Join L1 Capital International's CIO, David Steinthal, for an update on the investment environment, positioning of the L1 Capital International Fund (Managed Fund) and key takeaways from the recent results season.

No events currently listed.

Find a Fund

Peer Group Analysis View All»

| Index Selector Links | 1 Year | 3 Year | 5 Year |

|---|---|---|---|

6.25% |

6.45% |

6.75% |

|

72.07% |

20.63% |

46.11% |

|

7.83% |

-0.77% |

3.41% |

|

9.25% |

4.85% |

7.36% |

|

11.60% |

5.73% |

8.62% |

|

9.17% |

0.32% |

5.66% |

|

10.17% |

5.40% |

7.84% |

|

14.78% |

4.38% |

9.98% |

|

11.36% |

-0.27% |

8.00% |

|

12.32% |

1.12% |

8.42% |

|

5.28% |

0.55% |

1.44% |

|

8.47% |

3.08% |

3.97% |

|

8.91% |

6.41% |

6.04% |

|

9.28% |

6.39% |

6.03% |

|

0.06% |

5.43% |

4.01% |

|

7.37% |

3.38% |

6.06% |

|

-9.49% |

-3.44% |

0.69% |

Hedge Clippings

12 Jul 2024 - Hedge Clippings |12 July 2024

|

|

|

|

Hedge Clippings | 12 July 2024 If there was one topic aside from inflation and interest rates that was set to dominate the news in 2024, it was going to be elections - or more importantly their outcome. 64 countries, plus the European Union, have held, or are due to hold elections this year, representing 49% of the world's population. You would expect therefore to say "Democracy Rules" - except it doesn't always apply. The potential for change in Russia (even though elections were held) was limited to say the least, as it was in Bangladesh, or Pakistan, where the most popular politician, Imran Khan, was in jail. Last week's UK election is another case in point: Democracy, of a sort, took place with an overwhelming vote of no confidence in the ruling Conservative government, although only 59% of the population thought it was worth the effort to vote on the day. Presumably a fair proportion of the 41% who didn't vote were still following the UK's WWll era slogan "Keep Calm and Carry On". Meanwhile, a fair proportion of the 61% who did vote will have to do the same for the next 4 years. However, the result was lopsided. While the winning Labour Party control 412 or 63% out of the total of 650 House of Commons seats, they received only 34% of the overall vote. Much of the skew can be blamed on the UK's system of first past the post voting - although if blame is to really be apportioned, Rishi Sunak and his 4 predecessors in 10 Downing Street should really shoulder it. This system saw 12.2% of the vote cast for the Liberal Democrats, who won 72 seats, while arch-spoiler Nigel Farage's Reform UK party out-polled the Lib Dems with 14.5% of the vote, but only won a paltry 5 seats for their efforts. As above, Democracy of a sort, but we have to admit better than that available - or not, depending on your view - in Putin's Russia, or for that matter Xi's China, where he was unanimously elected by almost 3,000 delegates of the National People's Congress last year. Australia's political system may not be perfect, but proportional representation, thanks to our preferential system, sure beats the heck out of the UK, let alone China and Russia! Which leads us to the looming election in the US, where earlier today Joe Biden was mumbling and bumbling his way through an hour-long news conference following the end of the NATO Summit commemorating its 75 years' existence (six years short of Joe's own age). In between slips of the tongue (mixing Putin with Zelensky, and for a moment naming Trump as his Vice President) Biden sounded more like he was at an election rally than a summary of the NATO deliberations. Meanwhile Trump, thanks to the US Supreme Court's ruling on presidential immunity, was busy filing an appeal against his conviction on criminal charges stemming from hush money paid to a porn star. Unless Biden has a change of heart, which it seems he's unwilling to do, one of them will end up as President of the free world come November. Whichever side of politics you're on in Australia, thank your lucky stars you're here! News & Insights Down-trading Megatrend | Insync Fund Managers Why invest in global equities | Magellan Asset Management June 2024 Performance News Bennelong Australian Equities Fund Glenmore Australian Equities Fund Bennelong Long Short Equity Fund |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |

15 Jul 2024 - Performance Report: Delft Partners Global High Conviction Strategy

[Current Manager Report if available]

15 Jul 2024 - 10k Words | July 2024

|

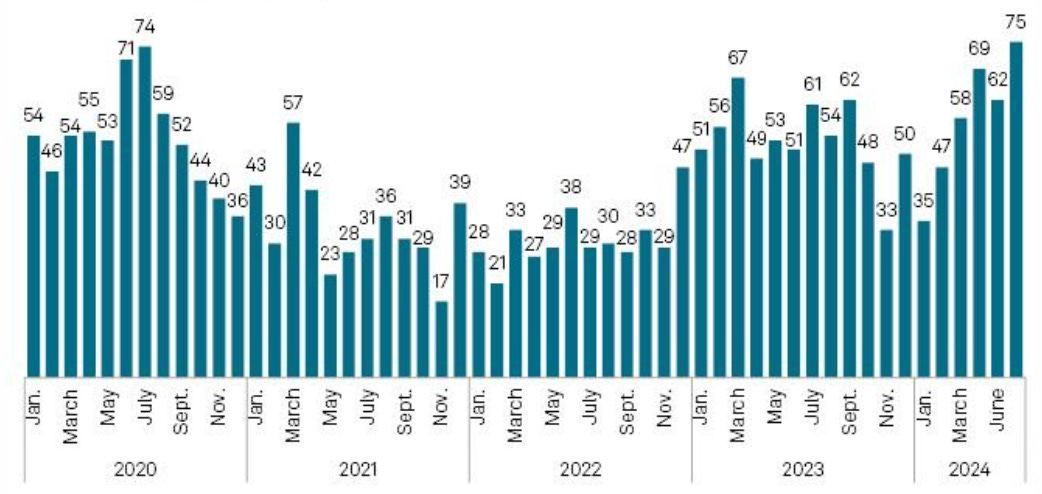

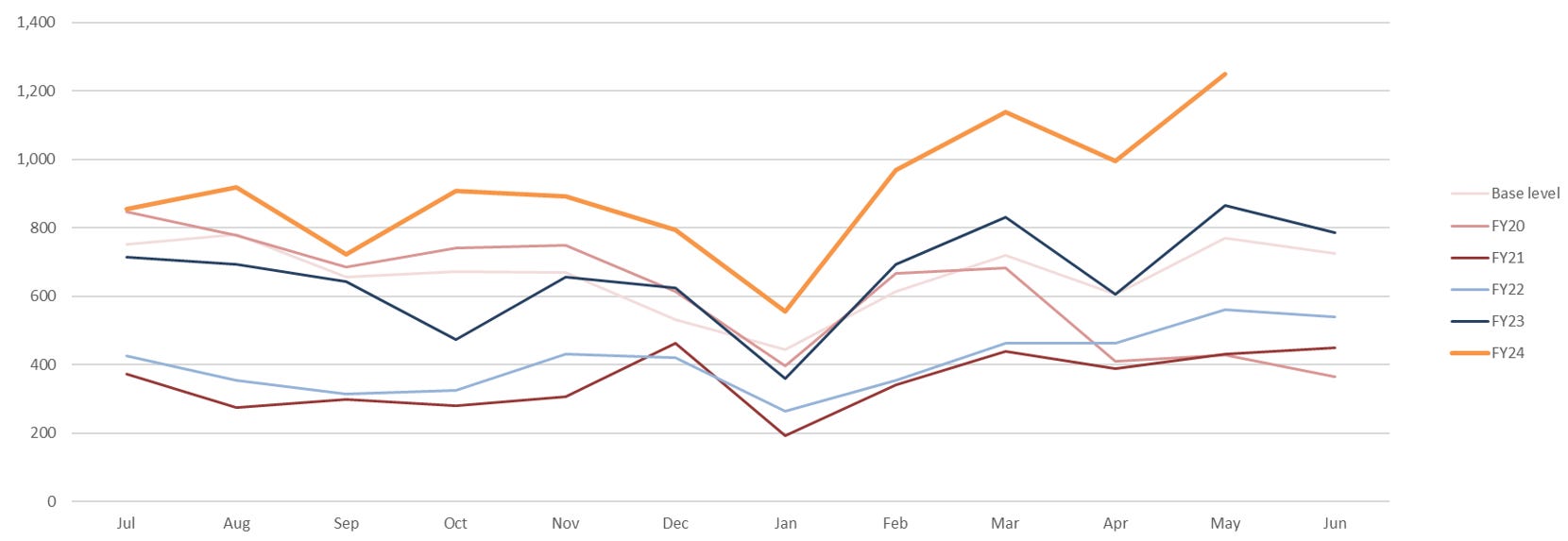

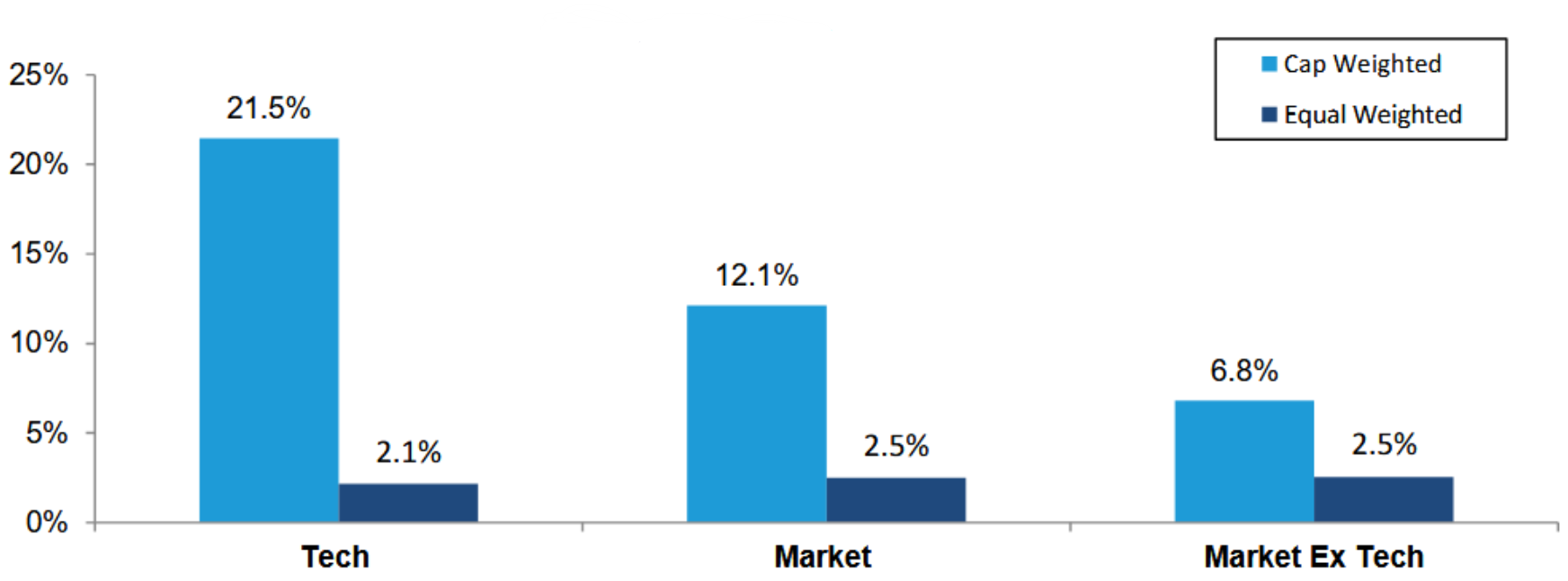

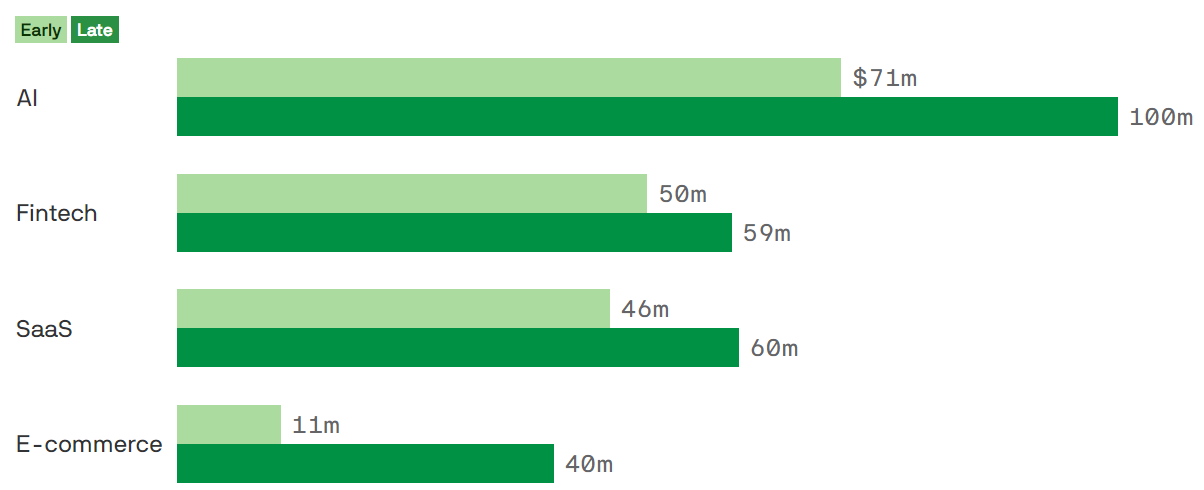

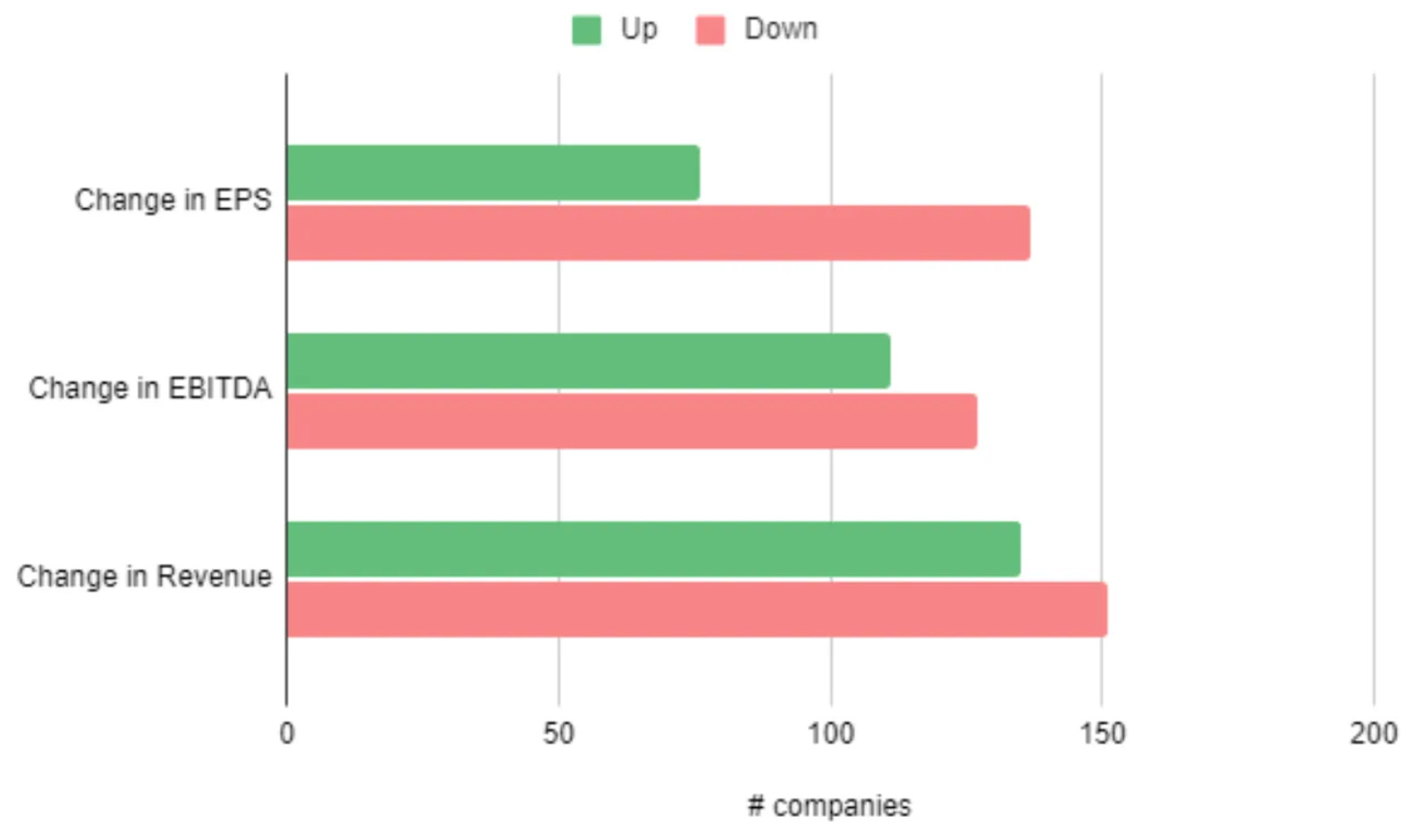

10k Words Equitable Investors July 2024 Seek's national job ads count is down 17% over 12 months; corporate bamkruptcy/administration filings at multi-year highs; equal-weighted tech stocks are lagging cap-weighted tech performance by even more than the broader US market; AI valuations holding up VC space too; sustained net short positon on S&P 500; ASX nano/micro caps and the seasonal performance driven by tax loss selling in June, with a rebound in July; and finally the volume of downgrades coming into ASX reporting season is in-line with prior years. Seek's June 2024 Australian job ads

Source: Seek US bankruptcies by month

Source: S&P Australian external administration appointments by year

Source: ASIC 2024 YTD absolute performance - tech v. rest of the market

Source: Bernstein via @modestproposal1 2024 VC-backed tech valuations of select verticals, by stage

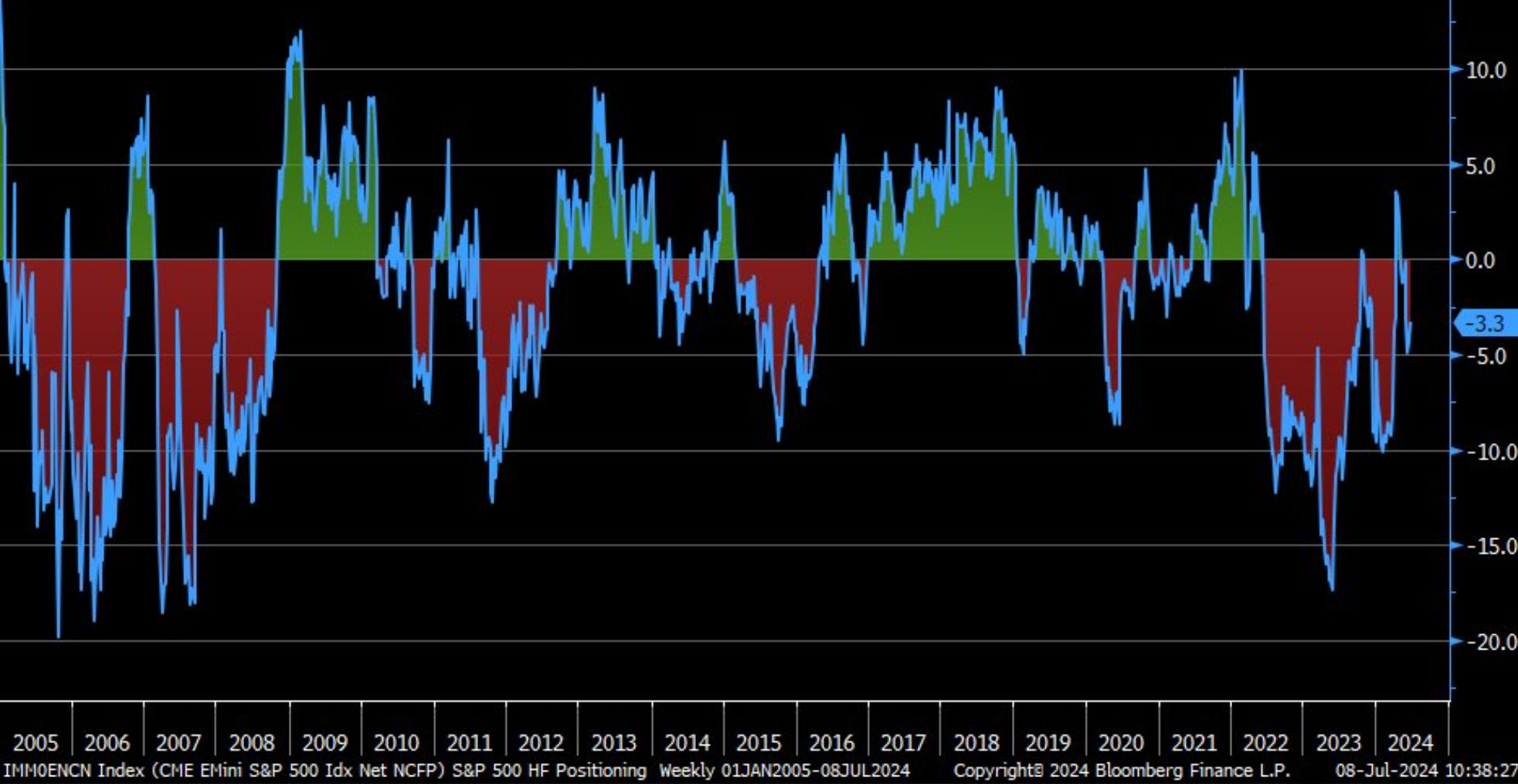

Source: Axios E-Mini S&P 500 net non-commercial futures positions % of open interest

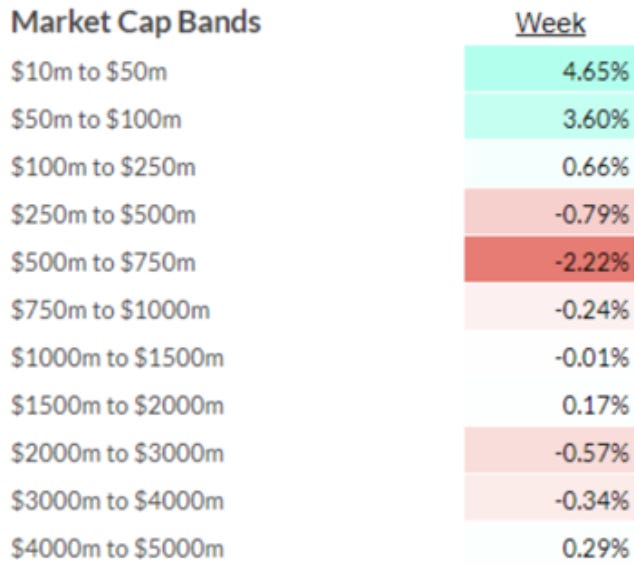

Source: @LizAnnSonders, Bloomberg ASX ex-resoures by market cap band over 12 months of CY2024

Source: Equitable Investors

ASX ex-resoures by market cap band - first week of FY2025

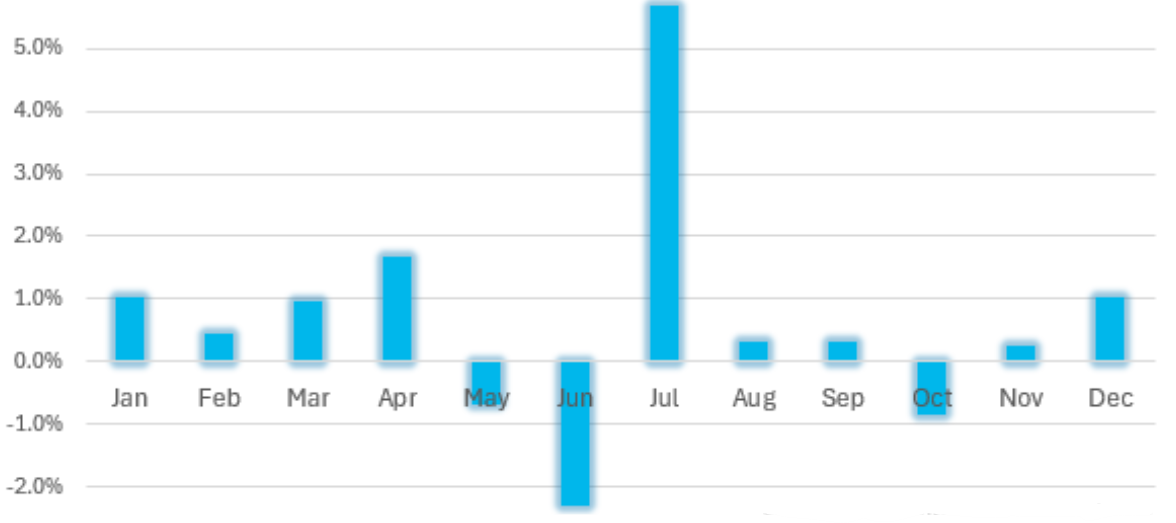

Source: Equitable Investors Average monthly return of S&P/ASX Emerging Companies Index (since March 2016, excluding COVID-impacted CY2020)

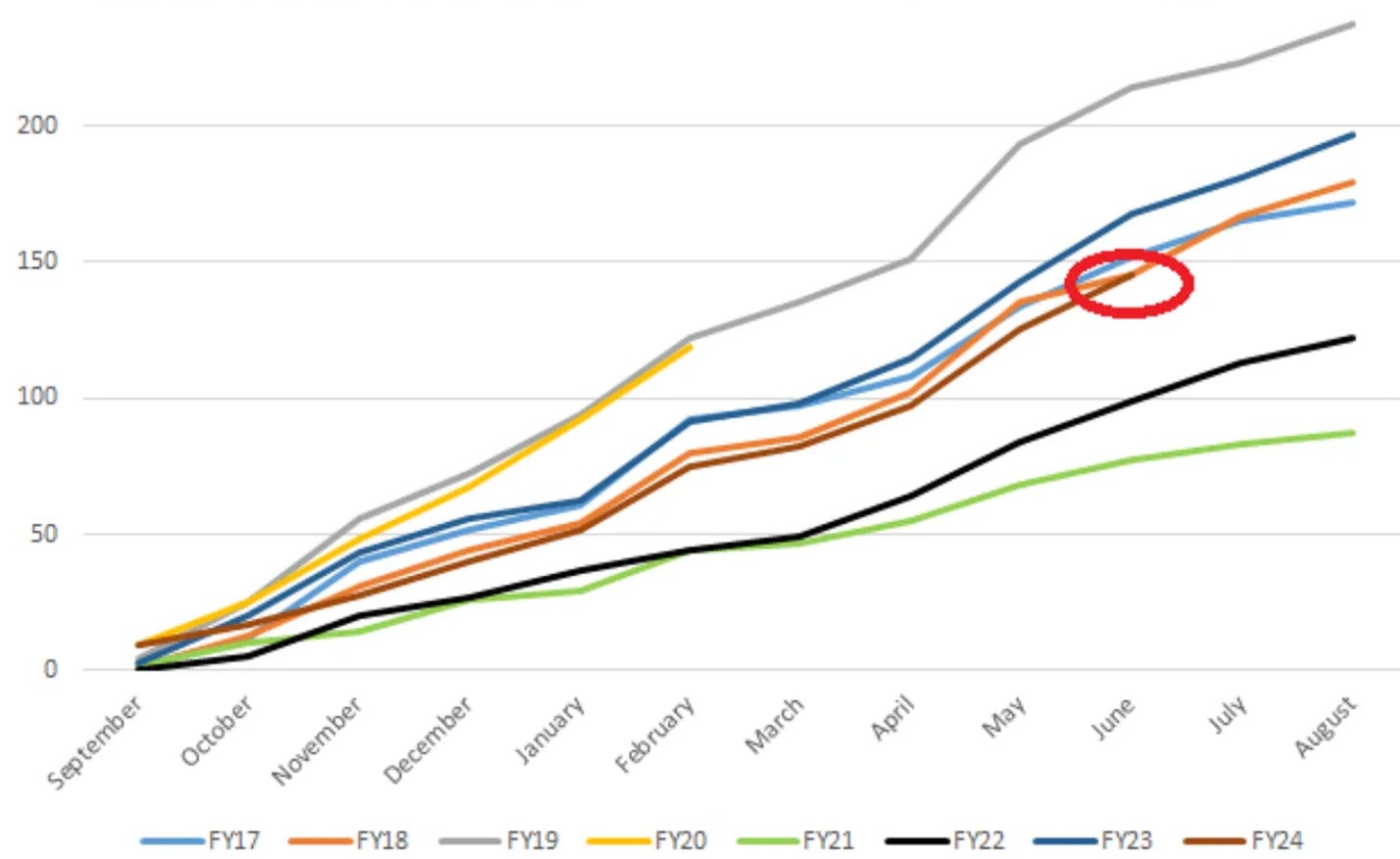

Source: Equitable Investors Number of ASX downgrades - comparison with past financial years (FY20 cut short by COVID)

"FIT" universe (ASX micro-to-mid, ex resources) - changes to consensus estimates over past 12 months

Source: Equitable Investors July 2024 Edition Funds operated by this manager: Equitable Investors Dragonfly Fund Disclaimer Past performance is not a reliable indicator of future performance. Fund returns are quoted net of all fees, expenses and accrued performance fees. Delivery of this report to a recipient should not be relied on as a representation that there has been no change since the preparation date in the affairs or financial condition of the Fund or the Trustee; or that the information contained in this report remains accurate or complete at any time after the preparation date. Equitable Investors Pty Ltd (EI) does not guarantee or make any representation or warranty as to the accuracy or completeness of the information in this report. To the extent permitted by law, EI disclaims all liability that may otherwise arise due to any information in this report being inaccurate or information being omitted. This report does not take into account the particular investment objectives, financial situation and needs of potential investors. Before making a decision to invest in the Fund the recipient should obtain professional advice. This report does not purport to contain all the information that the recipient may require to evaluate a possible investment in the Fund. The recipient should conduct their own independent analysis of the Fund and refer to the current Information Memorandum, which is available from EI. |

12 Jul 2024 - Performance Report: Cyan C3G Fund

[Current Manager Report if available]

12 Jul 2024 - Performance Report: Argonaut Natural Resources Fund

[Current Manager Report if available]

12 Jul 2024 - Performance Report: Bennelong Long Short Equity Fund

[Current Manager Report if available]

12 Jul 2024 - Fast food profits

|

Fast food profits Montgomery Investment Management June 2024 I have previously written here that one of the most repeatable ways to make money on the Australian Stock Exchange (ASX) is to buy into a retail store rollout story early. Catching the steepest part of the 'S' curve when revenue and profit growth are accelerating while head office becomes simultaneously more efficient usually produces good results thanks to the accompanying rise in the share price. And when like-for-like sales of existing stores are still growing and the number of new stores being added is high in proportion to the number of existing stores, jumping aboard early provides an even more beneficial tailwind. Store growth ambitions are often disclosed in a company's initial public offering (IPO) prospectus and within twelve months, investors usually have a good idea about management's ability to deliver on the stated plans, as well as customers' love for the concept. Recent retail success stories Some recent and not-so-recent examples include Lovisa (ASX:LOV), which sold its product through 60 stores in 2012. When it was listed in 2014, it had grown to 220 stores. Eight years after listing, Lovisa distributes its jewellery through 449 stores. And since it listed, the share price is 976 per cent higher. JB Hi-Fi (ASX:JBH) listed in October 2003, with just 25 stores, issuing shares at $1.55. Today, with 316 stores (including acquisitions of Clive Anthonys and The Good Guys) the shares trade at $58.46, a return of 3671 per cent, or 19.1 per cent per annum over 20 years, excluding dividends. The furniture retailer Nick Scali (ASX:NCK) was listed in May 2004. At the time of its 2004 full-year results, it reported sales of $43.4 million and earnings of $6.7 million from just 10 stores. The IPO price was $1. With 85 stores today, and more than 90 Plush stores, the share price is up 1378 per cent at $13.78, or 14 per cent per year over 20 years. Guzman y gomez IPO Recently, the healthy, fast, Mexican-inspired food chain Guzman y Gomez launched its prospectus for an already fully subscribed IPO to list shares on the ASX on 25 June. With its first store opening in 2006, and 185 stores in Australia currently, Guzman y Gomez's management has already proven to be one of Australia's fastest-growing quick service restaurant (QSR) teams. Guzman y Gomez plans to have over a thousand domestic stores in the next twenty years. This compares with McDonalds (NYSE:MCD) Australia, which opened its first store in 1971, reached 869 stores in 2011 and now has 1043 stores. Elsewhere, Subway, which launched in 1988, has 1227 stores across Australia today, while Domino's (ASX:DMP), which set up shop in 1983, now has 736 stores. And like Lovisa, JB Hi-Fi and Nick Scali before it, Guzman y Gomez lists 'new store openings' as its top source of future growth, stating, "new restaurant openings in Australia are expected to be the primary contributor to Guzman y Gomez's network sales growth over the long term. Guzman y Gomez believes there is an opportunity to grow its network to more than 1,000 restaurants in Australia over the next 20-plus years. The company believes that it has substantially built the team, restaurant pipeline, and infrastructure to be able to open 30 new restaurants per annum over the near-term [it opened 26 in CY23], increasing to 40 restaurants per annum within five years." As an aside, there are also 16 stores in Singapore, five in Japan and four in the U.S. Not only are store openings going to continue, they are expected to accelerate. That's the first source of growth. Importantly, individual store economics are extremely attractive, with Guzman y Gomez expecting to achieve a return on investment (ROI) in line with existing stores of approximately 50-55 per cent on new corporate restaurants and its franchisees to achieve an ROI of approximately 30 per cent on new franchise restaurants, with the difference being due to the royalty paid by franchisees. Not only is the number of these highly profitable stores expected to grow significantly and accelerate, but restaurant margins are also expected to improve. Guzman y Gomez restaurant margins improve with volume, and volume rises as Guzman y Gomez stores mature. In 2023, corporate restaurant margins were 14.4 per cent. In 2024, that margin is expected to rise to 17.1 per cent and 17.8 per cent in 2025. At the same time, the Franchise royalty rate is expected to rise from an average 7.6 per cent in FY23 to 8.3 per cent in 2025. And as the store count grows, the general and admin related costs should come down. Indeed, the company is aiming for a reduction in G&A-to-network-sales from the expected 6.8 per cent of sales in FY25. Accelerating store openings, continuing like-for-like sales growth, expansion in restaurant margins and franchise royalty rates should all add up to strong earnings growth, something investors are desperately seeking in an environment marred by slowing economic growth and heightened interest rates. What remains for investors to consider is the price they might be paying for all this growth. Cornerstone investors, which include Aware Super and Copper Investors, are acquiring their shares at $22 each following a 250-for-one share split. That price represents a very high price-earnings (P/E), so one might wonder what the cornerstone investors see that's worth paying up for, especially given at that multiple there will be any number of investors who turn their back on the opportunity. So is Guzman y Gomez the ultimate investor Mexican standoff? Valuation considerations Most investors value QSR businesses on an earnings before interest, tax, depreciation and amortisation (EBITDA) multiple basis, and the number on the prospectus is about 38 times, which, again, is very high. Importantly, it's worth understanding that 38 times includes the losses the company is currently incurring in the U.S. strip out those losses and the multiple applicable to the Australian business is about 32 times. It's also worth acknowledging a change in the terms between the company and its franchisees. When Guzman y Gomez first launched, the standard franchise contract included an eight per cent of sales royalty. Given Guzman y Gomez franchisees earn abnormally high returns on investment, Guzman y Gomez changed that franchise royalty to eight per cent of sales up to three million dollars per store and 15 per cent above that. All new franchise arrangements are struck on the new terms and old franchise arrangements, when they come up for renewal, will move to the new platform. Assuming Guzman y Gomez didn't open another restaurant ever again and existing stores traded without any further improvement, the shift to the new contract terms would see the EBITDA multiple falls from 32 to approximately 28 times. Meanwhile, if the company also opens its targeted 30 stores next year, never opens another store again after 2025, and these stores trade in line with existing stores, the EBITDA multiple falls to 23 times. It is clear from the prospectus, the company plans to open many more stores in coming years. International comparisons Despite Guzman y Gomez's prospectus appearing to play down its international growth opportunities, it may nevertheless be worth comparing the adjusted EBITDA multiple to global peers. A relevant comparison would be Cava (NYSE:CAVA), which IPO'd in the U.S. in June 2023, also at U.S.$22 per share, funnily enough. Upon listing, Cava shares surged 89 per cent to U.S.$42 amid that clearly welcomed long-term sustainable growth stories, especially category-defining brands. Cava has about 200 stores and trades at 82 times EBITDA. Meanwhile, Chipotle (NYSE:CMG), which is obviously the behemoth in the space, and arguably mature, with 6,000 stores, trades at 34 times. With an already proven store concept, a significant store rollout opportunity ahead, and a proven management team to execute that store rollout, some investors are clearly arguing the multiple is reasonable. And with existing shareholders (including your author) escrowed until August 2025, the supply of shares may be tight. Investing in the rapid rollout of a successful store concept has been one of the easiest and most repeatable ways to make money in the Australian stock market. The listing of Guzman y Gomez in June this year will help determine if that strategy remains relevant. Author: Roger Montgomery Funds operated by this manager: Montgomery (Private) Fund, Montgomery Small Companies Fund, The Montgomery Fund |

11 Jul 2024 - Performance Report: Glenmore Australian Equities Fund

[Current Manager Report if available]

11 Jul 2024 - Performance Report: Bennelong Australian Equities Fund

[Current Manager Report if available]

11 Jul 2024 - EMD outlook: election fever

|

EMD outlook: election fever abrdn June 2024 We look forward to the numerous elections that have the potential to shape the asset class and what it could mean for investors.There is rarely a dull moment in emerging market debt (EMD), and the first six months of 2024 have been no different. While the opening half of the year hasn't produced the blockbuster returns of 2023, there have been plenty of talking points. Most notably around elections and debt restructurings. Bond outlook pieces often mention developed market monetary policy as a driver of returns, and rightly so. For emerging markets (EMs) in 2024, however, a different theme has emerged- elections. To date, voters have gone to the polls in Bangladesh, Taiwan, El Salvador, Pakistan, Senegal, India, Mexico, Turkey and South Africa. We don't have time to run through the individual country outcomes but there are a few that warrant a closer look. Let's turn our attention to Pakistan. In January, a civilian government came to power, pledging fiscal consolidation and promising to build foreign exchange (FX) reserves. Sound familiar? That's because it is. Pakistan is now looking to enter a record 24th International Monetary Fund (IMF) programme. The question remains: will the outcome be different this time? The early signs are promising. Ongoing disinflation has allowed the central bank to loosen monetary policy. The balance of payments recently turned positive. But let's not get carried away. This story is still unfolding, and we'll keep a close eye on developments over the coming months. In Mexico, the election of Claudia Sheinbaum, a protégé of the current president (AMLO), is expected to maintain the political status quo. Sheinbaum will need to focus on reducing the deficit from 6% of gross domestic product to a manageable level. The fiscal deficit blew out in the run-up to the election, as AMLO increased unfunded social security payments - among other social transfers - in a bid to shore up support. It certainly did the trick. Sheinbaum will also have to reckon with Pemex, the state-owned energy company groaning under heavy debt and declining crude production. AMLO's decision to include Pemex's amortisation payments in the national budget for the first time also increased the deficit. It's hard to see how Sheinbaum will address these issues in the near future. Democracy alive and wellLiberal democracy has come under pressure over the last few years. It was therefore encouraging to see the world's largest democracy, India, go to the polls in a general election that was generally seen as free and fair. Such is the scale of proceedings that voting took place over six weeks. President Modi has walked away wounded but victorious. His BJP party remains the largest in congress and coalition partners are unlikely to block his planned economic initiatives. Finally, in South Africa, the loss of the ANC's majority for the first time since the dawn of democracy shocked the party. For the moment, things are likely to remain the same. Yet, looking ahead, there's an increased chance of the government collapsing, leading to either parliament choosing a new president or calling for new elections. Stay tuned. What does this mean for investors?Why are we focusing on country-specific events? Because it's in idiosyncratic stories where we see the most compelling investment opportunities. This plays to our strength in EMD: fundamental bottom-up research to generate alpha. At an index level, spreads across bond markets, including EMD, are tight compared with historic levels. Meanwhile, investment-grade spreads have been unattractive for several quarters. We remain underweight here. Over a year ago, we identified value in the distressed and CCC segments. The near completion of several debt restructurings has validated this view, leading to outperformance. Recently, investors accepted Zambia's debt restructuring deal, crafted by official creditors, the IMF and the private sector. These deals should lead to renewed inflows into Zambia and bodes well for Ghana and Sri Lanka, which are negotiating their own deals. While we haven't seen credit-rating upgrades for CCC-rated issuers - where the most significant spread changes have occurred - further narrowing of spreads is likely should such upgrades occur. What's the outlook?And so to the US Federal Reserve. Its decision to delay rate cuts has notably affected EM local bond markets, which are particularly sensitive to shifts in interest rate cut expectations. At the end of May, the EM Index was down -2.7% year-to-date. Despite the current challenges, rate cuts in EMs are coming. Monetary policy remains tight, growth is lagging long-term averages, and base effects mean inflation should continue to fall. Despite the macro backdrop, local bond markets continue to price-in tight monetary policy. We're holding positions and adding selectively in anticipation of the market delivering elevated returns in the coming months. After lagging EMs in 2023, EM Corporate Debt has outperformed in the first half of the year. Fundamentals remain in good shape, reflected in the low default rate year-to-date. At the end of April, the rate stood at just 0.7%, well-below the historical average. Most defaults in this asset class are coming from China's high-yield property sector. Like the sovereign market, spreads have been tightening recently, reaching near-historic lows. Despite this, the high absolute yield of over 7% remains appealing. For now, there seems to be little that could halt the momentum of the spread rally. Finally, a quick word on frontier local markets. What's changing? The answer is: a lot - and for the better. Policymakers are building external buffers, inflows into the local market are contributing to the rebuilding of FX reserves, and financing from commercial and official sources is on the rise. Meanwhile, fiscal consolidation and tightening monetary policy are helping to establish policy anchors. Finally, high nominal yields and attractive carry in countries like Pakistan, Nigeria, Kenya, and Egypt mean that these markets are garnering investor attention and are worth considering for investment. Author: Leo Morawiecki |

|

Funds operated by this manager: Aberdeen Standard Actively Hedged International Equities Fund, Aberdeen Standard Asian Opportunities Fund, Aberdeen Standard Australian Small Companies Fund, Aberdeen Standard Emerging Opportunities Fund, Aberdeen Standard Ex-20 Australian Equities Fund (Class A), Aberdeen Standard Focused Sustainable Australian Equity Fund, Aberdeen Standard Fully Hedged International Equities Fund, Aberdeen Standard Global Absolute Return Strategies Fund, Aberdeen Standard Global Corporate Bond Fund, Aberdeen Standard International Equity Fund, Aberdeen Standard Multi Asset Real Return Fund, Aberdeen Standard Multi-Asset Income Fund |

10 Jul 2024 - Performance Report: DS Capital Growth Fund

[Current Manager Report if available]

30 Oct 2023 - Global Quarterly Update

|

Global Quarterly Update Magellan Asset Management October 2023 |

|

Arvid Streimann discusses recent market volatility and the risks to watch out for, while Nikki Thomas shares her observations from her recent US trip and updates us on how the portfolio is positioned for the evolving investment landscape. (Viewing time: 15 mins) |

|

Funds operated by this manager: Magellan Global Fund (Hedged), Magellan Global Fund (Open Class Units) ASX:MGOC, Magellan High Conviction Fund, Magellan Infrastructure Fund, Magellan Infrastructure Fund (Unhedged), MFG Core Infrastructure Fund Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 ('Magellan') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to a Magellan financial product may be obtained by calling +61 2 9235 4888 or by visiting www.magellangroup.com.au. Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of a Magellan financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. Magellan makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Magellan. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Magellan will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material. Any third party trademarks contained herein are the property of their respective owners and Magellan claims no ownership in, nor any affiliation with, such trademarks. Any third party trademarks that appear in this material are used for information purposes and only to identify the company names or brands of their respective owners. No affiliation, sponsorship or endorsement should be inferred from the use of these trademarks. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan. |

11 Oct 2023 - Who will benefit from the energy transition?

|

Who will benefit from the energy transition? Magellan Asset Management September 2023 |

|

Net Zero is not a new ambition for governments and companies, with some sectors like utilities focused on this climate risk for quite some time now. David Costello, CFA, Portfolio Manager - Energy Transition Strategy discusses the opportunities we see from the energy transition and companies that may benefit from this transition. |

|

Funds operated by this manager: Magellan Global Fund (Hedged), Magellan Global Fund (Open Class Units) ASX:MGOC, Magellan High Conviction Fund, Magellan Infrastructure Fund, Magellan Infrastructure Fund (Unhedged), MFG Core Infrastructure Fund Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 ('Magellan') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to a Magellan financial product may be obtained by calling +61 2 9235 4888 or by visiting www.magellangroup.com.au. Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of a Magellan financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. Magellan makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Magellan. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Magellan will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material. Any third party trademarks contained herein are the property of their respective owners and Magellan claims no ownership in, nor any affiliation with, such trademarks. Any third party trademarks that appear in this material are used for information purposes and only to identify the company names or brands of their respective owners. No affiliation, sponsorship or endorsement should be inferred from the use of these trademarks. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan. |

3 Oct 2023 - Webinar Recording 26 September 2023| Getting the Most Out of the Fund Monitors Database

|

Webinar Recording | Getting the Most Out of the Fund Monitors Database FundMonitors.com 26 September 2023 |

|

To help you get a better understanding of the www.fundmonitors.com database, watch this webinar recording to help you learn to navigate the database and get the most out of its powerful fund analytics. The webinar covered the following:

|

28 Sep 2023 - The Rate Debate - Ep 42: Inflation has peaked

|

The Rate Debate - Ep 42: Inflation has peaked Yarra Capital Management September 2023 Outgoing Reserve Bank governor Philip Lowe finished his tenure as he began by keeping rates on hold as inflation cools. With inflation past its peak, can we expect rate cuts on the horizon, and could a softening of China's economy bring them even closer, or will services inflation drive the incoming governor Michele Bullock to deliver a rate rise later this year? Darren is joined by special guest Roy Keenan, Co-Head of Fixed Income, to explore this and the outlook for credit markets in episode 42 of The Rate Debate. |

|

Funds operated by this manager: Yarra Australian Equities Fund, Yarra Emerging Leaders Fund, Yarra Enhanced Income Fund, Yarra Income Plus Fund |

28 Aug 2023 - What really matters in investing

|

What really matters in investing Magellan Asset Management August 2023 |

|

Global Portfolio Managers, Arvid Streimann and Nikki Thomas dissect what's important and what's a distraction in the investment world. They talk us through where they are currently finding opportunities and how they are positioning the portfolio to benefit from structural tailwinds. Investment Analyst, Emma Henderson joins them to provide a deep dive into our restaurant holdings and why we like them. |

|

Funds operated by this manager: Magellan Global Fund (Hedged), Magellan Global Fund (Open Class Units) ASX:MGOC, Magellan High Conviction Fund, Magellan Infrastructure Fund, Magellan Infrastructure Fund (Unhedged), MFG Core Infrastructure Fund Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 ('Magellan') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to a Magellan financial product may be obtained by calling +61 2 9235 4888 or by visiting www.magellangroup.com.au. Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of a Magellan financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. Magellan makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Magellan. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Magellan will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material. Any third party trademarks contained herein are the property of their respective owners and Magellan claims no ownership in, nor any affiliation with, such trademarks. Any third party trademarks that appear in this material are used for information purposes and only to identify the company names or brands of their respective owners. No affiliation, sponsorship or endorsement should be inferred from the use of these trademarks. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan. |

8 Aug 2023 - Webinar Podcast 01 Aug 2023 | Infrastructure Funds - Analysing the Opportunities and Risks

|

Webinar Podcast | Infrastructure Funds - Analysing the Opportunities and Risks FundMonitors.com 01 August 2023 |

|

Listen to the podcast to discover the key insights and opportunities in this dynamic investment landscape. In this informative 45-minute session, we explored the potential benefits and risks of investing in infrastructure funds and uncovered the various types of infrastructure assets, including transportation, energy, and social infrastructure. Our panel consisting of Sarah Shaw from 4D Infrastructure, Ben McVicar from Magellan, and Matt Lorback from Atlas Infrastructure also delved into the regulatory and policy considerations impacting infrastructure investments. |

3 Aug 2023 - In Conversation with Airlie's Analysts

|

In Conversation with Airlie's Analysts Airlie Funds Management July 2023 |

|

Airlie Australian Share Fund Portfolio Manager, Emma Fisher, engages in a conversation with Airlie's senior analysts, Vinay Ranjan and Joe Wright. Emma discusses the performance of the Australian market during the past 12 months and asks Joe and Vinay to share insights on how some of their stocks have performed during the year within the Fund. This includes Mineral Resources, QBE Insurance and James Hardie. Funds operated by this manager: Important Information: Units in the fund(s) referred to herein are issued by Magellan Asset Management Limited (ABN 31 120 593 946, AFS Licence No. 304 301) trading as Airlie Funds Management ('Airlie') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to an Airlie financial product or service may be obtained by calling +61 2 9235 4760 or by visiting www.airliefundsmanagement.com.au. Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of an Airlie financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. Airlie makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Airlie. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. Any third party trademarks contained herein are the property of their respective owners and Airlie claims no ownership in, nor any affiliation with, such trademarks. Any third party trademarks that appear in this material are used for information purposes and only to identify the company names or brands of their respective owners. No affiliation, sponsorship or endorsement should be inferred from the use of these trademarks.. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Airlie. |

21 Jul 2023 - Why railroads are an attractive investment and how PSR is helping

|

Why railroads are an attractive investment and how PSR is helping Magellan Asset Management June 2023 |

|

Yathavan Suthaharan, Investment Analyst, discusses why railroads are an attractive infrastructure investment, recent events at Norfolk Southern and what the hype is around PSR. |

|

Funds operated by this manager: Magellan Global Fund (Hedged), Magellan Global Fund (Open Class Units) ASX:MGOC, Magellan High Conviction Fund, Magellan Infrastructure Fund, Magellan Infrastructure Fund (Unhedged), MFG Core Infrastructure Fund Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 ('Magellan') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to a Magellan financial product may be obtained by calling +61 2 9235 4888 or by visiting www.magellangroup.com.au. Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of a Magellan financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. Magellan makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Magellan. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Magellan will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material. Any third party trademarks contained herein are the property of their respective owners and Magellan claims no ownership in, nor any affiliation with, such trademarks. Any third party trademarks that appear in this material are used for information purposes and only to identify the company names or brands of their respective owners. No affiliation, sponsorship or endorsement should be inferred from the use of these trademarks. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan. |

3 Jul 2023 - Webinar Recording 27 June 2023 | Resource Funds - Analysing the Opportunities and Risks

|

Webinar Recording | Resource Funds - Analysing the Opportunities and Risks FundMonitors.com 27 June 2023 |

|

Resource funds can offer a unique avenue for capitalising on the growing demand for natural resources and the global shift towards sustainable energy and materials. In this webinar, we looked at the strategies and approaches employed by three successful resource fund managers and learn how they navigate the opportunities and risks associated with this asset class. Watch the recording of our manager round table webinar, where we were joined by Dan Porter from Pure Asset Management, David Franklyn from Argonaut Funds Management, and Matthew Langsford from Terra Capital. They shared their views on this interesting and diverse market sector. |

27 Jun 2023 - Banks, interest rates and opportunities in the finance sector

|

Banks, interest rates and opportunities in the finance sector Magellan Asset Management June 2023 |

|

Alan Pullen, Portfolio Manager, discussed the recent bank defaults, the impact of interest rates on banks in general and where he sees opportunities in the financial sector. |

|

Funds operated by this manager: Magellan Global Fund (Hedged), Magellan Global Fund (Open Class Units) ASX:MGOC, Magellan High Conviction Fund, Magellan Infrastructure Fund, Magellan Infrastructure Fund (Unhedged), MFG Core Infrastructure Fund Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 ('Magellan') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should read and consider any relevant offer documentation applicable to any investment product or service and consider obtaining professional investment advice tailored to your specific circumstances before making any investment decision. A copy of the relevant PDS relating to a Magellan financial product or service may be obtained by calling +61 2 9235 4888 or by visiting www.magellangroup.com.au. Past performance is not necessarily indicative of future results and no person guarantees the future performance of any strategy, the amount or timing of any return from it, that asset allocations will be met, that it will be able to be implemented and its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of a Magellan financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. Magellan makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Magellan. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. Any trademarks, logos, and service marks contained herein may be the registered and unregistered trademarks of their respective owners. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan. |

Online Applicatons

Free, simple and secure

Olivia123 - the fast simple and secure online alternative to completing paper based application forms.