction. Such a development would likely activate the US Federal Reserve (US Fed), which has remained in a holding pattern after last year's 100 basis point rates cuts - a non-stimulatory cutting cycle to match victories in fighting excessive inflation. The US Fed had moved to a "watch and see" holding pattern, keen to monitor the impact of Trump's policies on the economy. If economic conditions evolve with a material downside skew, a key question for markets will be how US Fed Chairman Jerome Powell responds to support the economy, particularly at a time when potential tariff-induced price rises could temporarily push inflation higher. This is a difficult policy combination, but the US Fed can potentially look through such a development, as many tariffs have yet to make a significant impact. In a "Trumpian" world, these tariffs might even fail to materialise just as quickly as they were enacted. The extent to which tariffs may drive inflation remains highly uncertain, providing Powell some wiggle room with US Fed policy. However, such look through is unlikely on the growth front. We have written at length on the feedback loops from stalling growth (remember the terminologies of 'hard', 'soft' or 'no' landing). If growth stalls it can be very difficult to reactivate without a 'stimulatory'' rate cutting cycle of significant magnitude. That is hardly a base case, but that outcome is growing in probability as the left tail of significantly higher rates is mitigated by the DOGE (Department of Government Efficiency - led by Elon Musk) effect on the economy. While risks remain, the prevailing sentiment suggests that authorities are prepared to act if markets experience deeper corrections. However, they are reluctant to overstep unless the situation becomes truly dire. Otherwise, further corrections remain "healthy". This is a colossal change worthy of your attention. As such, any notion of a Trump "put" seems further away for now. In other words, the idea of Trump stepping in to prop up markets in a crisis is less immediate than previously thought. In light of the uncertainties, particularly around the evolving economic landscape and potential policy shifts, investors need to be cautious and reassess their exposure to sectors vulnerable to policy changes, trade disruptions, and global economic slowdowns. While the US Fed's cautious stance offers some breathing room, the lack of definitive government support raises the likelihood of volatile market conditions ahead. Charlie Jamieson, Chief Investment Officer Funds operated by this manager: CC Jamieson Coote Bonds Active Bond Fund (Class A), CC Jamieson Coote Bonds Dynamic Alpha Fund, CC Jamieson Coote Bonds Global Bond Fund (Class A - Hedged) |

20 Feb 2025 - Trump effect, policy uncertainty and government spending - Key themes for bond markets in 2025

|

Trump effect, policy uncertainty and government spending - Key themes for bond markets in 2025 JCB Jamieson Coote Bonds January 2025 As we enter 2025, investors are navigating a shifting landscape shaped by evolving central bank policies, economic uncertainty, and fiscal dynamics. While challenges remain, there are also opportunities on the horizon. Charlie Jamieson, Chief Investment Officer, explores the key themes set to influence bond markets this year from interest rate movements to government spending and policy direction. Below is a brief summary. Summary of key themes for bond markets in 2025Recap of 2024: The bond market faced underwhelming performance despite global rate cuts. A key driver of this was a sell-off in long-dated bonds, spurred by expectations of continued US fiscal spending. In Australia, the Reserve Bank of Australia (RBA) held interest rates steady throughout 2024 but is expected to begin cutting in February 2025, which should provide support to bond markets given current valuations. Global economic outlook: The outlook for 2025 remains divided, particularly with the Trump administration now in its second term. The US economy continues to perform well, spurred on by the "Trump effect" of strong business optimism. However, economic conditions in the rest of the world are weaker, with Europe, Canada, Australia, and New Zealand all expected to cut rates further. Policy uncertainty: While markets had hoped for more clarity, there is still little certainty around economic policy direction. A major area of concern is the potential for increased tariffs, which could reintroduce inflationary pressures. Although not yet confirmed, the expectation is that tariffs will be implemented and may rise throughout the year. This, combined with Trump's stated preference for lower inflation and interest rates, creates a complex policy landscape that could have significant market implications. Fixed Income performance^: For fixed income investors, returns are expected to be relatively solid. Cash returns should remain in the 3-4% range, while bond market performance could reach 5-6%, depending on yield movements. Government spending and fiscal policy: In both the US and Australia, public sector spending has been a major driver of economic activity. However, with concerns over inflation and fiscal sustainability, there is increasing pressure to rein in spending. As investors navigate 2025, market divergence, policy uncertainty, and fiscal decisions will be key factors shaping the bond market outlook. ^ Recipients should not rely on this information in making investment decisions. The information here is illustrative and shall not be relied upon as a promise or representation of past or future performance. All investments contain risk.Charlie Jamieson, Chief Investment Officer Funds operated by this manager: CC Jamieson Coote Bonds Active Bond Fund (Class A), CC Jamieson Coote Bonds Dynamic Alpha Fund, CC Jamieson Coote Bonds Global Bond Fund (Class A - Hedged) |

17 Jan 2025 - The Australian: Economic uncertainty driven by a Trump guessing game

|

The Australian: Economic uncertainty driven by a Trump guessing game JCB Jamieson Coote Bonds November 2024 The year 2025 is shaping up to be one of great uncertainty, with global politics driven by the incoming Trump administration likely leading significant market gyrations and increased asset class volatility. Trump US exceptionalism is expected, but the actual policies used to generate "make America great again" are still the source of debate only a week from the presidential inauguration. Many permutations and combinations for policy are possible and the medium-term impacts may be quite different to the "shoot first and ask questions later" moves of modern markets as we are seeing with US equities back towards election day valuations. Expectations for continued earnings and growth are high after two exceptional years for risk assets, while longer-dated US fixed income yields have increased despite the US Federal Reserve and many other global central banks cutting interest rates in 2024. This is historic in and of itself (usually rates fall as funding rates are lowered), driven by concerns about US fiscal spending and inflation impacts that continue an unsustainable pathway. Will the change in the US government generate any fiscal prudence? Will the Department of Government Efficiency succeed in curbing excessive fiscal spending to reduce inflation fuelled by excessive government spending? And what could be the growth implications of this withdrawal of government support from the economy? These remain key questions for bond yields which, if they rise, could dampen the outlook for all asset markets by increasing the global cost of funding. Australia finds itself heavily influenced by these global trends yet uniquely positioned between contrasting economic realities. In the US, bond yields are increasing, with 10-year Treasury yields rising 66 basis points in 2024 to 4.57 per cent, reflecting expectations of pro-business policies, tax cuts and a market-friendly administration. Meanwhile, in China, 10-year bond yields fell 89 basis points across the same period to just 1.67 per cent as the economy continues to struggle with low growth and disinflation. This divergence has continued in the opening days of 2025, further highlighting the US exceptionalism of the times. Away from US markets, global growth looks tepid - no longer will a raising US tide lift all boats, meaning investors will need to place their bets selectively as asset performance across geographies will likely diverge significantly in similar asset markets. In 2025, the volume of corporate debt requiring refinancing is set to increase significantly. After locking in low rates during the Covid period, a significant proportion of loans and bonds now face repayment or rollover. This dynamic has the potential to add some spice to markets this year, as there will be some bad refinancing stories in the credit space after such a dramatic shift in the interest rate environment since the pandemic. Private credit issues already are emerging in Australia, with a number of high-profile private credit investment managers citing issues around the sector. However, the inherent lack of transparency within private credit means these challenges often remain hidden until the damage is done. In some cases, junior or subordinated lenders in local deals have already faced complete losses. As interest rates continue to exert pressure and delinquencies rise, we anticipate more such stories to surface, reflecting the sustained impact of a restrictive rate environment. Private credit is a highly attractive asset class but its rapid growth has attracted many new participants who promote high returns with minimal perceived risk (and low market volatility because of infrequent asset revaluation). This can be misleading, as high returns typically involve substantial risks that may not be immediately apparent. Investors require significant skill to identify who they are lending to, where they sit in the capital stack, who might run the workouts on distressed assets if required and how long this process may take. These products typically require long lockups of capital, which increasingly will need to ride through heightened uncertainty. Returns must be exceptionally high to compensate for these factors. The question is whether these challenges will escalate into a systemic tipping point, triggering broader market repercussions, or whether they will remain isolated incidents, wiping out the few unfortunate folks who didn't do their homework or ran the risk regardless. The answer will likely depend on the scale and interconnectedness of the issues as they unfold. The year looks set to be full of surprises. We expect the Reserve Bank will cut interest rates early in 2025, as inflation continues to moderate with a significant lag to the rest of the world, and we expect other jurisdictions will continue cutting rates as economies slow. Calibrating all of that with such significant policy uncertainty is difficult; investors will need to ride the developments and adjust accordingly. As always, we think portfolio diversification is prudent into such uncertainty, as bold bets will likely be as lucky as they are smart. Charlie Jamieson, Chief Investment Officer Funds operated by this manager: CC Jamieson Coote Bonds Active Bond Fund (Class A), CC Jamieson Coote Bonds Dynamic Alpha Fund, CC Jamieson Coote Bonds Global Bond Fund (Class A - Hedged) |

5 Dec 2024 - The Australian: Donald Trump 2.0 puts global markets on edge

|

The Australian: Donald Trump 2.0 puts global markets on edge JCB Jamieson Coote Bonds November 2024 Uncertainty will reign after the re-election of Donald Trump and the Republican Red sweep on Capitol Hill, giving the Grand Old Party (GOP) a clear mandate for significant change. After a campaign dominated by personal insults and grubby fearmongering, actual hard policy detail is somewhat scant. Initially, markets have responded by backing Trump and team GOP, with risk assets rallying, thrilled with an outlook of perceived positive growth policies centred around tax cuts, deregulation and less focus on environmental issues. However, markets must wait for more detail to truly release the animal spirits, as some touted Trump policies may threaten such growth outcomes by taking momentum out of the economy. Will the bark of Trumpian policy be equal to the bite, or does the "art of the deal" translate into vocal threats without the downside of chosen short-term pain? The US budgetary outlook will provide guardrails to these expectations. 2024 has been a year of toppling sitting governments, as voters remain angry in a post-Covid world with extreme cost-of-living pressures. Opposition parties the world over are being swept into power, only to find that governance in the aftermath of such an environment is quite difficult: it is far easier to criticise from the opposition benches than solve the complex problems in government. While the GOP has a clear voter mandate to lift living standards and restore low and stable inflation, some of the publicly suggested policy combinations threaten to deliver the opposite outcomes if enacted. Such moves could take the gloss off the initial market enthusiasm enjoyed since the election announcement. Trump has touted an across-the-board 10 per cent import tariff as a tool to drive change in trade policies, attempting to level the playing field by making US products more competitive against lower-cost producers, while also encouraging US-based investment. He has also targeted specific countries, such as China, proposing tariffs as high as 60 per cent. While this would help improve the US fiscal position by generating revenue from tariff taxes on imported goods, it effectively acts as a direct tax on American consumers, who would face higher prices on everyday items due to increased import costs. This would raise the general price level, stimulating inflation at a time when the Federal Reserve is lowering interest rates from emergency settings used to combat the last bout of Covid-induced inflation shocks. It would likely be very politically unpopular and, despite the sweeping mandate just received, the midterm elections of 2026 are always in the back of political minds. Trump has similarly proposed cutting up to $US2 trillion in deficit spending by appointing Elon Musk as a change agent to drive efficiency across federal government operations. While reducing waste is beneficial in the long term, the US economy is already reliant on significant government spending to bolster its somewhat slight growth profile―- all things considered―- given the already massive intervention of the government in the economy. The deficit spend is simply unprecedented for non-war times, running at 6-7 per cent of GDP under the Biden administration. Such massive government spending is only generating a tepid 2.8 per cent GDP growth, all while the economy experiences significant positive tailwinds from immigration. Removing such a large amount of spending from the economy would have significant growth implications if not replaced by other positive accretive outcomes such as a productivity enhancement. In these delicate political times, choosing such a deacceleration of economic activity seems an unlikely political choice. Delicate choices and policy combinations need to be made by the Trump administration as tax cuts and spending for growth require financing inside a US budget set up that is already strained after large Covid spending programs. Bond markets are on watch around the sustainability of the US fiscal position, now exceeding $US35 trillion and climbing (120 per cent of GDP), amid concerns that the budget has little room to provide a counter-cyclical buffer should the economy experience any type of recessionary outcomes. Since the election, yields have stabilised, supported by ongoing interest rate cuts from central banks such as Sweden's Riksbank, the Bank of England, and the Federal Reserve. Markets remain cautious, noting the potential risks of politically driven policies that lack economic foresight - highlighted by the swift removal of British Prime Minister Liz Truss after bond markets reacted sharply to her fiscal plans. Until US policy plans are laid out in full, we maintain a preference for Australian and European fixed income assets, which offer stronger fiscal conservatism and higher credit quality. Overall, this environment underscores the importance of diversification, careful monitoring of fiscal policy announcements, and considering exposure to regions with more stable economic policies. Funds operated by this manager: CC Jamieson Coote Bonds Active Bond Fund (Class A), CC Jamieson Coote Bonds Dynamic Alpha Fund, CC Jamieson Coote Bonds Global Bond Fund (Class A - Hedged) |

11 Oct 2024 - Are high grade bonds a natural choice for strengthening your fixed income allocation

|

Are high grade bonds a natural choice for strengthening your fixed income allocation JCB Jamieson Coote Bonds September 2024 In a rapidly evolving macroeconomic landscape, Australian investors are increasingly turning to global high grade government bonds as a highly defensive component of their investment portfolios. This move is predominately driven by global government bond markets offering greater portfolio diversity, enhanced return potential and broad sources of yield. In this article, we unpack the key themes influencing investors' long-term views on the value of including global high-grade bonds into a fixed income portfolio. Where are we now in the cycle?The key question facing investors today is: Where are we in the current business cycle, and when will the next shift occur? A glance at the economic growth of the world's major economies and stock markets over the past decade reveals that we've been in an extended expansionary phase. However, determining exactly when the cycle will peak is notoriously difficult. While certain indicators have pointed to an approaching recession, accurately predicting this shift remains a challenge. At a time where geopolitical tensions are intensifying and policy makers are grappling with softening global growth and persistent inflation, investors face a landscape of heightened uncertainty on many fronts. Global central banks are embarking on a synchronized interest rate cutting cycle as the narrative has switched this year from inflation concerns to growth concerns. Global inflation has moderated from its peak levels, with current annual rates of inflation at 2.50% in the US (the lowest since February 2021), 2.00% in Canada, 2.20% in the UK, 2.20% in EU and 3.8% in Australia, although forecasted to fall to 2.70%. Meanwhile economic growth has started to show some cracks, which until now has been supported by government spending. Employment remains a key determinant in the direction of growth and recent signs from the US indicate that this is turning. US employment data was recently sharply revised lower - which has triggered anxiety amongst central bankers. In response, they are eager to get on the front foot and curb labour market weakness before it deteriorates sharply. Savings are already getting depleted, and signs of rising delinquency are cautionary tales that will be exacerbated from job losses. Asset allocations can be dynamically adjusted to optimise performance during different phases of the cycle. With the recent loss of US employment momentum, are we moving from Slowdown to Recession? If so, improving asset quality and liquidity will be important to navigate the coming market environment. Chart 1: Phases in the business cycle.The economic cycle consists of four key phases: Boom, Slowdown, Recession and Recovery, which then leads back to another Boom - continuing the cycle.

Expanding horizons: Unlocking enhanced alpha opportunities that may awaitNot all bonds are created equal. High quality sovereign global bonds offer a lower risk profile due to their stability and creditworthiness. These bonds are typically issued by governments with strong financial standing, making them less susceptible to default and economic fluctuations compared to lower-rated or corporate bonds. As a result, they can serve as a safer option for investors seeking to mitigate risk within their portfolios. Global high grade bonds currently present unique alpha opportunities for investors.

Chart 2: Global Government Bonds Have Outperformed International Equities During Major Sell-OffsGlobal government bonds are among the safest investments in an investor's portfolio, offering capital preservation and helping to reduce equity volatility due to their long-term negative correlation with stocks. They also provide stability to portfolios, especially during market downturns. We can observe how global sovereign bonds perform during periods of financial market crises and significant events in the chart below. During the dot-com crash, the global financial crisis and European debt crisis, global government bonds outperformed equities providing capital preservation and a hedge against the equity market collapse. During the COVID-19 pandemic, global sovereign bonds and equities once again exhibited contrasting performances, although the dynamics were more complex than during previous crises. The pandemic caused a sharp, short-term market shock in early 2020, followed by an unprecedented recovery, largely driven by aggressive fiscal and monetary stimulus.

Source: JCB team analysis based on data from Bloomberg. How should investors position fixed income portfolios as global rate cuts begin?When considering the long-term value of fixed income, high grade bonds stand out as one of the safest investments in an investor's portfolio. Not only do they preserve capital but also help reduce equity volatility due to their long-term negative correlation with stocks, ultimately stabilising portfolios during tough market conditions. We believe that now could be an ideal time to lock in elevated income levels and broaden fixed income portfolios to include a variety of global bonds. The onset of the cutting cycle is likely to lead to a decrease in bank deposit rates, making government bonds a more attractive option for investors seeking capital appreciation. As a significant amount of dollars currently parked in money market funds is expected to flow into the government bond sector, this shift is further supported by the frothy nature of the private credit market, which has more than doubled in size since 2019. Interest rate cuts mean private credit's floating rate is less attractive, redirecting capital away from it into higher interest bearing assets. The transparency and liquidity of government bond funds provide a compelling argument for this reallocation. Adapting to market changes: why global sovereign bonds matter nowFalling interest rates signal a shifting investment landscape, presenting new opportunities for asset allocators. Rate cutting cycles underscore the importance of diversification, especially as economic conditions can change rapidly. Funds operated by this manager: CC Jamieson Coote Bonds Active Bond Fund (Class A), CC Jamieson Coote Bonds Dynamic Alpha Fund, CC Jamieson Coote Bonds Global Bond Fund (Class A - Hedged) |

11 Mar 2021 - How will the recovery influence returns?

|

How will the recovery influence risk and returns? Mark Burgess, Chairman of the Advisory Board at Jamieson Coote Bonds As the macro risks associated with COVID-19 have loomed over global markets and economies for almost a year now, changing expectations of the shape and strength of the recovery will be important in influencing returns and volatility for 2021. We recently sat down with Mark Burgess, Chairman of the Advisory Board at Jamieson Coote Bonds to discuss this and other important issues on investors' minds. Navigating the economic recovery This recovery is unique as we've seen one of the most dramatic interventions in markets in history, to the credit of central banks and governments who took immediate action last year and we are now beginning the see the consequences of that. Will it take traction in the economy? How will the virus develop? These are critical issues which are raising serious question marks about the style and nature of the recovery. Financial markets are looking through this - at some of the beneficial aspects of low rates and at the rising liquidity aspect of central bank intervention. The economic environment is rather unclear, relative to financial markets, which are taking a forward looking view. Inflation risks on the rise I'm always reminded of what I believe is the right approach to risk and look to a range of scenarios, such as economic growth. Inflation should be one of those scenarios. How does inflation play out? Is it a rising risk? We're likely to get an uptick in inflation as the year-on-year comparisons turn positive. There are a couple of factors that have helped keep inflation low in the past, such as globalisation, that appear to be changing and therefore the ability to keep inflation at low levels is changing at the margin. On the flip side, we have very slack labour markets, we have an output gap that's quite wide, and at these low interest rates, capacity can be added quite quickly across the world. With this in mind, my expectation is that perhaps inflation will uptick but we're unlikely to get the kind of embedded or serious inflation that we saw say in the 1970s. Competition caused by excess investment as a result of low interest rates could cause deflation in parts of an investor's portfolio, and the inflation-deflation combination should be assessed across the assets that go into a well-diversified portfolio. Watch the video to hear more. Constructing fixed income allocations - the risk of chasing yield Yields are going to be low generally and the most important risk is not to chase yield for yield sake. If you're chasing yield with risk attached to it, those risks will be lurking in the background more over the next two to three years than they have in the past. As bond yields are marginally moving back up, they're getting ready to be a defensive asset again. Markets are experiencing this combination where yield is becoming available in some places and in other places there's certainly a lot of competition for yield. Investors should be cautious as risk attached to yield is one of the most important things to watch out for. We've long advocated this; one example is separating corporate credit from high grade sovereign bonds. High grade government bonds provide safety, while corporate credit will have other risk and return characteristics. Most importantly, as we come out of the COVID-19 environment, we'll find out which corporates are safe and which are in good shape as we see that part of the cycle play out. "The most important risk is not to chase yield for yield sake." The important role of high grade government bonds in diversifying some of the unknown risks that remain High grade government bonds were defensive during the downturn, playing the important diversifying role that they have always played in portfolios. As government bonds edge slightly higher again, they will provide that defensive characteristic and diversification within a portfolio. We believe they will always be a good asset to hold. Australian investors haven't held a large position in government bonds historically, and a key lesson from the events of last year proved the diversification characteristics of the asset, at a time where diversification was difficult to find. There are a couple of other places to find diversification, but high grade government bonds are certainly one component of that. Watch the video to hear more.

|

18 Feb 2021 - January 2021 High Grade Bonds Performance and Market Update

|

Charlie Jamieson, Chief Investment Officer at Jamieson Coote Bonds, discusses the market and performance of high grade bonds in January 2021. |

Online Applicatons

Free, simple and secure

Olivia123 - the fast simple and secure online alternative to completing paper based application forms.